Why the acquirer merchant relationship matters more than most businesses think

In payments, people often focus on the visible moment. A customer enters card details, taps a button, and sees a message that says the payment is complete. It feels simple. But anyone who has spent time around payment operations knows that the visible part is only the surface. The more important question is what happens underneath that moment, and that is exactly where the acquirer merchant relationship starts to matter.

The term acquirer merchant is slightly awkward, and in the industry you will often see merchant acquirer or acquiring bank instead. But the real issue behind the keyword is clear. Businesses want to understand who actually helps them accept card payments, who manages the relationship behind settlement, and who stands between the merchant and the wider card payment infrastructure. An acquirer, also called an acquiring bank, is the financial institution that processes card payments for the business and routes them through the card networks to the issuing bank.

That definition is useful, but it does not fully explain why this topic becomes so important once a business grows. The best way to think about the acquirer merchant relationship is not as a technical label, but as a commercial relationship that affects how reliably a business turns customer intent into real, settled revenue.

What an acquirer does for a merchant

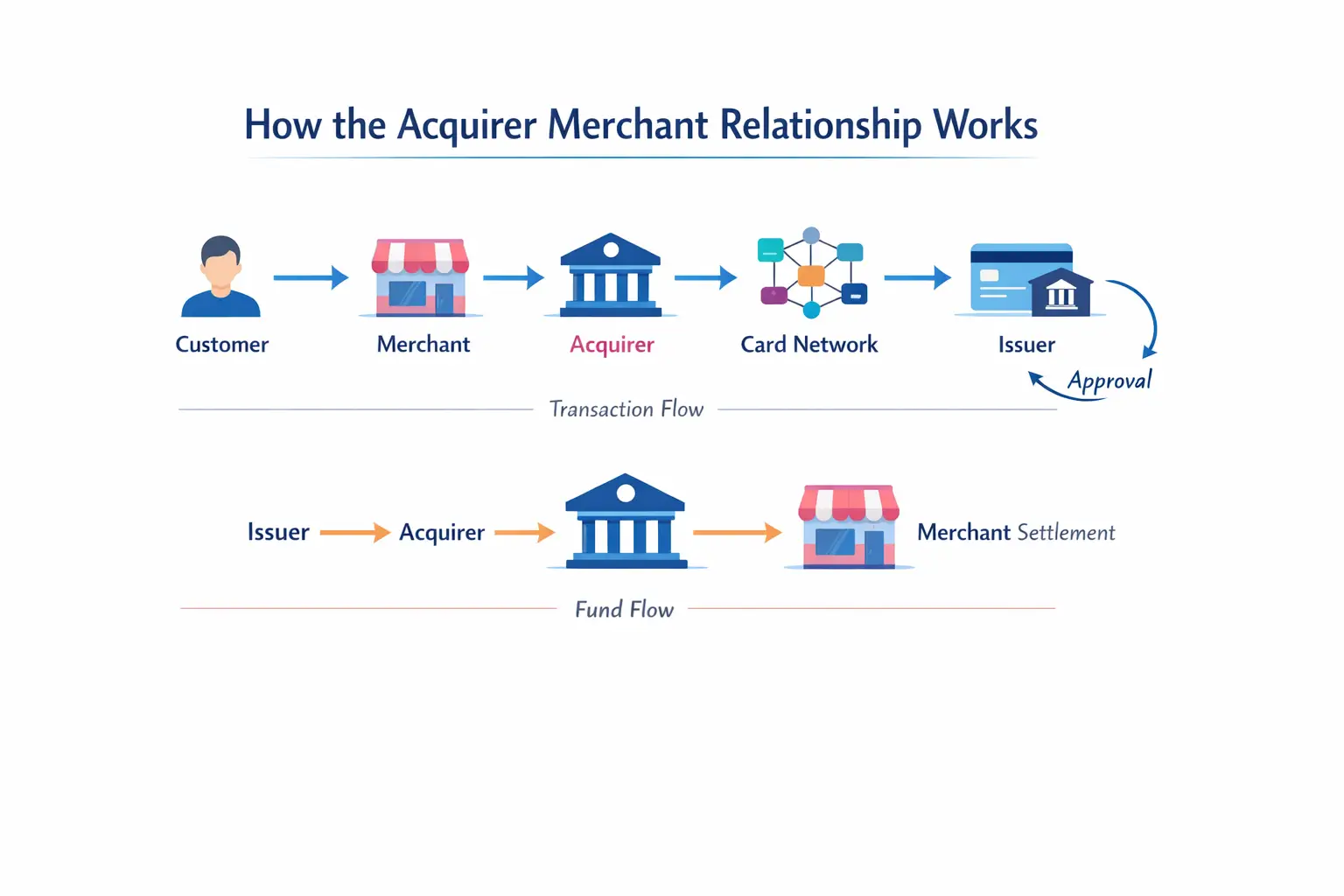

At the most basic level, the merchant is the business selling goods or services, and the acquirer is the institution that enables that business to accept card payments. The acquirer processes those transactions, sends them through the network flow, and supports settlement into the merchant’s account. Stripe explains that the acquirer represents the business side of the transaction and helps ensure that money from the issuer is deposited into the business’s account.

