RTGS is not just a fast payment message. It means settlement happens immediately, payment by payment, through central bank money.

If you search “what is RTGS,” you will usually find a short answer like this: RTGS stands for Real-Time Gross Settlement. That answer is correct, but it is also incomplete.

The real value of RTGS is not captured by the acronym alone. RTGS is not simply a fast way for banks to send payment instructions to each other. It is a settlement model designed for payments that need to be completed immediately, individually, and with finality, typically in central bank money. In other words, “real-time” does not just mean the message moves quickly. It means the settlement itself reaches the central bank layer right away, rather than being postponed to a later batch or netting cycle.

That distinction matters more than most explainers admit. In payments, there is a big difference between a transfer that looks instant on a screen and a transfer that is actually settled at the underlying money layer. RTGS belongs to the second category. It is the system architecture used when financial institutions want to eliminate as much waiting, ambiguity, and settlement uncertainty as possible. That is why RTGS sits at the center of wholesale banking, central bank operations, and high-value financial market infrastructure.

What RTGS actually means

To understand RTGS properly, it helps to break the phrase into its three parts.

Real-time means payment orders are processed as they arrive. They are not parked until the end of the day. They are not bundled into a later settlement window. They move through the system on a continuous basis.

Gross means each payment is settled one by one, in full. The system does not first offset what one bank owes another against opposite-direction payments before settlement.

Settlement means the transfer is completed at the level that matters for final discharge of the obligation. In RTGS systems, that usually means settlement in central bank money, which is considered the safest settlement asset in the financial system.

Put those pieces together and you get the core idea: RTGS is a system where payments are settled individually, immediately, and finally in central bank money. That is why the concept is so important. It is not just about faster communication between institutions. It is about immediate completion of the payment at the settlement layer itself.

Why “real-time” is the most important word

The word real-time is often misunderstood because it sounds like marketing language. In retail payments, many services claim to be real-time, instant, or immediate even when the underlying settlement design is more complicated. RTGS is different because the term has a much stricter meaning.

In an RTGS system, the payment does not just receive a quick approval or acknowledgment. It is actually settled as it is processed. The European Central Bank explains that in T2, payment orders are settled one by one on a continuous basis in central bank money, with immediate finality. That is one of the clearest official descriptions of what RTGS means in practice.

The Federal Reserve makes the same logic clear in the U.S. context. Fedwire is used for large-value, time-critical payments, and payments processed over the service are made in central bank money and are final and irrevocable once made. That is not just a fast front-end user experience. It is a statement about where and how settlement is completed.

This is the point many articles miss. A payment instruction can be fast without being finally settled. RTGS matters because it closes that gap. The payment is not merely “on its way.” It is not “awaiting later net settlement.” It is done. For banks, central counterparties, and financial market participants, that difference is everything.

