Why identity verification sits at the center of modern fintech

One of the most surprising things about fintech is how much has to happen before a user even makes the first payment.

From the outside, digital onboarding looks simple. A user downloads an app, enters a few details, scans an ID, takes a selfie, and opens an account. It feels fast, almost casual.

But behind that short experience, a fintech company is trying to answer a very serious question:

Is this person real, and can this service trust them enough to open the door?

That is why identity verification matters so much in fintech.

It is not just a compliance step. It is the starting point of trust. If identity verification is weak, fraud can enter early. If it is too heavy, real users drop off before they even begin. Good onboarding lives in that narrow space between security and convenience.

What identity verification in fintech actually means

Identity verification in fintech is the process of checking whether a person opening or accessing a digital financial service is really who they claim to be.

That usually sounds simple until you imagine what fintech companies are really dealing with.

They are not verifying people face to face at a bank counter. They are verifying them remotely, through a phone screen, often in just a few minutes. That means they need to evaluate documents, facial images, device signals, user behavior, and onboarding risk all at once.

So identity verification in fintech is not one single check. It is a chain of checks.

It often includes:

- collecting basic personal information

- checking official ID documents

- comparing a selfie to the ID

- detecting liveness or spoofing attempts

- screening against risk or compliance rules

- deciding whether to approve, review, or reject the onboarding

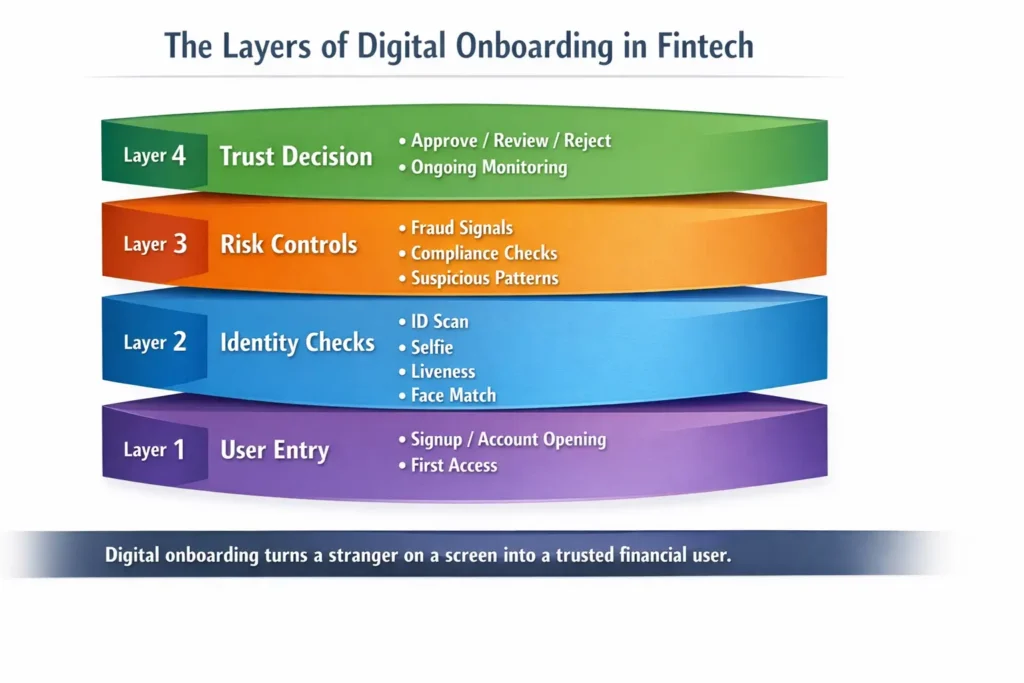

This is why digital onboarding is not just a sign-up flow. It is a trust-building engine.

The basic onboarding flow in fintech

Most fintech onboarding journeys follow a similar logic, even if the design looks different from app to app.

| Step | What the user sees | What the fintech is really checking |

|---|---|---|

| 1. Sign-up | Email, phone number, password, or passkey | Basic account setup and contact verification |

| 2. Personal details | Name, address, date of birth | Identity consistency and data completeness |

| 3. ID capture | Photo of passport, ID card, or driver’s license | Document authenticity and data extraction |

| 4. Selfie or video | Face scan or short live capture | Face match, liveness, and spoof detection |

| 5. Risk checks | Usually invisible to the user | Fraud signals, compliance checks, suspicious patterns |

| 6. Decision | Approved, pending review, or rejected | Trust decision based on identity and risk |

This is why digital onboarding can feel almost magical when it works well. The user sees a quick mobile flow. The fintech sees a layered decision process.

