Fintech security is not just about blocking hackers

When people hear the word fintech, they usually think of speed, convenience, and smooth user experience.

Open an account in minutes. Send money with a few taps. Verify your identity through a phone camera. Pay without ever touching a card reader.

That is exactly why fintech security matters so much.

The more convenient finance becomes, the more exposed it also becomes. Every login, every API connection, every onboarding flow, every payment request, and every data-sharing process creates a new point of trust. If that trust breaks, the service may still look modern, but it no longer feels safe.

That is why fintech security is not a side issue. It is part of the product itself.

So what is fintech security?

Fintech security is the full system that helps digital financial services stay safe, reliable, and trustworthy.

It includes checking whether a user is real, controlling who can access what, protecting sensitive data, detecting suspicious behavior, stopping fraud, and keeping services running even when something goes wrong.

In other words, fintech security is not one lock on one door.

It is the entire building design.

A strong fintech service does not only ask, “Can users log in?”

It also asks:

- Is this really the right person?

- Is this action normal or suspicious?

- Is the data protected while moving and while stored?

- Can the system recover quickly if there is an attack or outage?

- Will users still trust us after something goes wrong?

That is the real meaning of fintech security.

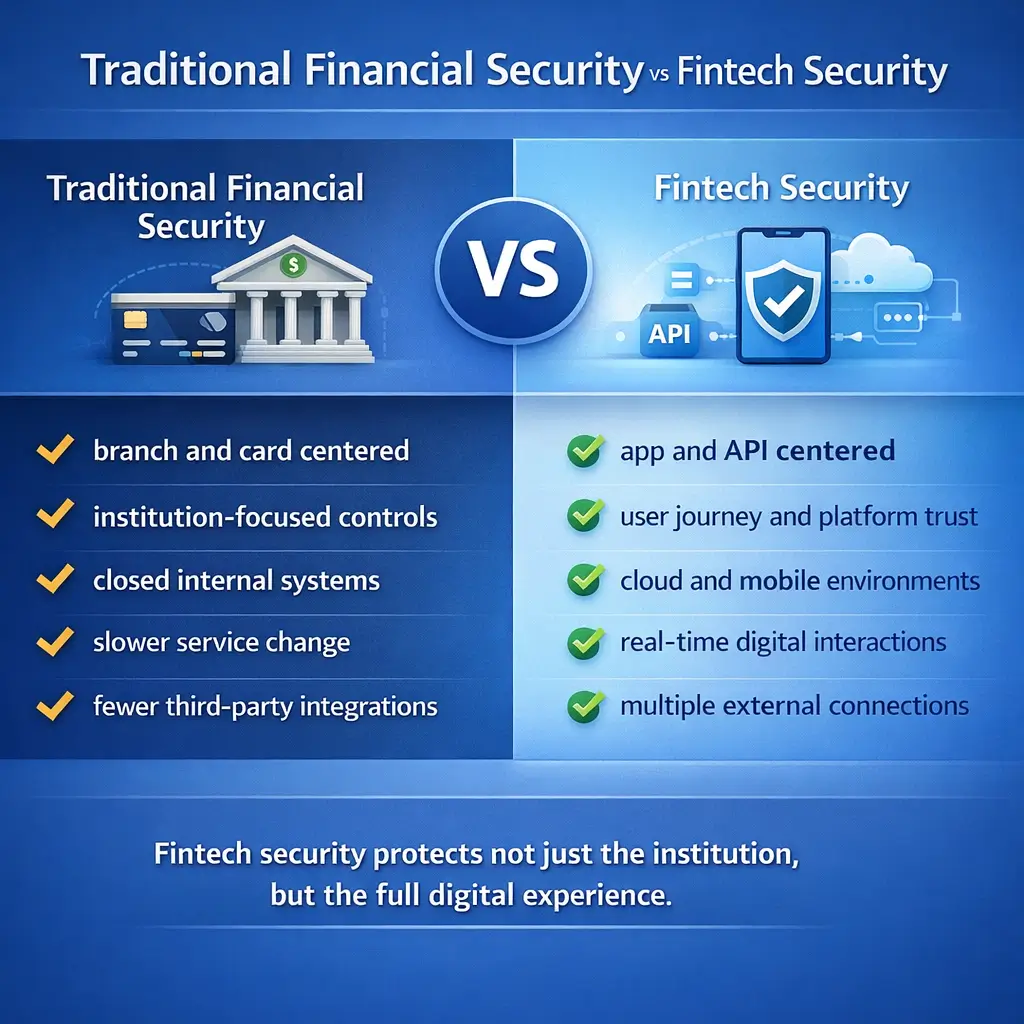

Why fintech security feels different from traditional financial security

Traditional financial security often focused on protecting the institution.

Fintech security has to protect the institution, the platform, the user journey, and the connections between many outside systems at the same time.

That is a big difference.

