Why fraud detection in banking feels different now

A few years ago, fraud detection in banking mostly meant catching a stolen card or blocking an unusually large transaction. Today, the picture is much messier. A scammer may impersonate a bank by phone, trick a customer into sharing a one-time code, log in from a new device, change account details, and move money out within minutes. In other cases, the fraud starts even earlier with a fake identity used to open an account that looks completely normal for months. Regulators and central bank-related bodies have been warning that fraud is becoming more digital, more automated, and more closely tied to identity abuse and social engineering.

That is what makes bank fraud detection interesting. Banks are not only watching transactions anymore. They are watching devices, logins, identity data, behavior patterns, account changes, and payment flows at the same time. The real story is not “a suspicious transaction was blocked.” The real story is that fraud detection has become a live risk engine running behind every login, transfer, and onboarding flow. ECB Banking Supervision says banks are increasingly using AI for fraud detection because it improves real-time monitoring and pattern recognition across large data sets.

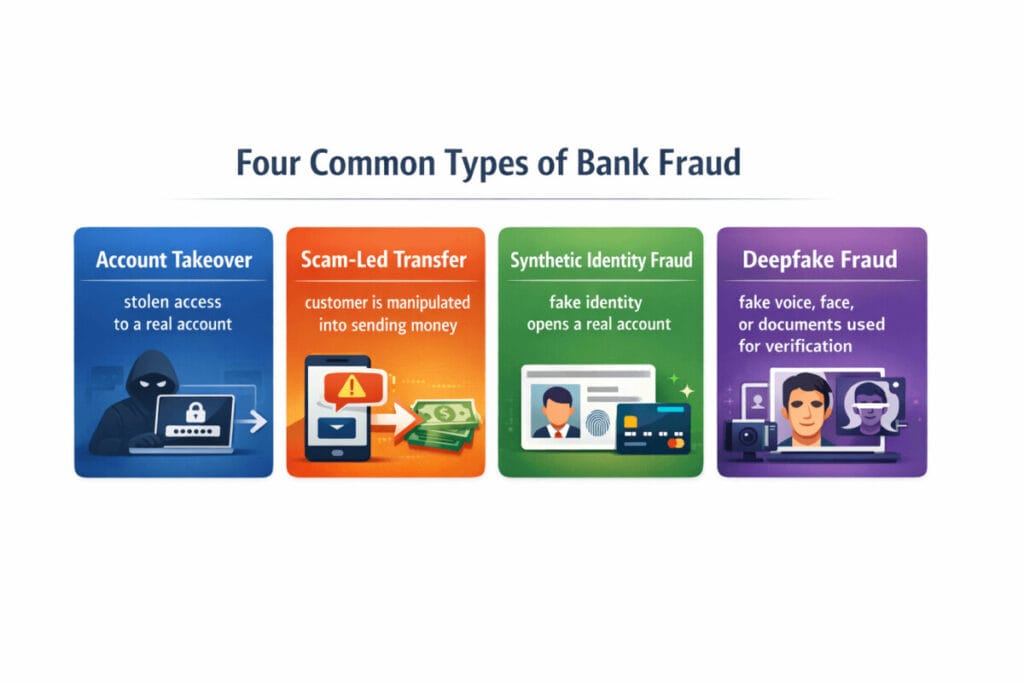

A quick look at the main fraud patterns banks care about

| Fraud type | What it looks like | Why it is hard to catch | What banks watch |

|---|---|---|---|

| Account takeover | A criminal gets into a real customer account and starts moving money | The account is real, so the activity may look partly legitimate at first | New device, odd login behavior, address change, new payee, fast transfer pattern |

| Bank impersonation / scam-led transfer | A customer is tricked into “authorizing” a payment after a fake fraud alert | The customer may appear to approve the payment | Call patterns, payee risk, sudden urgency, unusual destination account |

| Synthetic identity fraud | A fake person is built using real and invented data, then used to open accounts or obtain credit | It can look normal for months or years | Thin credit history, inconsistent profile data, linked phone/IP/device signals |

| Deepfake-enabled fraud | Fake voice, video, or manipulated identity documents are used in onboarding or authentication | The evidence may look highly convincing | Liveness checks, document validation, biometric mismatch, device and geolocation mismatch |

The reason banks need multiple layers is simple: fraud does not always begin at the payment stage. Sometimes it starts at account opening, sometimes at login, and sometimes with social engineering that makes the customer act on the fraudster’s behalf. FinCEN has warned about deepfake media targeting financial institutions, while the Federal Reserve ecosystem has repeatedly highlighted synthetic identity and account takeover as major threats.