That sounds straightforward, but in practice the acquirer’s role reaches much further than simple transaction handling. The acquirer is closely tied to merchant account management, underwriting, settlement, and operational risk. Stripe’s payment processor versus merchant acquirer explanation notes that the processor handles the secure movement of transaction data, while the acquirer manages the merchant account, works with the issuing bank on authorization, and facilitates settlement of funds.

This is why I think many businesses misunderstand payments in the early stage. They assume card acceptance is mainly a front-end problem. They worry about checkout design, payment buttons, and customer friction. Those things matter, of course. But when payments begin to scale, the more serious questions often sit behind the interface. How stable is settlement? How strict is underwriting? How exposed is the business to disputes? How well does the setup support international growth? Those are acquirer merchant questions, even if the business does not describe them that way.

The simplest way to understand the payment structure

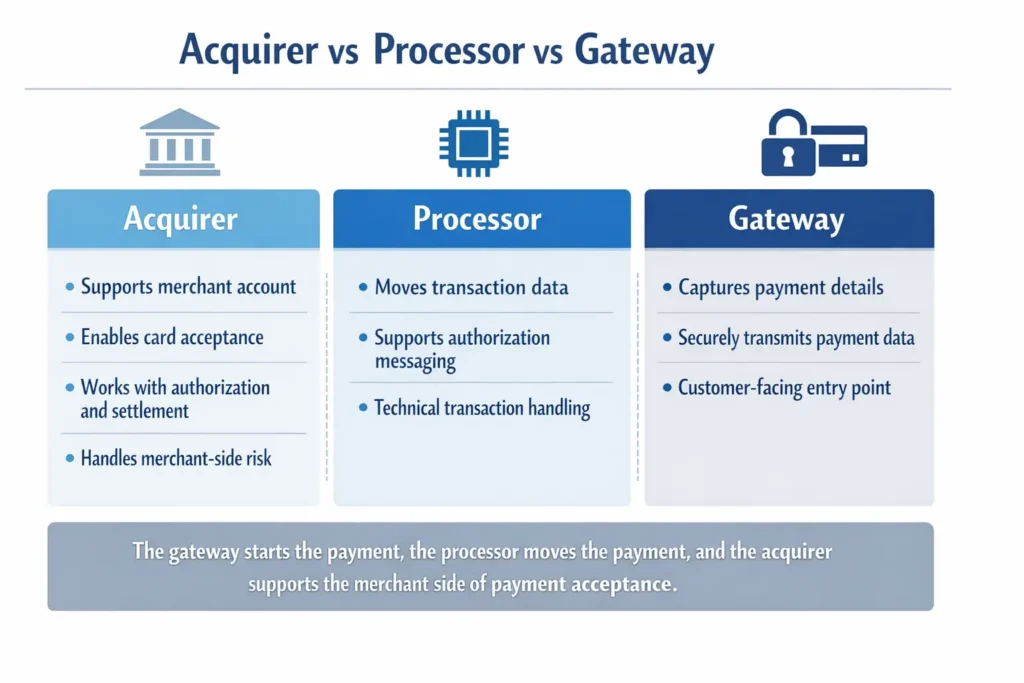

A clean table helps make the roles easier to remember.

| Role | Main function |

|---|---|

| Merchant | Sells goods or services to the customer |

| Acquirer | Enables the merchant to accept card payments and receive settled funds |

| Processor | Handles the secure transmission and processing of transaction data |

| Issuer | The customer’s bank that approves or declines the payment |

| Card network | Connects participants and governs the card transaction framework |

This is one of those areas where the payment industry can sound more complicated than it needs to be. In reality, the most important distinction is simple. The merchant sells. The issuer represents the customer’s account. The acquirer represents the business side of card acceptance. The processor helps move transaction data through the system.

