Money does not move on technology alone. It moves on shared rules.

A card payment looks simple. A bank transfer feels instant. A securities transaction appears to be nothing more than numbers changing on a screen. But behind every smooth financial experience sits a much larger system of agreements. Banks, payment providers, market infrastructures, regulators, and software systems all need to understand data in the same way, use the same definitions, and trust the same processes.

That is where standards come in.

And one of the most important places where those standards are shaped is ISO/TC 68.

ISO/TC 68 is the ISO technical committee for financial services. That may sound dry at first, but its role is surprisingly important. It helps create the common language that allows financial systems to work across institutions, across technologies, and often across borders. If modern finance is a global network, ISO/TC 68 is part of the group writing the grammar.

Why does finance need international standards at all?

Finance is not just about moving money. It is about moving data, instructions, identities, security information, and legal meaning.

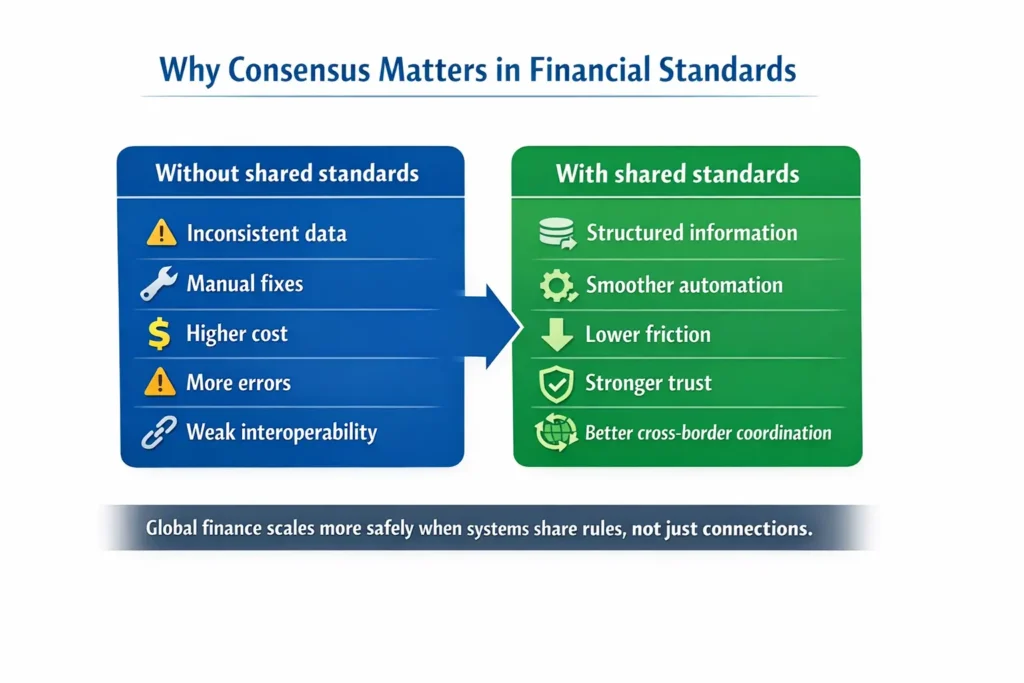

If one institution labels a transaction one way, another records it differently, and a third expects an entirely different format, automation starts to break down. Systems need manual intervention. Exceptions increase. Costs rise. Errors become more likely. Cross-border activity becomes slower and more expensive.

Standards reduce that friction.

They make it easier for institutions to exchange information consistently. They improve interoperability. They help support automation. They reduce misunderstanding between systems that were never built by the same company, in the same country, or under the same regulatory environment.

In that sense, standards are not a decorative layer on top of finance. They are part of the infrastructure underneath it.

So what exactly is ISO/TC 68?

ISO/TC 68 is the ISO committee responsible for standards in financial services. Its scope is broad. It is not only about payments, and it is definitely not only about one message format or one corner of banking.

It covers core banking, payments, securities and capital markets, card processing, information exchange, reference data, and security topics related to financial services. That breadth matters. Finance is deeply interconnected. Payment systems rely on secure data exchange. Market infrastructures rely on shared identifiers. Financial institutions rely on common definitions and structured information. Standards in one area often affect many others.

That is why ISO/TC 68 is better understood not as a niche committee, but as a foundational structure in global finance.

Who takes part in ISO/TC 68?

One of the most interesting things about ISO/TC 68 is that it reflects international participation rather than one-country control.

International standards are not supposed to be one market’s preferred habits exported to everyone else. They are developed through participation by national standards bodies, with input that may include central banks, regulators, financial institutions, market infrastructures, industry associations, and technical experts.

That matters because finance is not the same everywhere.