How RTGS works in the real world

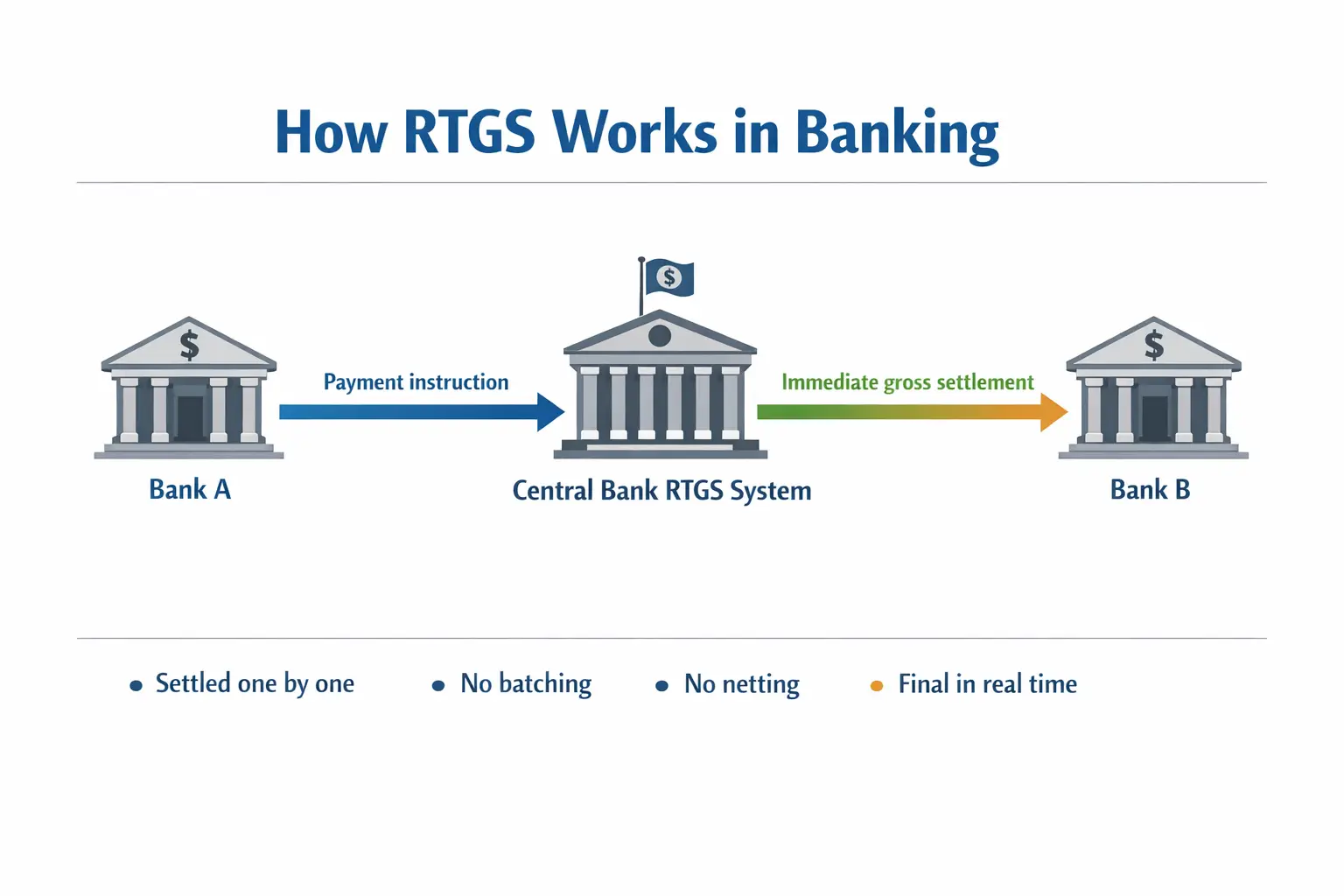

Imagine that Bank A needs to send a large-value payment to Bank B. In an RTGS environment, Bank A sends the instruction into the central bank-operated or central bank-anchored settlement system. If Bank A has sufficient liquidity in its settlement account, the payment is processed immediately. Bank A’s balance is debited, Bank B’s balance is credited, and the obligation is extinguished at that moment.

Then the next payment arrives and the system repeats the process.

Then the next one.

And the next one.

That is why RTGS is often described as transaction-by-transaction settlement. Each payment stands on its own. There is no need to wait for a queue of obligations to be combined and netted first. This design minimizes settlement uncertainty and gives participants immediate clarity about whether funds have actually moved.

This structure also explains why RTGS systems are commonly used for high-value and high-priority payments. If a bank is funding its liquidity position, making a major market payment, or settling the cash leg of a financial market transaction, waiting until the end of a batch cycle is often not acceptable. The system needs certainty now, not later.

Why central bank money matters so much

One of the most important things about RTGS is that it is usually built around central bank money. That is not a minor technical detail. It is a core reason why RTGS systems are trusted.

In modern monetary systems, central bank reserves are the ultimate safe settlement asset. Commercial bank money plays an enormous role in everyday finance, but when institutions want the highest degree of settlement safety, central bank money is the benchmark. BIS materials continue to emphasize that wholesale financial obligations in RTGS systems are typically settled in central bank money, and that central bank reserves remain the foundation of trusted settlement at par.

That is why saying “RTGS is a fast payment system” is not enough. A better explanation is this: RTGS is a central bank settlement design for critical payments. The money does not just move between two private institutions at the messaging level. It moves at the settlement layer where finality is recognized and legal uncertainty is minimized.

