Why digital fraud in fintech often looks normal at first

When people think about fraud in fintech, they often imagine a dramatic cyberattack.

Real fraud usually looks much more ordinary.

A fake account gets opened with stolen information. A login comes from a new device, but not one strange enough to trigger an instant block. A payment looks routine on the surface. A customer receives a message that feels just believable enough to trust.

That is what makes fraud so dangerous in digital finance. It rarely announces itself. It often hides inside normal-looking user behavior.

That is why fraud prevention in fintech matters so much. It is not just about blocking obviously bad activity. It is about spotting weak signals early, connecting them quickly, and stopping fraud before it turns into real loss.

What fraud prevention in fintech actually means

Fraud prevention in fintech is the system companies use to detect, reduce, and stop dishonest activity across onboarding, login, payments, transfers, and account use.

It is much bigger than one fraud tool or one security rule.

A fintech company may need to stop:

- fake or stolen identities during sign-up

- account takeover after login

- suspicious transfers and payment abuse

- scam-driven customer actions

- repeated fraud attempts across linked devices or accounts

So fraud prevention is not one checkpoint. It is a full monitoring and decision system.

In simple terms, fintech fraud prevention keeps asking the same question again and again:

Does this action make sense for this user, at this moment, in this context?

Why fraud prevention in fintech feels different from traditional fraud control

Traditional financial fraud controls often operated in a more limited environment. Branch visits, card-present transactions, face-to-face identity checks, and slower service flows gave institutions more context before money moved.

Fintech changed that.

Accounts can now be opened remotely. Payments can move almost instantly. Apps rely on mobile devices, APIs, cloud systems, and outside connections. A fraudster no longer needs to walk into a branch or physically use a stolen card. They can exploit identity data, weak login controls, rushed onboarding flows, or social engineering at scale.

That is why fraud prevention in fintech feels broader. It is not only protecting a payment. It is protecting the full digital journey that leads to the payment.

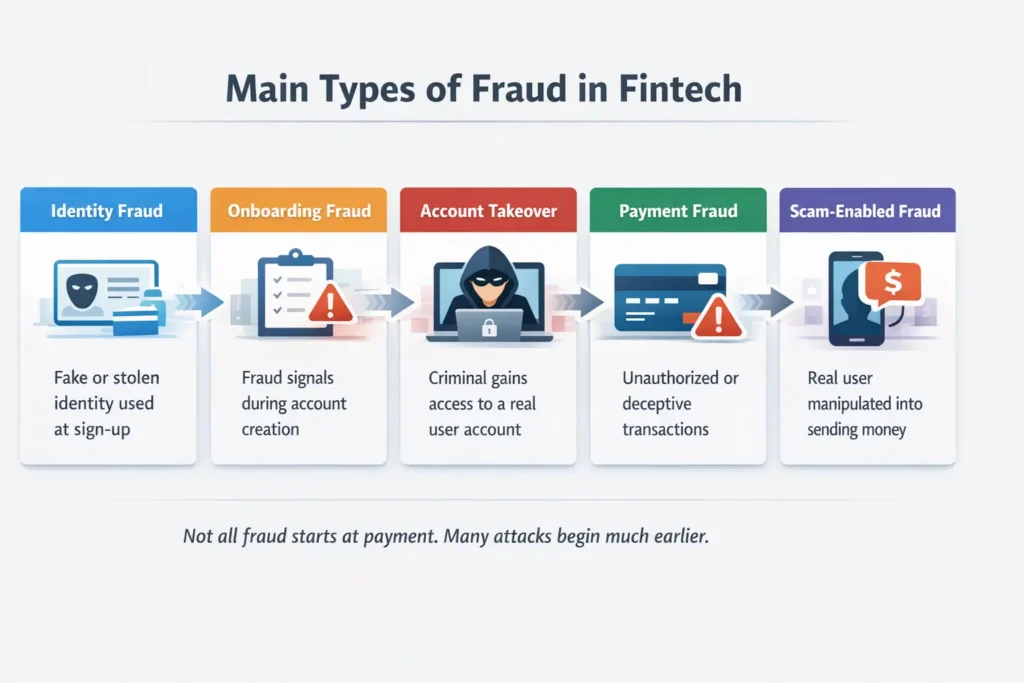

The main types of fraud fintech companies try to stop

The easiest way to understand fintech fraud prevention is to look at the major fraud patterns.

| Fraud type | What it looks like | Why it matters |

|---|---|---|

| Identity fraud | Fake or stolen identity used to open an account | Fraud enters before the relationship even begins |

| Onboarding fraud | Suspicious behavior during account creation | Weak entry controls create future losses |

| Account takeover | Criminal gains access to a real customer account | A trusted account becomes a fraud channel |

| Payment fraud | Unauthorized or deceptive transaction activity | Money can move before the user reacts |

| Scam-enabled fraud | A real customer is manipulated into sending money or sharing codes | Normal-looking actions can still be fraud-driven |

This is why strong fraud prevention starts before the first transaction and continues long after the account is approved.