Some markets are card-heavy. Others are more account-to-account. Some financial systems are built around strong domestic rails. Others are shaped by large international banking networks. Some jurisdictions have stricter regulatory expectations in certain areas. Others prioritize different operational needs. A global standard that ignores those realities would not last very long.

That is why the process matters almost as much as the final document. Standards in finance need to be technically sound, but they also need to survive contact with real markets.

What does the structure of ISO/TC 68 look like?

At a high level, ISO/TC 68 is organized into major subcommittees. A simple way to understand them is this:

| Subcommittee | Main focus | Plain-English meaning |

|---|---|---|

| SC 2 | Financial services security | The rules that help financial systems stay safe and trusted |

| SC 8 | Reference data for financial services | Shared data elements everyone needs to define the same way |

| SC 9 | Information exchange for financial services | How systems and institutions communicate with each other |

This structure tells you something important. Finance is not treated as a single stream of transactions. It is treated as a system that depends on security, common data, and reliable information exchange.

That is a much smarter way to think about financial infrastructure.

A payment is not just a payment. It is also identity, authorization, message structure, reconciliation, and trust. A securities process is not just an asset changing hands. It is also data consistency, market convention, legal clarity, and operational coordination. ISO/TC 68 sits much closer to that real-world complexity than many people realize.

What kind of work does ISO/TC 68 actually do?

This is where the committee becomes much more practical than people expect.

ISO/TC 68 does not exist to produce abstract theory. It works on standards that affect how financial services operate in practice. That can include security frameworks, card-related security topics, data definitions, structured information exchange, identifiers, and newer questions emerging from changes in technology and financial architecture.

In recent years, the broader TC 68 structure has also shown interest in areas such as digital currencies, artificial intelligence, decentralized finance, identification, and sustainable finance. That does not mean it is chasing every trend. It means the committee is watching how finance is changing and asking a serious question: what common rules will global systems need next?

That is an important distinction.

A standard-setting body should not exist to sound fashionable. It should exist to make emerging financial systems more understandable, more interoperable, and more resilient. That is where ISO/TC 68 matters.

How does a financial standard get made?

This is one of the most overlooked parts of the topic, and also one of the most fascinating.

A standard does not appear because someone had a good idea on a Tuesday.

It usually begins with a recognized need. Maybe there is inconsistency across markets. Maybe a new financial activity lacks a common framework. Maybe existing practices are causing friction, confusion, or security weakness. A proposal is raised. Drafting begins. Experts review the text. National members comment. Revisions are made. More comments follow. Voting takes place. The document moves through formal stages until it is ready for approval and publication.

The simplified flow looks like this:

| Stage | What it means | What is really happening |

|---|---|---|

| Proposal | A new standard is suggested | Someone says the market needs a common rule here |

| Drafting | Experts prepare a working text | The first serious version is built |

| Committee review | Members comment and revise | Markets push back, refine, and negotiate details |

| Broader voting | Wider member review and approval | The draft is tested for international acceptability |

| Final publication | The standard is issued | The rule becomes official |

In ISO language, people often refer to stages such as CD, DIS, and FDIS. But what matters more than the abbreviations is the logic behind them: a standard must be reviewed, challenged, improved, and accepted before it can become something global markets rely on.

That is why standards can take time. They are not just technical documents. They are negotiated foundations.

Why is consensus such a big deal?

Because finance is not a laboratory. It is a live system.

A technically elegant idea may still fail if it does not fit regulatory realities, operational practices, legal frameworks, or market structure. A standard that works beautifully in one jurisdiction may create problems in another. So international financial standards cannot be based on elegance alone. They need breadth. They need durability. They need enough shared support to work across different environments.

Consensus is not about making a document bland. It is about making it usable.

That is especially important now. Financial innovation moves fast, but not everything that moves fast becomes foundational. New tools, new rails, new data models, and new forms of digital finance only scale if institutions can actually use them together. In other words, innovation often gets the headlines, but standards determine whether innovation becomes infrastructure.