Why RTGS is used for wholesale payments

RTGS is not mainly designed for buying coffee or splitting dinner. It is designed for wholesale finance.

Wholesale payments include interbank transfers, central bank operations, large corporate payments routed through banks, securities-related cash settlement, and other transactions where values are high and timing is critical. These are the payments where delay can create funding stress, market disruption, or knock-on problems elsewhere in the system. The BIS notes that RTGS systems provide the safe and efficient foundation on which retail payment systems and cross-border payment arrangements rely.

That is an important point for a global audience. Retail payment brands get the headlines. Instant consumer apps get the attention. But underneath the visible payments experience, wholesale settlement infrastructure is doing the real heavy lifting. RTGS is part of that deep plumbing. It is what gives the system a place where critical obligations can be discharged with immediate finality.

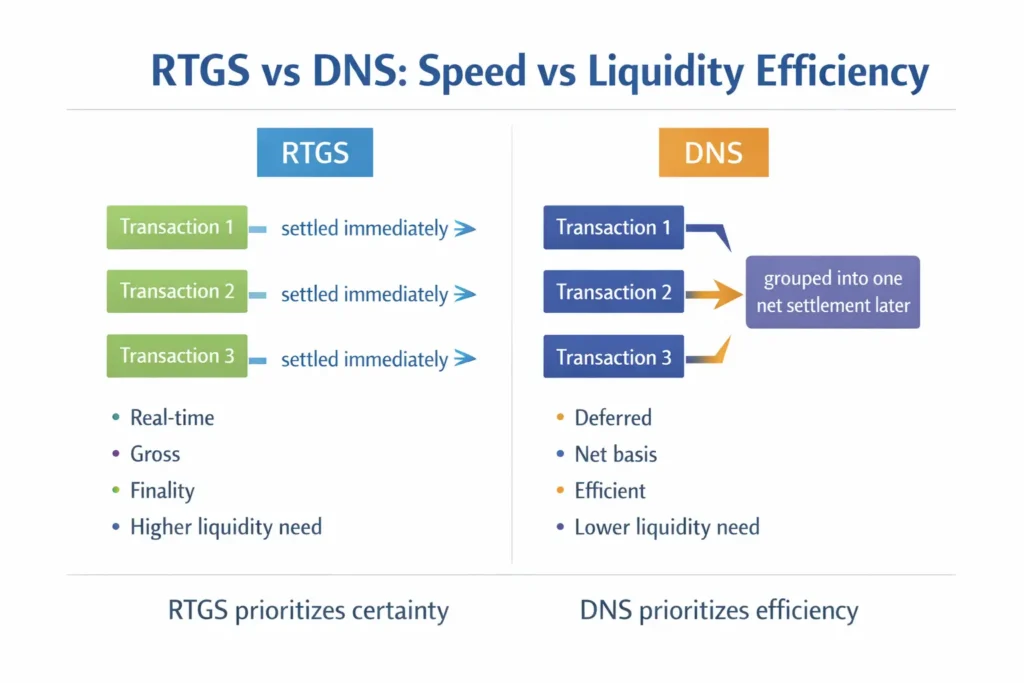

RTGS vs DNS: the difference that really matters

To understand RTGS fully, you have to compare it with DNS, or Deferred Net Settlement.

DNS follows a different logic. Instead of settling every payment one by one as it arrives, a DNS arrangement collects obligations over a period of time and settles them later on a net basis. If banks owe each other payments in both directions, those obligations are offset against each other first. Only the resulting net positions are settled later. The BIS describes DNS as settlement that occurs on a net basis at some later time.

This means RTGS and DNS are solving different problems.

RTGS says: settle now, payment by payment, in full.

DNS says: accumulate first, offset claims, and settle the final balance later.

RTGS prioritizes certainty at the settlement layer. DNS prioritizes efficiency in liquidity usage and operational throughput. That is why DNS is not some outdated relic that RTGS has rendered irrelevant. It is a different settlement design with a different strength.

Why DNS still has real advantages

A lot of content about RTGS quietly implies that real-time settlement must always be superior. That is too simplistic.