A fintech company may depend on cloud services, third-party APIs, identity providers, payment processors, open banking connections, and mobile app infrastructure all at once. That makes the service powerful, but it also increases the number of places where risk can appear.

Here is a simple way to think about it.

| Area | Traditional finance focus | Fintech security focus |

|---|---|---|

| Customer access | Branch, card, bank login | App login, device trust, MFA, passkeys |

| Identity | In-person verification | Remote identity verification, onboarding checks |

| Data | Internal banking systems | APIs, mobile apps, cloud, third-party sharing |

| Fraud | Transaction fraud monitoring | Onboarding fraud, account takeover, behavioral fraud |

| Reliability | Core system continuity | Always-on digital service and fast recovery |

This is why fintech security feels broader. It is not only about keeping attackers out. It is also about keeping digital finance usable, reliable, and trusted.

The first layer: identity and access

Everything starts with identity.

Before a fintech service can move money, approve a loan, open an account, or connect financial data, it has to answer one basic question:

Who is this person?

That sounds simple, but in digital finance it is one of the hardest questions to answer well.

A good fintech service needs to know whether the person signing up is real, whether the ID document is genuine, whether the selfie matches the document, and whether the behavior looks normal. Then, after onboarding, the service has to keep checking whether the same person is the one coming back later.

That is why identity and authentication are not the same thing.

Identity verification is about proving who someone is.

Authentication is about proving that the person trying to log in right now is really the approved user.

In practice, that is where tools like MFA, biometrics, device binding, and passkeys become important. Good fintech security makes this process feel light for real users and hard for bad actors.

The second layer: fraud prevention

This is where fintech security becomes much more interesting.

Many people imagine cybersecurity as a story about hackers breaking into systems. But in digital finance, fraud is often even more practical and more damaging.

Someone may use stolen information to open an account.

Someone may take over a real customer’s login.

Someone may trigger a transfer that looks ordinary on the surface but is actually part of a scam.

So fintech security is not only technical defense. It is also pattern recognition.

It tries to notice the difference between normal behavior and risky behavior.

That means asking questions like:

- Is this login coming from a strange device?

- Is this payment request unusual for this user?

- Is this account behaving like a mule account?

- Is this identity synthetic, stolen, or manipulated?

- Does this onboarding flow show signs of fraud?

Fraud prevention matters because many fintech attacks do not look like “attacks” at first. They often look like ordinary customer actions until the signals are examined more closely.

The third layer: data and API protection

Fintech runs on connections.

Banks, fintech apps, payment providers, identity vendors, cloud platforms, and open banking systems all exchange data through digital channels. That is part of what makes modern finance feel seamless.

But smooth connections can also become weak points if they are not protected carefully.

Financial data is not ordinary data. It can reveal where people spend, how they earn, which accounts they hold, and how they behave financially. If that kind of information leaks, the damage is not only technical. It becomes personal very quickly.

That is why fintech security has to protect data in storage, in transit, and in shared environments. It also has to control which outside party can access what, for how long, and for what purpose.

When people talk about API security in fintech, this is what they mean. APIs are not just technical tools. They are trust channels.

The fourth layer: resilience and trust

This is the part many beginners overlook.

A secure fintech service is not only one that prevents attacks. It is also one that can keep operating, respond quickly, and recover well when something unexpected happens.

That matters because finance is emotional.

People do not panic when a music app stops working for ten minutes.

They react very differently when a payment app fails, when an important transfer is delayed, or when they cannot access their account.

In fintech, resilience is part of security because trust is part of security.

Users trust digital finance when they believe three things:

- Their identity is protected.

- Their money and data are handled safely.

- The service will not collapse the moment something goes wrong.

That is why strong fintech security includes incident response, business continuity, service recovery, and operational resilience. A service that cannot recover quickly may still have good controls on paper, but it will not feel safe in real life.

Why this matters for users, not just companies

It is easy to think fintech security is only a company problem.

It is not.

It shapes the user experience every day.

A strong security design can mean:

- faster but safer onboarding

- less account takeover risk

- fewer false declines

- better trust in payments and transfers

- more confidence when sharing financial data

A weak security design can mean:

- frustrating verification flows

- too much friction for normal users

- more fraud losses

- more support issues

- lower trust in the brand

The best fintech products do not force users to constantly think about security. They make safety feel built in.

That is the real goal.

The real takeaway

Fintech security is much bigger than anti-hacking tools.

It is the system that connects identity, authentication, fraud prevention, data protection, API security, and operational resilience into one trust framework for digital finance.

That is why security in fintech is not just a technical layer behind the scenes. It is one of the main reasons users trust a service enough to keep using it.

A fintech company can have a beautiful app, fast onboarding, and smart features. But if users do not feel safe, the product will always feel incomplete.

In digital finance, trust is not a marketing message.

It is an operating requirement.

References

Finteconomix, Fintech Cybersecurity Infrastructure Finance

FFIEC, Authentication and Access to Financial Institution Services and Systems