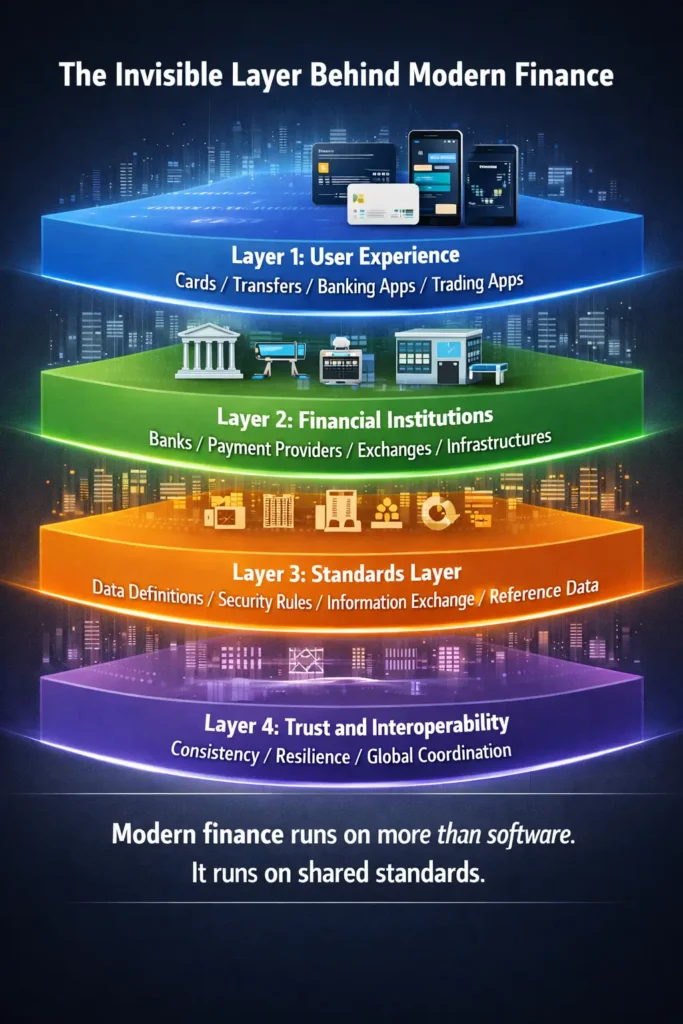

Why does ISO/TC 68 matter beyond specialists?

Because the visible side of finance depends on the invisible side.

Consumers see apps, cards, transfers, wallets, and confirmations. Institutions see messages, controls, identifiers, exception handling, liability, and system compatibility. Policymakers see resilience, interoperability, and trust. ISO/TC 68 sits much closer to that second and third layer than the first, but the first layer depends on it anyway.

If the standards underneath finance are weak, fragmented, or outdated, the user experience eventually suffers. Costs rise. Cross-border processes stay clumsy. Security becomes harder to maintain. Integration becomes slower. Innovation becomes more expensive than it should be.

If the standards are strong, something interesting happens: the system starts to feel simple.

That is usually the sign that the invisible architecture is doing its job.

A useful way to think about ISO/TC 68

It helps to compare finance to a city.

Most people notice the buildings, the shops, the traffic, and the lights. But a city only works because of deeper systems: roads, water, electricity, zoning rules, maps, and engineering standards.

Finance works in much the same way.

Most people see payments, transfers, trading apps, banking screens, and account balances. But underneath those experiences are shared structures that make the whole system understandable and operable. ISO/TC 68 is part of that underneath.

It is not the storefront. It is closer to the street grid.

The bigger meaning of ISO/TC 68

ISO/TC 68 matters because global finance cannot grow on custom connections forever.

At a small scale, institutions can build one-off links, one-off formats, and one-off workarounds. At a global scale, that becomes expensive, fragile, and inefficient. Standards are what allow a system to expand without collapsing under its own complexity.

That is the real value of ISO/TC 68.

It helps financial services move from isolated systems toward shared understanding. It helps different markets speak with less friction. It helps trust become operational rather than merely aspirational. And it reminds us that in finance, the most important architecture is often the part nobody sees.

Money moves quickly. Trust does not.

Trust is built slowly, through common rules, consistent definitions, and processes that different institutions can rely on. That is why ISO/TC 68 matters. It is not the loudest part of finance, but it helps make modern finance possible.

Quick summary

| Question | Answer |

|---|---|

| What is ISO/TC 68? | The ISO technical committee for financial services |

| Why does it exist? | To support common standards across financial systems and markets |

| Who participates? | National standards bodies and experts connected to financial services |

| What does it cover? | Security, reference data, information exchange, and broader financial service standards |

| Why is it important? | It supports interoperability, efficiency, trust, and scalable global finance |

References

Finteconomix : Why Financial Standards Matter / What Mismatched Power Outlets Teach Us About Finance

https://finteconomix.com/why-financial-standards-matter-what-mismatched-power-outlets-teach-us-about-finance/

ISO/TC 68 official committee page

https://www.iso.org/committee/49650.html

ISO/TC 68 official site

https://committee.iso.org/home/tc68

ISO stages and resources for standards development

https://www.iso.org/stages-and-resources-for-standards-development.html

ISO/TC 68 Newsletter, February 2026

https://committee.iso.org/files/live/sites/tc68/files/newsletters/ISO-TC68_27.FEBRUARY.2026.pdf