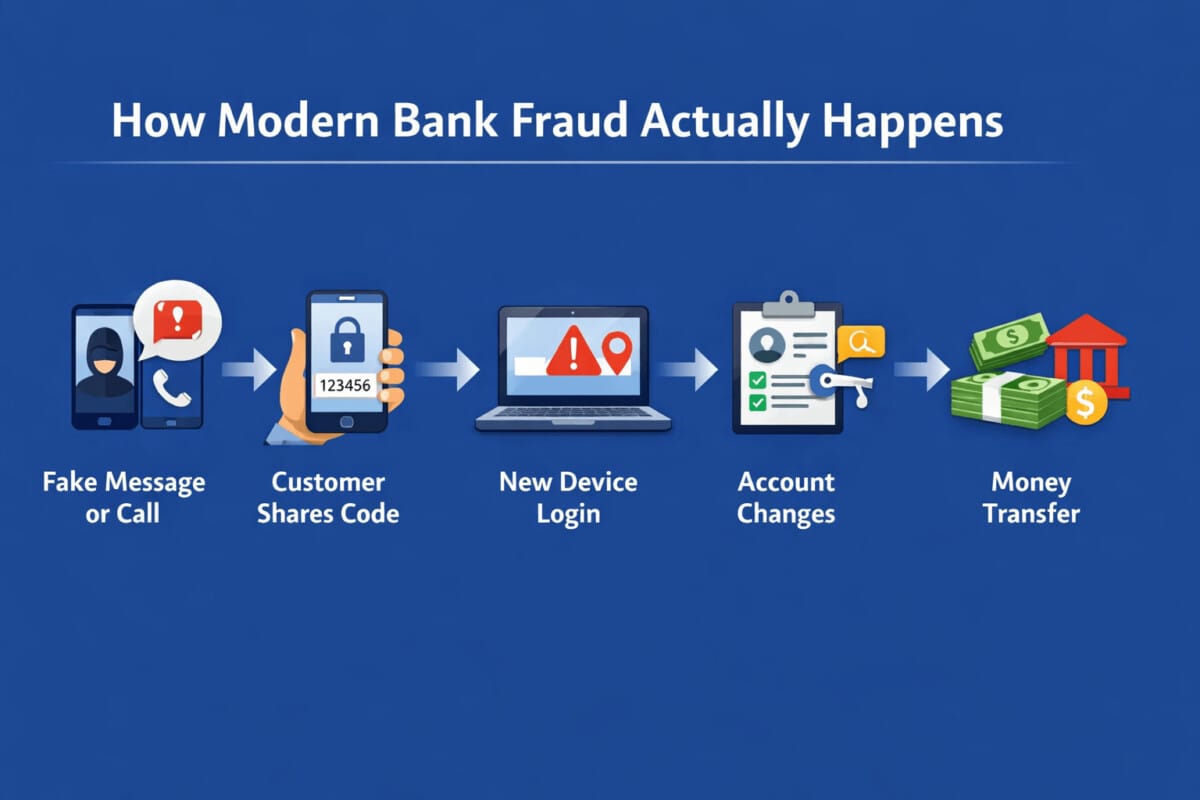

Example 1: “We detected fraud on your account” — but the message is the fraud

This is one of the most believable scams because it exploits the exact thing customers already worry about: security.