Fraud prevention begins before money moves

One of the biggest mistakes in fintech is treating fraud as only a payments problem.

Fraud often starts much earlier.

If a bad actor can create an account using stolen or synthetic identity information, they do not need to “break in” later. They are already inside. The account may even behave normally for a while before being used for abuse.

That is why onboarding controls matter so much. A fintech company has to look at document quality, selfie checks, liveness, device risk, signup speed, IP patterns, and behavior inconsistencies before the account is even opened.

To the user, onboarding may feel simple.

Behind the scenes, it is often one of the most important fraud decision points in the entire customer journey.

The real challenge is not blocking everything

This is where fraud prevention gets difficult.

A weak system lets too much suspicious activity pass.

A clumsy system blocks too many real users.

Both are expensive.

If a company misses fraud, it loses money, time, and trust. If it creates too many false positives, real users get frustrated, abandon the app, or stop trusting the service.

That is why the best fintech fraud systems do not act like hard walls. They act more like intelligent filters.

- low-risk actions may move smoothly

- medium-risk actions may trigger extra checks

- high-risk actions may be delayed, challenged, reviewed, or blocked

That layered approach matters because not every unusual action is fraud. Sometimes a real customer really is logging in from a new phone while traveling. Good fraud prevention is not just about suspicion. It is about context.

What signals fintech companies actually use

Fraud prevention sounds complicated until you break it into signals.

A fintech company may look at:

- whether the device is new or trusted

- whether login behavior matches past patterns

- whether the transaction amount is unusual

- whether the location suddenly changed

- whether multiple accounts behave in similar suspicious ways

- whether the user skipped or failed expected steps

- whether the identity story makes sense from start to finish

One signal alone may mean very little.

But several unusual signals together can tell a very different story.

That is why modern fintech fraud prevention is often about combining weak clues into a stronger judgment. A fraudster may try to look normal in one area. The system tries to detect the mismatch across many areas.

Why account takeover is such a serious problem

One of the most important fraud risks in fintech is account takeover.

This happens when a criminal gains access to a real customer account and starts acting like the legitimate user. That can lead to stolen funds, changed account details, linked device abuse, or fraudulent transfers.

What makes account takeover especially dangerous is that the account already has trust. It may already be verified, active, and familiar to the system. That means the fraudster is not attacking from outside. They are abusing a trusted relationship from inside.

This is why authentication, device trust, step-up verification, and behavioral monitoring are so closely tied to fraud prevention.

Fraud prevention is also a customer experience issue

This part is easy to overlook.

Fraud prevention is not just a risk function. It shapes product experience directly.

A customer who gets blocked too often may leave.

A customer who suffers account takeover may never return.

A customer who feels unsafe linking a bank account may never finish onboarding.

That means fraud prevention affects:

- conversion

- retention

- support costs

- trust in the brand

- long-term growth

The best fintech products do not feel like fraud systems. They quietly guide users through safer behavior and only add friction when the risk justifies it.

That balance is hard to get right, but it is one of the biggest differences between weak fraud prevention and strong fraud prevention.

Why fraud prevention in fintech is becoming more adaptive

Fraud is changing because digital behavior is changing.

Scammers are blending identity theft, account abuse, social engineering, and payment manipulation in ways that make old fraud categories feel less separate. Some fraud begins outside the fintech app, then enters through a login, a transfer, or a customer support interaction.

That means fintech fraud prevention cannot rely only on fixed rules from the past.

It has to become more adaptive. It has to connect onboarding risk with login risk, payment risk, and account behavior in real time.

The strongest systems are not built around one “fraud tool.” They are built around connected judgment across identity, access, payments, behavior, and trust.

The real takeaway

Fraud prevention in fintech is not simply about blocking suspicious transactions.

It is about stopping fraud before the account opens, during login, during payment, and even during the moments when a real customer is being manipulated into doing the wrong thing.

That is what makes it so important.

A fintech company is not only protecting money. It is protecting the full path that leads to money movement.

When fraud prevention works well, users barely notice it.

When it fails, everything suddenly feels fragile.

That is why the best fintech companies treat fraud prevention as part of product design, not just part of risk management.

References

FFIEC, Authentication and Access to Financial Institution Services and Systems