From payments and open banking to fraud, APIs, and quantum risk

fintech cybersecurity is often described as a technical problem. That framing is too small.

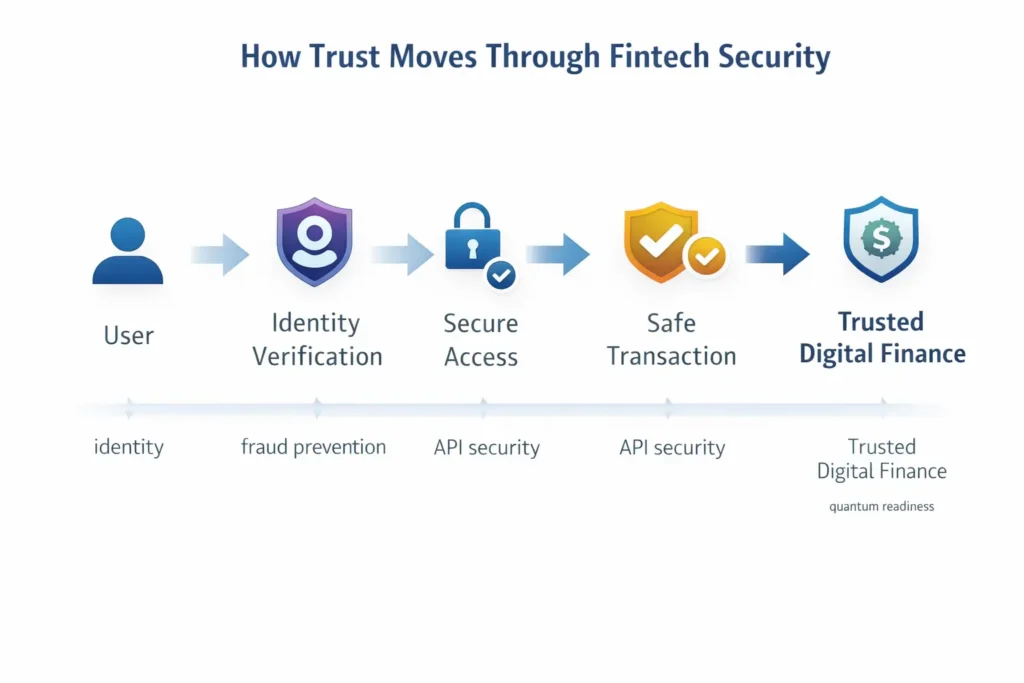

In reality, fintech cybersecurity is the system that keeps digital finance believable. A payment app only feels simple because an invisible stack is doing hard work in the background: verifying identity, checking whether a transaction looks legitimate, controlling API access, detecting fraud, and keeping services running even when systems are under stress.

That is why the topic matters now more than ever. Fintech is no longer just about faster checkout or cleaner mobile UX. It is about who gets trusted, how money moves, where data flows, and whether a platform can keep operating when attackers, outages, or third-party failures hit at the worst possible moment.

What fintech cybersecurity really means

At a basic level, fintech cybersecurity is the practice of protecting digital financial services from fraud, data compromise, service disruption, and unauthorized access.

But that definition still misses the real story.

Fintech security is not one lock on one door. It is a layered operating model across the full customer journey:

- identity verification when a user signs up

- authentication when a user logs in

- transaction monitoring when money moves

- API security when systems talk to each other

- resilience planning when something breaks

That is what makes fintech different from a normal consumer app. In social media, a breach is bad. In finance, a breach can turn into direct monetary loss, regulatory exposure, and a collapse of user trust within hours.

Why fintech cybersecurity matters more now

Digital finance has made money movement feel lightweight. A card payment takes seconds. A wallet can be linked in minutes. A new account can be opened without a branch visit.

The risk, though, has not disappeared. It has changed shape.

The biggest threats in fintech today are not limited to classic “hackers breaking into servers.” They also include account takeover, social engineering, synthetic identity fraud, API abuse, merchant fraud, payment scams, and operational disruption. In other words, the threat surface grows as finance becomes more connected, faster, and more programmable.