Once you see that clearly, the acquirer merchant relationship becomes much easier to understand.

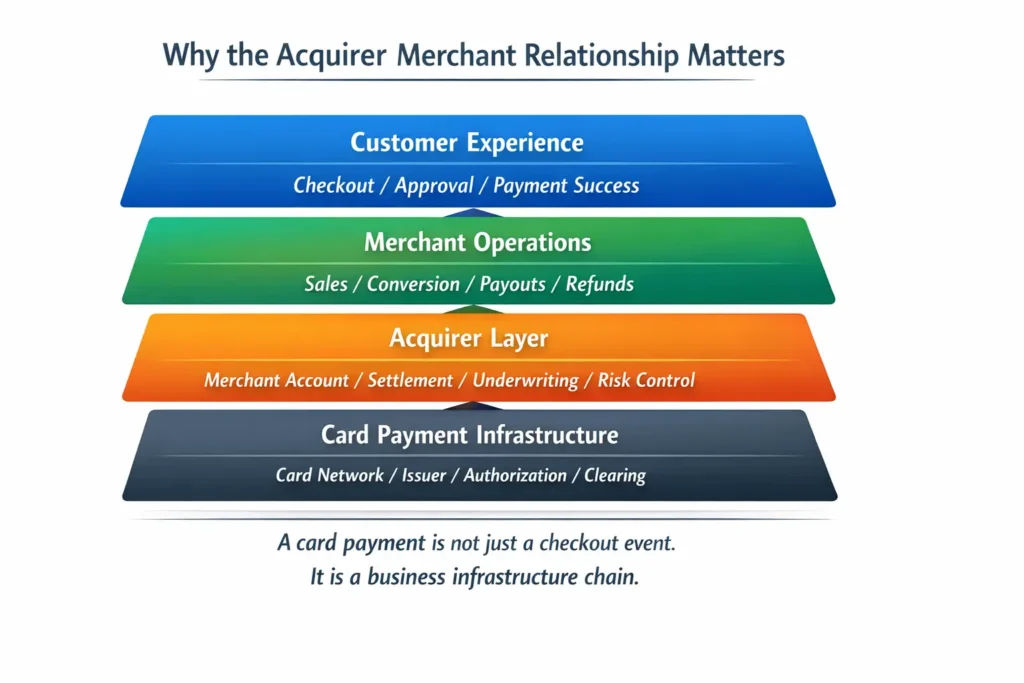

Why the acquirer merchant relationship is not just back-office plumbing

This is where the topic gets more interesting.

In a healthy payment setup, the acquirer stays mostly invisible. Transactions flow smoothly. Funds arrive on time. The merchant rarely thinks about the relationship in any deep way. But when the setup is weak, the acquirer becomes impossible to ignore. Suddenly there are payout delays, risk reviews, rolling reserves, higher scrutiny, or payment acceptance problems in certain markets.

That is why I tend to think of the acquirer merchant relationship as one of the hidden pressure points in commerce. It does not attract much attention when everything is working. But when the business starts expanding, changing models, entering new geographies, or facing more fraud pressure, the quality of that relationship becomes much more obvious.

This is especially true in online commerce. A merchant selling domestically with low risk may barely notice the acquiring layer. A merchant running subscriptions, travel services, digital goods, or cross-border payments may feel it every week. The same card rails can look stable for one business and highly sensitive for another. That is not just a payments detail. It is a business reality.

Acquirer merchant and settlement: where revenue becomes cash

One reason this topic matters so much is that it sits close to the difference between sales and actual cash receipt.