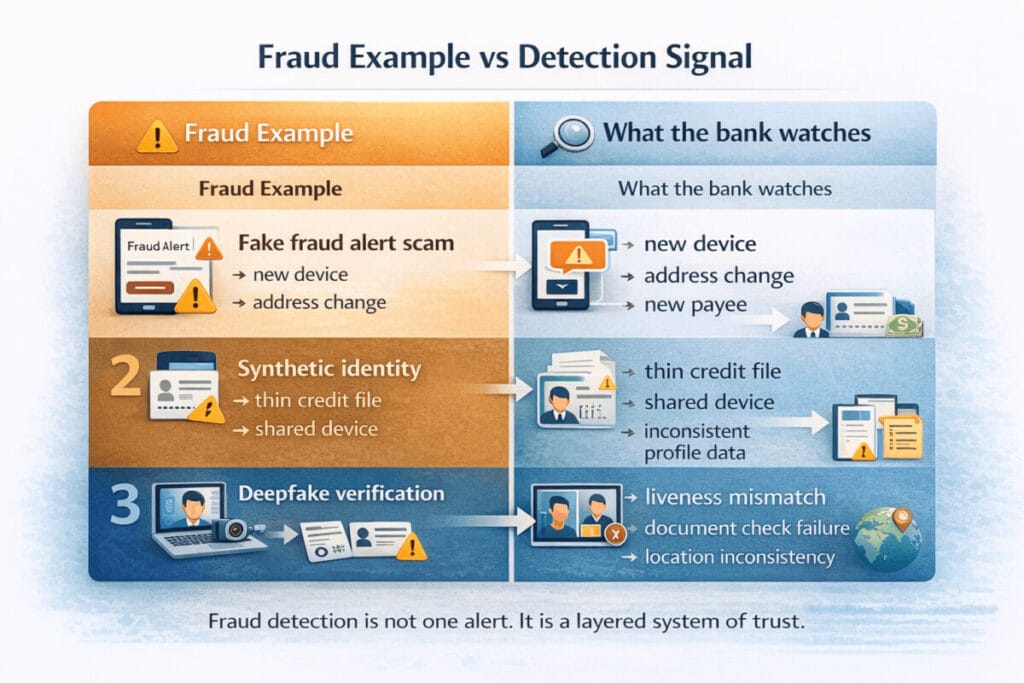

A customer receives a text, call, or email that appears to come from their bank. The message says there has been suspicious activity, and the customer needs to verify their identity immediately. The scammer asks for login details, card information, or a texted code. Once they get it, they use that information to access the real account and initiate transfers. CFPB gives examples where a fraudster pretends to be a representative from the consumer’s financial institution and tricks the consumer into sharing login information, a confirmation code, or debit card details that are then used to initiate an EFT. FedPayments Improvement also notes that spoofing makes fake fraud alerts look as if they came from a trusted institution.

How a bank may detect this

The transaction itself may not be the first clue. The earlier clues are often stronger.

A bank may notice:

- a login from a new device

- a sudden change of home address or contact details

- a password reset followed by a high-risk action

- a transfer to a new receiver account

- a large outbound payment shortly after the account profile changes

FedPayments Improvement gives a concrete example: if a new device logs into an account, then the home address changes, and soon after the user tries to transfer a large share of funds to a new receiver, that sequence should trigger alerts and extra verification.

In plain language, the bank is not only asking, “Is this payment strange?” It is asking, “Does the story of this session make sense?”

Example 2: A fake person opens a real account

Synthetic identity fraud is much more interesting than ordinary identity theft because there is often no obvious victim who notices right away. Instead of stealing one person’s full identity, a fraudster pieces together real and fake data to create someone who does not actually exist. Federal Reserve-related materials describe synthetic identity fraud as fraud that combines false and sometimes real information to establish a new identity and build a credit record under that synthetic profile. Boston Fed explains that criminals often use these identities to apply for credit cards or open accounts, giving them access to the banking system and places where they can move money through.

One FedPayments use case describes two fraudsters who created more than 750 synthetic identities and used some of them to fraudulently obtain millions of dollars from an emergency relief loan program. That example is useful because it shows the scale synthetic identity fraud can reach once the fake identities have been cultivated long enough to appear legitimate.

How a bank may detect this

This is where fraud detection gets subtle. Synthetic identities often behave carefully at first.

Banks may look for signals such as:

- very limited or brief credit history

- a profile built mostly around unsecured credit

- inconsistencies across application data

- phone number ownership that does not match the applicant

- IP address or geolocation that does not fit the stated address

- several accounts linked by common devices, payment sources, addresses, or contact points

FedPayments materials say any inconsistency in the customer’s credit profile warrants more investigation, and list factors such as limited credit history, transaction activity patterns, payment source, credit line growth, and shared data elements across accounts as potential detection criteria. Another Federal Reserve toolkit item notes that online information, phone-number ownership checks, geolocation, and IP-address comparisons can help identify synthetic identities during onboarding and portfolio review.