That matters because fintech losses are not abstract. The U.S. FTC said consumers reported losing more than $12.5 billion to fraud in 2024, up 25% year over year, and bank transfers and payment methods remained a major channel for losses. That is exactly why fintech cybersecurity is not just an IT concern. It is a business model concern and a trust concern.

Source: FTC press release, March 10, 2025

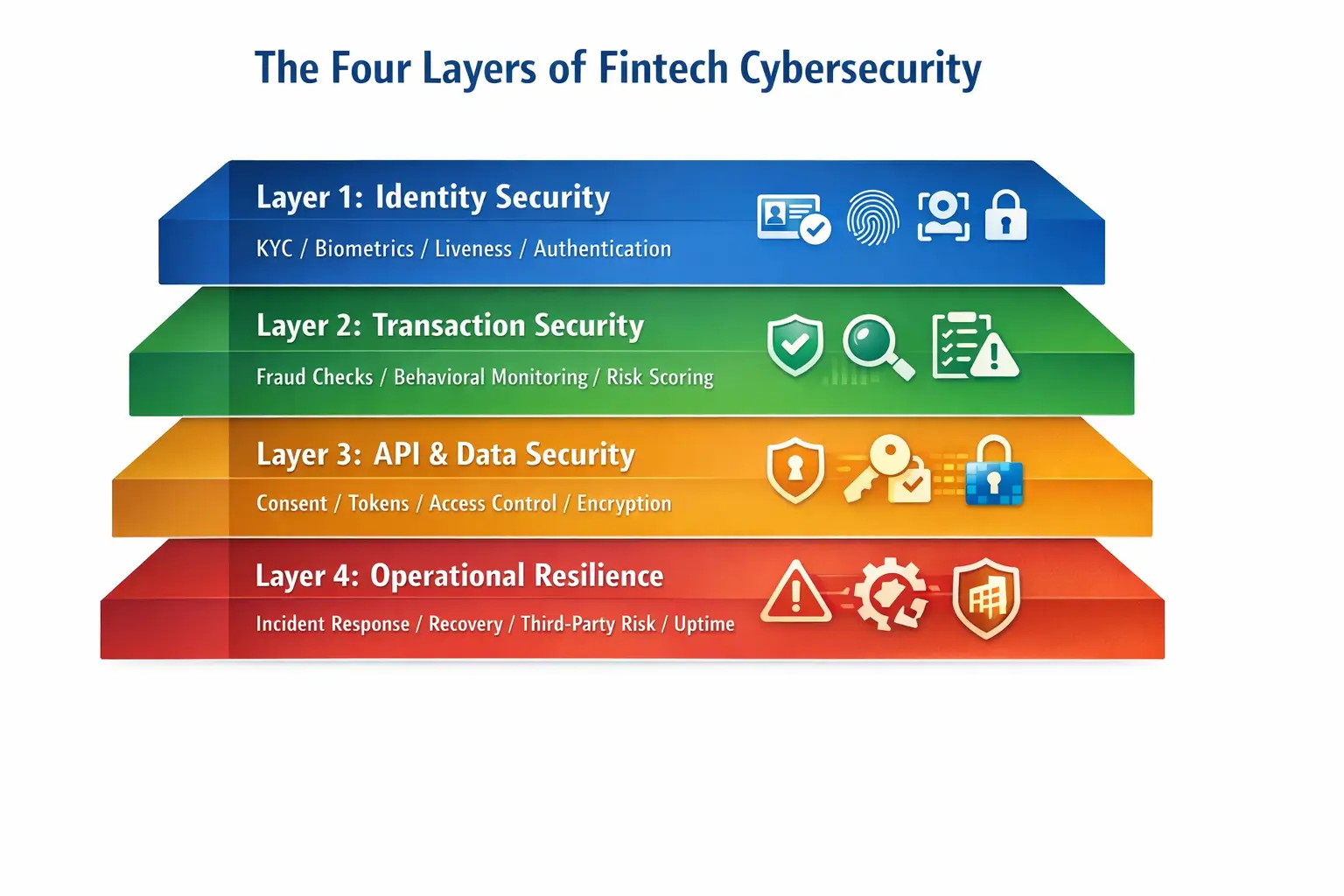

The four layers of fintech cybersecurity

A useful way to understand the topic is to stop thinking in tools and start thinking in layers.