The Office of the Comptroller of the Currency describes merchant processing as the settlement of card sales transactions for merchants and notes that acquiring banks usually pay merchants by initiating ACH credits to merchants’ deposit accounts. The OCC also explains that merchant processing is separate from card issuing and involves collecting sales information, collecting funds from the issuing bank, and paying the merchant.

That point is more important than it sounds. Many founders and operators spend a lot of time thinking about revenue, but not enough time thinking about the path from approved transaction to available cash. In practice, the acquirer merchant relationship sits directly in that path. It shapes how reliably payment acceptance turns into business liquidity.

From a payments specialist’s perspective, this is one of the most overlooked lessons in commerce infrastructure. A strong payment setup is not just about accepting a card. It is about turning accepted transactions into stable cash flow under real operational conditions.

Why underwriting and risk change the merchant experience

Another reason merchants eventually care about acquiring is that acquiring is not just a processing function. It is also a risk function.

Stripe explains that acquiring banks, also called merchant acquirers, are responsible for underwriting merchant accounts, assessing business risk, and ensuring compliance. This matters because not all merchants look the same from a risk perspective. A local retailer, a marketplace, a subscription service, and a high-chargeback digital business do not present the same acquiring profile.

That is where payment operations become much more human than people expect. Behind the technical flow is a judgment layer. Is this merchant stable? Is the product category risky? Are the refund patterns normal? Is the cross-border transaction behavior expected? Can the business scale without creating unacceptable exposure?

Merchants often discover this only when something changes. Maybe they launch in a new market. Maybe their chargeback rate climbs. Maybe their average ticket size jumps. Maybe they move into a business category that the acquiring side treats more cautiously. At that point, the acquirer merchant relationship stops feeling like a background contract and starts feeling like a real commercial constraint.

Acquirer merchant versus processor and gateway

A processor manages the authorization flow and the secure transfer of transaction data, while the acquirer manages the merchant account, coordinates with the issuing bank, and supports settlement. A gateway, meanwhile, is generally the secure digital entry point that transmits payment information. Stripe’s resources make clear that these functions are closely related but not identical.

This distinction matters because merchants often buy payment services as bundled products and assume all roles are the same. In reality, even when one provider offers an integrated experience, the acquiring function still exists underneath the surface. That is why the acquirer merchant relationship remains important even in modern all-in-one payment stacks.

Why this matters for growing online businesses

The more a business grows, the more the acquiring layer tends to matter.

A small merchant may care mainly about getting paid. A growing merchant starts caring about approval rates, payout timing, chargeback handling, and expansion support. An international merchant starts caring about local acquiring, issuer behavior, and cross-border efficiency. Stripe’s local and global acquiring materials explain that acquiring structures can shape how businesses accept and process payments across markets.

This is the point where payment infrastructure becomes strategic rather than administrative.

I have always thought this is one of the biggest mindset changes in payments. At first, merchants see payments as a necessary utility. Later, they begin to understand that payments are part of business design. The acquirer merchant relationship is a good example of that shift. It begins as a technical necessity and ends up becoming a commercial advantage or a commercial weakness, depending on how well it fits the business model.

The real takeaway

The best answer to the keyword acquirer merchant is not just a short definition.

Yes, the acquirer is the institution that helps the merchant accept card payments and receive funds. That is true. But the more useful insight is that the acquirer helps translate customer payment intent into approved, routed, settled, and risk-managed business revenue.

That is why this relationship matters so much. It affects not only whether a merchant can accept cards, but how well the merchant can grow, how resilient the payment flow is under pressure, and how cleanly revenue becomes cash.

In other words, the acquirer merchant relationship is not just part of the payment system. For many businesses, it is one of the quiet foundations of the business itself.

References

- Finteconomix : Payment Gateway vs Payment Processor — https://finteconomix.com/payment-gateway-vs-payment-processor/

- Stripe: Payment processor vs. merchant acquirer — https://stripe.com/resources/more/payment-processor-vs-merchant-acquirer

- Office of the Comptroller of the Currency: Merchant Processing, Comptroller’s Handbook — https://www.occ.treas.gov/publications-and-resources/publications/comptrollers-handbook/files/merchant-processing/pub-ch-merchant-processing.pdf