This is why banks try to catch synthetic fraud before the relationship is opened. Once the fake customer is on the books and behaves normally for a while, detection becomes much harder.

Example 3: Deepfake fraud turns identity checks into a moving target

The fraud problem is not just stolen passwords anymore. It is increasingly about manufactured credibility.

FinCEN issued an alert in November 2024 on fraud schemes involving deepfake media targeting financial institutions. The alert warns that deepfake content can be used alongside manipulated or generated identity documents to exploit account opening, account access, and transaction processes. That matters because many digital banking workflows rely on remote identity verification, document capture, facial matching, and video-based verification.

What makes this useful for your article is the storytelling angle. The scary part is not just that a fake face or voice exists. The scary part is that it can be inserted into processes that used to feel trustworthy:

- video onboarding

- customer support verification

- selfie-based liveness checks

- voice confirmation

- document submission

How a bank may detect this

A bank usually does not rely on one signal. It layers them.

That can include:

- document authenticity checks

- liveness detection

- biometric comparison

- device fingerprinting

- geolocation consistency

- session behavior analysis

- cross-checking known fraud-linked data points

FinCEN’s alert and Federal Reserve materials together point toward the same lesson: when fraudsters can generate convincing media, banks need identity validation plus behavioral and device-level monitoring, not just one visual check.

Example 4: The customer clicks “send” — but it is still fraud

One reason modern fraud is so difficult is that the customer may appear to authorize the payment. In Europe, ECB supervisory commentary has noted that manipulation of payers accounted for over half of fraudulent credit transfers, typically through social engineering enabled by cyber capabilities. That is a striking point because it shows how much fraud now depends on persuasion, not only technical compromise.

This makes for a strong article point: some of the most damaging fraud today is not “the bank was hacked.” It is “the customer was manipulated.”

How a bank may detect this

Banks may look for a combination of:

- unusual urgency

- a first-time payee

- a high-value transfer outside the customer’s normal pattern

- payments to accounts already associated with scam typologies

- sudden changes after a suspicious inbound call or login recovery flow

This is also where fraud detection meets customer experience. If the bank interrupts too many legitimate transfers, people get frustrated. If it interrupts too few, losses rise.

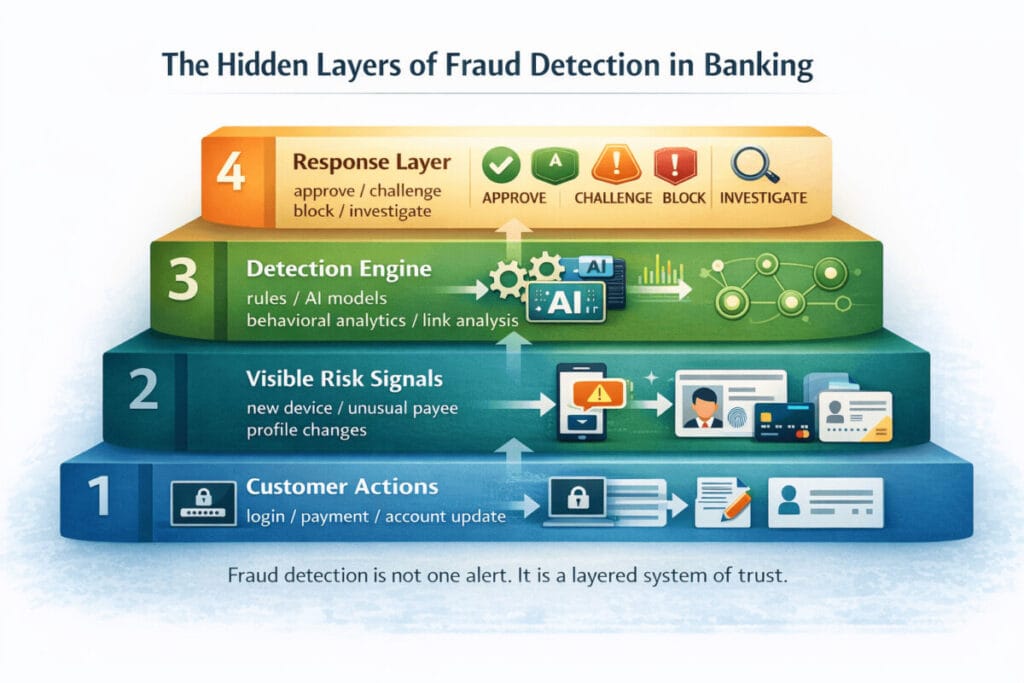

What banks are really doing behind the scenes

When people hear AI fraud detection in banking, they often imagine a single model deciding whether a transaction is fraudulent. In reality, banks usually combine multiple layers.