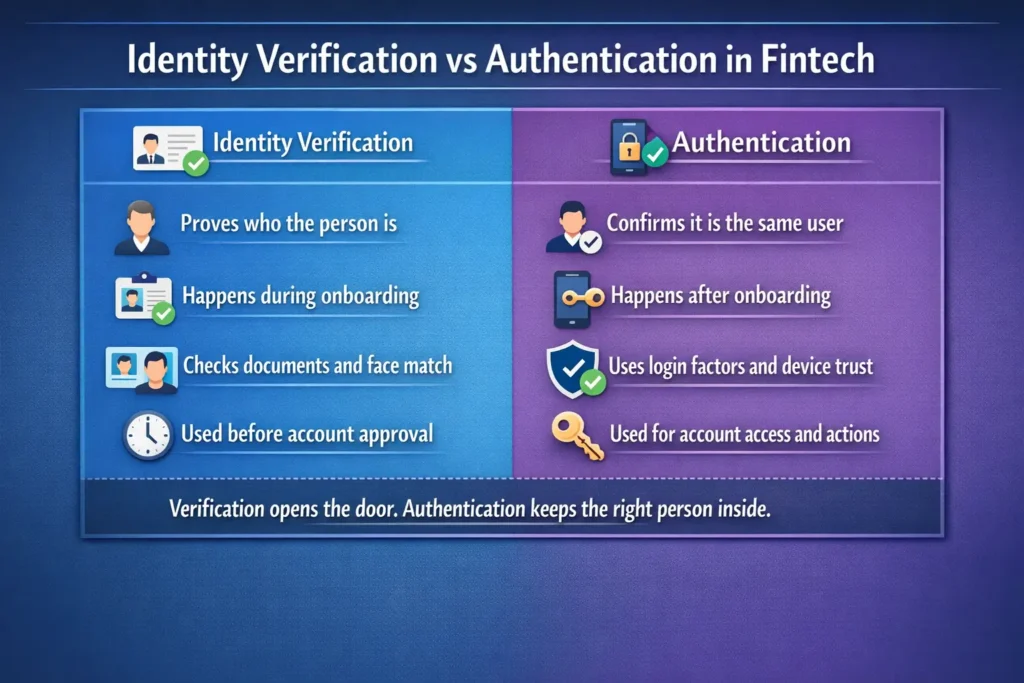

Identity verification is not the same as authentication

This is where many beginners get confused.

Identity verification and authentication are related, but they are not the same thing.

Identity verification happens when a service tries to establish who a user is.

Authentication happens later, when the service checks whether the person coming back is really the approved user.

A simple way to think about it is this:

- identity verification = proving your identity at the door

- authentication = proving it is still you every time you come back

That distinction matters because fintech security does not end when onboarding ends. In fact, onboarding is just the first trust decision. After that, authentication, device trust, biometrics, passkeys, and transaction monitoring keep that trust alive.

Why fintech onboarding is harder than it looks

Digital onboarding has to do two difficult things at the same time.

First, it has to stop fake identities, stolen identities, synthetic identities, and manipulated onboarding attempts.

Second, it has to avoid making normal people feel like they are being interrogated by an airport security team just to open a financial app.

That tension is the whole game.

If onboarding is too light, fraud risk increases.

If onboarding is too heavy, growth slows down.

This is why identity verification in fintech is never just about accuracy. It is also about user experience.

A great onboarding flow feels smooth for a legitimate user, but difficult for a fraudster. That sounds obvious, but in practice it is incredibly hard. The same selfie check that feels effortless to one user may fail another because of lighting, camera quality, document wear, or connection issues.

The main risks fintechs are trying to stop

When people think about identity verification, they often imagine only fake IDs. In reality, the problem is much broader.

A fintech onboarding system may be trying to catch:

- stolen identity information used by someone else

- synthetic identities built from real and fake data

- document tampering or forged IDs

- impersonation using another person’s face or image

- bot-driven sign-up attacks

- mule account creation for later fraud activity

That is why strong onboarding does not rely on one signal. A document image alone is not enough. A selfie alone is not enough. A name and address alone are not enough.

Trust comes from combining signals.

The best systems do not ask only, “Does this look like a real person?”

They also ask, “Does this entire onboarding story make sense?”

Why biometrics and liveness matter so much

One of the biggest changes in fintech onboarding is the use of biometrics and liveness checks.

A selfie is no longer just a selfie. It is often part of a deeper verification process designed to answer questions like:

- Is this a real human in front of the camera?

- Is the face matching the ID document?

- Is the image live, or is someone using a photo, replay, or mask?

- Does the interaction look natural?

This matters because remote onboarding changed the old model completely. In the branch era, a human employee could compare a face and an ID in person. In fintech, that judgment has to happen digitally and at scale.

That is why liveness detection became such a central part of modern onboarding. It helps fintech firms separate a real user from a static image, manipulated media, or an impersonation attempt.

Identity verification is also a business issue

It is easy to think identity verification belongs only to compliance or security teams.

It does not.

It affects marketing, conversion, user experience, support costs, fraud losses, and long-term trust.

A poor onboarding flow creates friction.

A weak onboarding flow creates fraud.

A confusing onboarding flow creates abandonment.

That means identity verification is not just a risk control. It is also part of growth strategy.

If a fintech wants to scale, it needs onboarding that is:

- secure enough to block risky users

- smooth enough to keep real users moving

- flexible enough to handle different devices and markets

- reliable enough to support trust over time

In other words, onboarding is where product design and security design meet.

The real takeaway

Identity verification in fintech is not just a box to tick before account opening.

It is the process that turns a stranger on a screen into a trusted user inside a financial system.

That is why digital onboarding matters so much. It is where fintech companies decide who can enter, under what level of confidence, and with what level of ongoing monitoring.

When digital onboarding works well, it feels simple.

When you look underneath, it is anything but simple.

It is document checks, face matching, liveness signals, risk scoring, compliance logic, fraud detection, and user experience design all working together in a few short minutes.

That is what makes identity verification one of the most important foundations in modern fintech.

References

Fintech Cybersecurity: Why Security Is the Real Infrastructure Behind Digital Finance

What Is Fraud Detection in Banking? Real Examples of How Banks Spot Fraud