1. Identity security

Before a fintech can protect money, it has to know who it is dealing with.

That sounds obvious, but it is getting harder. Fraudsters do not only steal real identities anymore. They mix real and fake data to create synthetic identities, use document forgery, or try to bypass onboarding with AI-generated media. In a digital onboarding flow, identity is no longer a paperwork problem. It is a live risk decision.

This is why strong fintech platforms invest in document verification, liveness checks, device intelligence, and layered KYC controls. The goal is not just to approve users fast. It is to approve the right users fast.

2. Transaction security

Even if identity checks are strong, a legitimate account can still be abused.

That is where transaction security comes in. The question is no longer only who is this user? It becomes does this payment or transfer make sense for this user right now?

A login from a familiar device followed by a normal low-value payment may be low risk. A sudden high-value transfer to a new beneficiary from an unfamiliar device is a different story. Good fintech security looks at behavior, context, timing, and pattern shifts. It does not treat every action as equal.

3. API and data security

Modern fintech runs on connections.

Banks connect to fintechs. Wallets connect to card networks. lenders connect to data providers. Open banking and embedded finance depend on APIs, tokens, permissions, and consent frameworks.

This creates speed and innovation, but it also creates new attack paths. Weak authentication, over-permissioned access, poor token handling, or broken authorization logic can expose money movement and customer data without anyone “hacking the app” in the old-fashioned sense.

That is why API security is core fintech cybersecurity, not a side topic.

4. Operational resilience

A secure fintech must do more than prevent incidents. It must survive them.

If authentication fails, payments stall. If a cloud dependency goes down, onboarding may freeze. If a critical vendor is compromised, fraud controls may become blind right when they are most needed.

This is why resilience now sits inside the cybersecurity conversation. The EU’s DORA framework is built around exactly this point: financial entities need stronger digital operational resilience, including ICT risk management, incident handling, third-party oversight, and testing.

Source: EUR-Lex summary of DORA

The biggest risks in fintech cybersecurity

A good fintech cybersecurity article should not sound like a random list of threats. The better approach is to understand the kinds of failure that actually damage digital finance.

Account takeover

This is still one of the most expensive and persistent risks. Attackers do not always need to breach a core system if they can hijack the customer instead. Stolen credentials, SIM swap attacks, phishing, malware, and social engineering can all lead to account access that looks legitimate at first glance.

Fraud at onboarding

Fast signup is good for growth, but weak onboarding can poison the platform from day one. If a fintech approves synthetic identities, mule accounts, or manipulated documents too easily, fraud is not entering through the side door. It is walking in through the front door.

Payment scams

In many cases, the user is tricked into making the payment themselves. That makes prevention harder because the transaction may technically be “authorized,” even when it is induced by deception. This is one reason payment and transfer fraud is such a serious fintech cybersecurity issue.

API misuse

When the security model around permissions, tokens, and access scopes is weak, the fintech may expose too much to the wrong system or user. In highly connected finance, security failures often travel through integrations.

Third-party concentration risk

Fintech rarely operates alone. Cloud providers, KYC vendors, fraud engines, card processors, messaging tools, and banking-as-a-service partners all sit inside the operating chain. A weakness in one dependency can become a platform-wide issue.

Where quantum computing fits into fintech cybersecurity

This is the part many articles miss.

If you talk about fintech cybersecurity today without mentioning quantum computing, you are not talking about the full future risk map.