| Layer | What it does | Example signals |

|---|---|---|

| Rules | Catches known bad patterns fast | Large transfer to new payee right after password reset |

| Behavioral analytics | Compares activity to the customer’s normal behavior | Typing rhythm, login timing, usual payment values |

| Device intelligence | Evaluates the risk of the device and session | New device, emulator, risky browser fingerprint |

| Identity validation | Tests whether the claimed identity is believable | Document checks, phone ownership, IP/address mismatch |

| Network / link analysis | Finds hidden connections across accounts | Shared device, shared funding source, repeated receiver |

| Human investigation | Reviews borderline or high-impact cases | Case analyst review, callback, temporary hold |

ECB Banking Supervision says banks are using AI models such as decision-tree-based approaches and neural networks for fraud detection, with humans still involved either in final decision-making or ex-post oversight. That is important because the best anti-fraud systems are not fully automatic black boxes. They are layered systems where models, rules, and investigators work together.

Why this makes a better story than “banks use AI”

The most interesting part of fraud detection in banking is not that banks use machine learning. It is that they are trying to solve a very human problem with data.

A scammer impersonates trust.

A synthetic identity imitates legitimacy.

A deepfake imitates presence.

An account takeover imitates the customer.

So the bank’s job is really to ask one question over and over again:

Does this behavior fit the identity, the device, the account history, and the timing — or is something just slightly off?

That is why the best fraud detection systems do not focus on just one transaction. They reconstruct the whole story around it.

Final thoughts

Modern fraud detection in banking is not really about catching one suspicious transaction.

It is about spotting a pattern before the damage is done.

A fake fraud alert.

A new device login.

A sudden profile change.

A first-time payee.

A transfer that looks ordinary on its own, but suspicious when the full sequence is put together.

That is what makes banking fraud harder now. The fraud often does not begin with the payment itself. It begins with identity abuse, social engineering, account access, or a small inconsistency that only becomes obvious when multiple signals are connected.

This is also why banks cannot rely on simple rule-based checks alone. Modern fraud detection increasingly depends on layered monitoring across identity, behavior, devices, account activity, and payment patterns. The real goal is not just to block bad transactions. It is to decide, as quickly as possible, whether the story behind the activity makes sense.

In that sense, fraud detection is really a trust system.

Banks are constantly asking:

Is this the real customer?

Is this normal behavior?

Does this payment fit the account history?

Or is this a carefully staged performance designed to look legitimate?

The banks that handle fraud best will not just have better models. They will have better context, better coordination, and better judgment about how risk actually unfolds in digital finance.

Fraud detection in banking is no longer a back-office control. It is now part of the invisible infrastructure that makes digital banking possible.

References

- ECB Banking Supervision, AI use cases in banking: https://www.bankingsupervision.europa.eu/press/supervisory-newsletters/newsletter/2025/html/ssm.nl251120_1.en.html

- ECB speech on fraud patterns and manipulation of payers: https://www.bankingsupervision.europa.eu/press/speeches/date/2026/html/ssm.sp260203~672ce5d5ff.en.html

- FinCEN alert on deepfake fraud targeting financial institutions: https://www.fincen.gov/system/files/shared/FinCEN-Alert-DeepFakes-Alert508FINAL.pdf

- CFPB Electronic Fund Transfers FAQs: https://www.consumerfinance.gov/compliance/compliance-resources/deposit-accounts-resources/electronic-fund-transfers/electronic-fund-transfers-faqs/

- Federal Reserve Bank of Boston, synthetic identity fraud and GenAI: https://www.bostonfed.org/publications/six-hundred-atlantic/interviews/synthetic-identity-fraud-how-ai-is-changing-the-game.aspx