The main trade-off is liquidity. In RTGS, because payments settle individually and immediately, participants need enough funds available to make those payments as they arrive. In DNS, by contrast, offsetting obligations reduce the amount that must be settled in final form. This can make DNS much more liquidity-efficient, especially in systems with huge volumes of relatively lower-value payments.

That is why DNS remains attractive in many contexts. If the payment system’s main challenge is not immediate finality for every transaction but rather efficient handling of massive payment volumes, net settlement can be a very smart design. DNS can conserve liquidity, reduce settlement funding pressure, and support scale in ways that matter enormously for everyday payment ecosystems.

So the real comparison is not “advanced RTGS” versus “old-fashioned DNS.” The better comparison is this:

- RTGS is stronger on certainty and immediate finality

- DNS is stronger on liquidity efficiency

Modern payment system design is often about balancing those two goals rather than choosing one ideology forever.

RTGS is safer in one sense, but more demanding in another

Because RTGS settles payments continuously and individually, it reduces the risk that institutions accumulate unresolved obligations throughout the day. That is a major stability benefit. It lowers the uncertainty around whether a payment will eventually settle and reduces the chance that a late failure ripples backward through a chain of financial obligations.

But RTGS also makes liquidity management harder. If a participant lacks funds at the moment a payment arrives, the payment may have to wait in a queue until liquidity is available. BIS and central bank materials discuss how RTGS systems often depend on intraday liquidity arrangements to keep payments moving smoothly. In other words, RTGS improves settlement certainty but does not eliminate the need for active liquidity support and careful funding management.

That tension is one of the most interesting things about RTGS. It is often presented as the “gold standard” of settlement, and in many ways it is. But it is not magic. It shifts the problem. Instead of carrying more deferred settlement uncertainty, participants must carry more real-time liquidity discipline.

Why RTGS still matters even in the age of instant payments

Now that many countries are building fast retail payment systems, some readers might wonder whether RTGS still matters as much as it once did. The answer is yes.

Retail instant payment systems may offer near-immediate consumer experiences, but wholesale settlement architecture still matters enormously. In many jurisdictions, instant payment systems either settle directly in central bank money or rely on structures that are deeply connected to central bank settlement arrangements. The ECB’s TIPS service, for example, settles retail instant payments in central bank money. That illustrates the broader lesson: the visible user experience may change, but the importance of safe settlement infrastructure does not disappear.

In fact, the rise of 24/7 instant payment expectations can make liquidity management even more complicated for banks. That is one reason settlement design is becoming more important, not less. As payment systems become faster and more always-on, the relationship between settlement finality, liquidity availability, and central bank infrastructure becomes even more central to the conversation.

RTGS vs DNS at a glance

| Feature | RTGS | DNS |

|---|---|---|

| Full name | Real-Time Gross Settlement | Deferred Net Settlement |

| Timing | Immediate | Later, at defined intervals |

| Settlement basis | Payment by payment | Net basis after offsetting |

| Settlement asset | Typically central bank money | Final net positions settled later |

| Core strength | Finality and certainty | Liquidity efficiency |

| Main challenge | Higher intraday liquidity need | Delay before final settlement |

| Best fit | High-value, urgent, wholesale payments | High-volume flows where efficiency matters |

The clearest way to explain RTGS

If you want one sentence that gets to the heart of RTGS, use this:

RTGS means a payment is settled individually and immediately, all the way through the central bank settlement layer, instead of waiting to be netted and settled later.

That is the real meaning of real-time in RTGS. Not just fast transmission. Not just fast confirmation. Not just a quick front-end message. It means the payment reaches the place where final settlement actually happens.

And once you understand that, the rest of the debate becomes easier to read. RTGS is not simply “better because faster.” RTGS is stronger where certainty matters most. DNS remains valuable where liquidity efficiency matters more. Global payment systems need both ideas because not all payments are trying to solve the same problem.

References

- Bank for International Settlements (BIS) — Real-time gross settlement systems

- Bank for International Settlements (BIS) — The quest for speed in payments

- Federal Reserve — Fedwire Funds Service

- European Central Bank — T2 Glossary (PDF)