Quantum computing is not the main cause of current payment fraud, account takeover, or API abuse. Those are immediate risks. But quantum computing matters because much of digital finance still depends on cryptographic systems that were designed for a world without large-scale quantum attacks.

The concern is simple: if quantum computers become powerful enough for relevant cryptographic attacks, some of the public-key systems used across digital finance, secure communication, authentication infrastructure, and key exchange could become vulnerable. That does not mean every fintech app is about to break tomorrow. It does mean the migration window is longer than many teams think.

This is why post-quantum planning matters now, not later. The transition will not be a single software patch. It may involve infrastructure updates, vendor coordination, cryptographic inventory work, hardware dependencies, long retention data risks, and backward compatibility challenges across financial ecosystems.

NIST finalized its first three post-quantum cryptography standards in August 2024 and has explicitly encouraged organizations to begin the transition. In March 2025, NIST also announced HQC as a backup algorithm for general encryption, showing that post-quantum preparedness is continuing to evolve. For fintech, that means cybersecurity strategy should include both today’s fraud defenses and tomorrow’s cryptographic migration path.

Source: NIST releases first finalized post-quantum encryption standards

Source: NIST selects HQC as fifth algorithm for post-quantum encryption

Why fintech security is not just about blocking attacks

A weak article on fintech cybersecurity usually turns into a checklist: use MFA, encrypt data, secure APIs, monitor fraud. None of that is wrong, but it misses the real tension inside fintech.

The real challenge is this:

How do you make a financial service feel instant and easy while still making it hard to exploit?

That is the product question behind cybersecurity in fintech.

Too much friction kills conversion. Too little friction attracts abuse. Too many false positives hurt good customers. Too much trust in automation can open the door to sophisticated fraud. The best fintechs do not solve this by choosing between security and growth. They solve it by designing risk-based trust.

That means low-risk actions stay smooth. High-risk actions trigger stronger controls. The user experience changes based on context, not on one rigid rule for everyone.

Fintech cybersecurity and open banking

Open banking made finance more connected, but it also made security architecture more visible.

Before open banking, much of financial security was hidden inside the walls of a bank. Now permissions, consent, API calls, access scopes, token flows, and data-sharing models are part of the product itself.

That changes the cybersecurity discussion. The question is no longer only whether a bank’s perimeter is strong. It is whether the right party is getting the right access to the right data for the right duration under the right consent terms.

That is a much more modern cybersecurity problem.

It is also why open banking security and fintech cybersecurity should not be treated as separate topics. They are the same story viewed from different angles: trust, access, data control, and operational accountability in connected finance.

What strong fintech cybersecurity looks like

Strong fintech cybersecurity does not always look dramatic from the outside. In fact, when it works well, it often feels invisible.

A user signs up smoothly, but document fraud detection is running underneath.

A user logs in normally, but device intelligence is being checked.

A payment goes through in seconds, but transaction monitoring has already scored the risk.

A platform suffers a disruption, but incident response and fallback processes keep the service available.

That is what maturity looks like.

Not “security theater.”

Not endless friction.

Not a vague claim that customer data is protected.

Real maturity means the fintech can identify users well, detect abnormal behavior fast, control its integrations tightly, and continue operating under pressure.

Final thoughts

The most useful way to think about fintech cybersecurity is not as a narrow technology topic, but as the trust architecture of digital finance.

It protects identities before money moves.

It checks intent while transactions happen.

It secures the connections that make fintech scalable.

It helps the platform recover when something goes wrong.

And increasingly, it has to prepare for the cryptographic future as well, including the long-term implications of quantum computing.

That is why fintech cybersecurity is not just about preventing the next breach.

It is about making digital finance credible enough to keep growing.

References

- Finteconomix: Can Quantum Computers Break RSA Used in Payment Systems?

- FTC: New data show reported fraud losses reached $12.5 billion in 2024

- EUR-Lex: Digital operational resilience for the financial sector (DORA)

- NIST: First finalized post-quantum encryption standards released

- NIST: HQC selected as fifth algorithm for post-quantum encryption