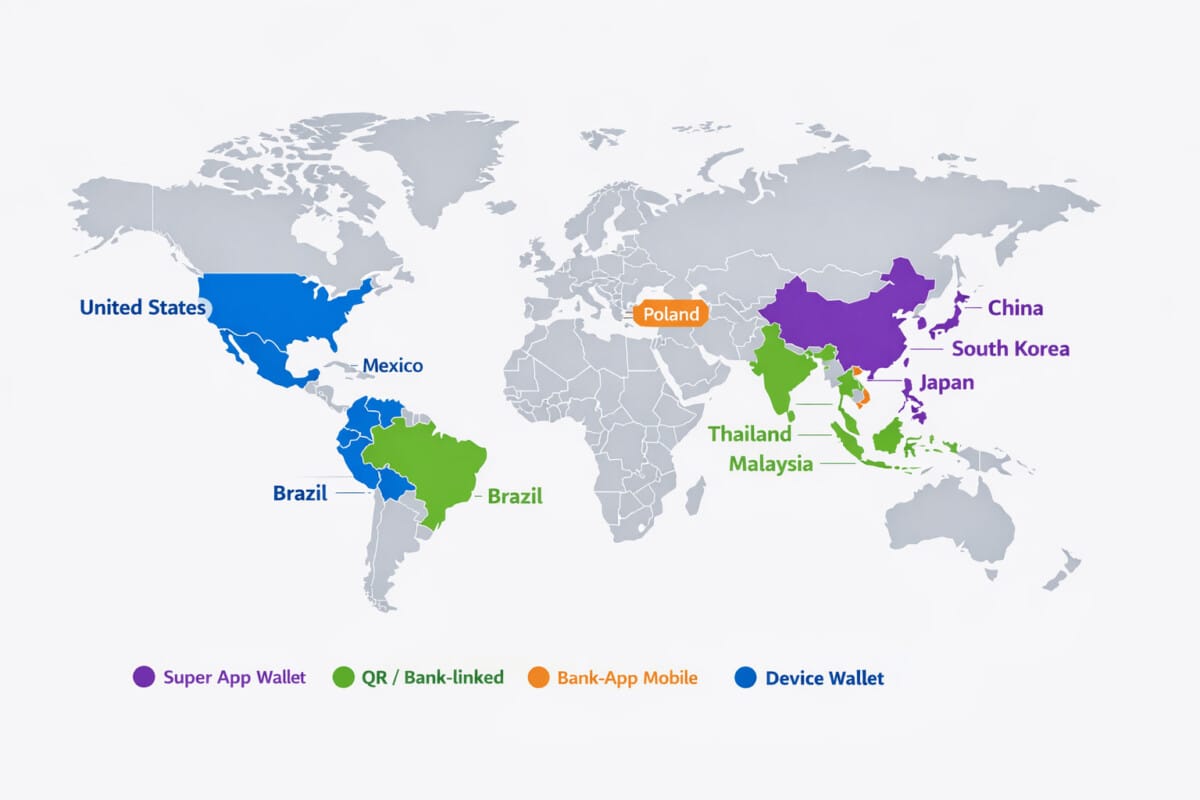

Global Wallet Map

Explore how mobile wallet ecosystems differ across countries, from super apps and QR wallets to bank-app payment layers and device wallets. This page is designed as a visual reference for consumer-facing wallet infrastructure across major payment markets.

Markets included in the current version

Wallet models used for comparison

A key format in many Asian wallet ecosystems

The main consumer interface in most wallet-led markets

Asia

Asia contains some of the world’s most important wallet-led and QR-led payment markets, ranging from super apps to bank-linked mobile payment layers.

China

Super app wallet

China is one of the clearest examples of a wallet-led consumer payment ecosystem built around app-first payment behavior.

China’s mobile wallet model is defined by super apps that combine payment, commerce, and broader digital services in one consumer interface.

South Korea

App wallet layer

South Korea’s wallet layer is shaped by app-based payments built on top of an already mature digital finance environment.

Korea is not a pure wallet-only market, but mobile wallet layers are highly visible in online and app-based consumer payments.

India

Bank-linked app layer

India’s mobile wallet experience is closely tied to UPI apps rather than a single closed stored-value wallet model.

India is best understood as an app-led account-to-account mobile payment market rather than a traditional closed wallet market.

Singapore

Bank-app mobile layer

Singapore’s mobile payment experience is shaped by fast bank-linked transfers and mobile-number-based payment usability.

Singapore is useful because the consumer experience feels mobile-wallet-like even though the underlying structure is strongly bank-account-based.

Thailand

QR-led mobile layer

Thailand is a strong example of a mobile payment market built around fast transfers and QR-based consumer use.

Thailand is especially relevant because QR-based mobile payments are closely linked to domestic and cross-border consumer payment use.

Malaysia

National QR layer

Malaysia’s wallet map is strongly shaped by a shared QR payment layer that connects banks and e-wallet providers.

Malaysia stands out because one QR layer can connect multiple wallet and banking ecosystems at the merchant side.

Japan

QR wallet

Japan’s wallet market is strongly associated with QR apps rather than one national bank-transfer mobile layer.

Japan is useful because it shows a wallet market built around consumer QR apps instead of a single dominant real-time bank transfer wallet experience.

Europe

Europe includes some mobile payment models that feel like wallets to users even when they are tightly connected to banking apps and local payment schemes.

Poland

Bank-app mobile layer

Poland’s mobile payment experience is strongly shaped by BLIK, which sits inside banking apps rather than a standalone super app wallet model.

Poland is a strong example of how banking apps themselves can become the main mobile wallet-like interface for consumers.

North America

In North America, device wallets are often more important than local super apps when consumers pay with phones in stores or online.

United States

Device wallet

The US wallet market is shaped more by device wallets layered on top of cards than by one domestic wallet super app.

The US is best understood as a device-wallet-over-card market rather than a QR-first mobile wallet market.

Latin America

Latin America includes app-based wallet ecosystems that often sit close to e-commerce, merchant services, and fast-moving consumer finance adoption.

Mexico

Digital wallet

Mexico’s wallet layer is visible in app-based ecosystems that combine payments, balance, transfers, and merchant acceptance.

Mexico is useful because wallet growth is closely connected to merchant acceptance and broader platform ecosystems.

Brazil

Digital wallet ecosystem

Brazil combines strong fast-payment infrastructure with highly visible app-based wallet brands in consumer payments.

Brazil is especially interesting because mobile wallet brands coexist with one of the world’s most visible instant payment infrastructures.

Wallet models explained

These categories simplify comparison across markets. They are meant to highlight the main consumer-facing wallet model, not every payment product available in each country.

Super app wallet

A wallet built inside a broader app ecosystem that combines payments with commerce, messaging, or other daily digital services.

App wallet

A consumer-facing mobile wallet app used for payments, transfers, and digital checkout across multiple channels.

Bank-app mobile layer

A mobile payment experience that feels wallet-like to users but is strongly tied to bank accounts and banking apps.

Device wallet

A phone-based wallet layer that typically sits on top of existing card infrastructure for in-store and online payments.