Financial Standards Matter

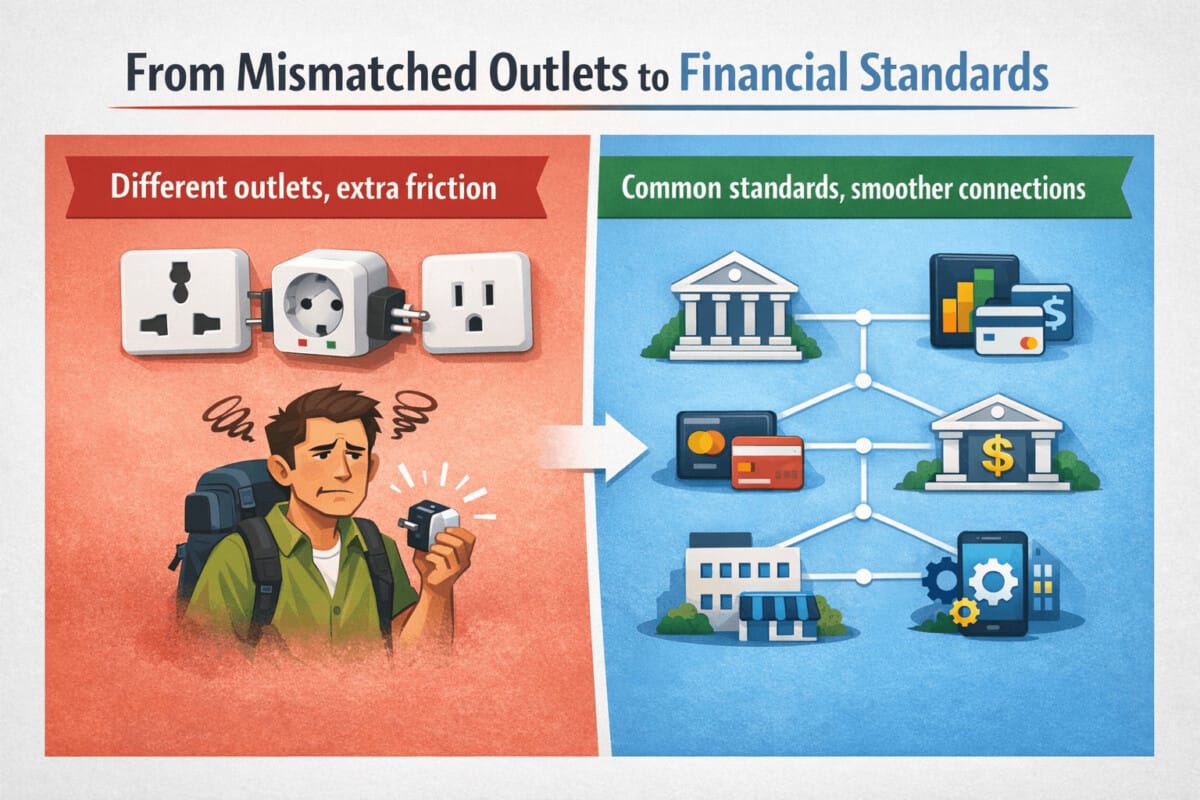

You only need to travel abroad once to understand why standards matter.

You packed the charger. Your phone is almost dead. The hotel room has power. But the outlet shape is different, so nothing connects. Suddenly, a tiny design difference turns into friction, delay, extra cost, and mild annoyance.

That is exactly how many people think about standards: annoying rules that make everything look the same.

But in reality, the opposite is often true.

Without standards, systems become harder to connect, more expensive to operate, and more likely to fail.

That is true for power outlets. It is also true for finance.

Standards do not remove freedom. They reduce friction.

At first glance, standardization can feel restrictive. Why should everyone follow the same format, the same code, or the same protocol?

Because when every system uses its own rules, the burden shifts to everyone else.

If power outlets are all different:

- travelers need adapters

- manufacturers build more variations

- mistakes become more common

- costs rise for everyone

Finance works the same way.

Banks, payment companies, card networks, securities firms, central banks, and regulators all exchange data. If each institution uses a different language, format, identifier, or messaging structure, the system still works — but only after adding layers of translation, reconciliation, exception handling, and manual repair.

That is why financial standards matter.

They are not there to make finance look tidy. They are there to make finance connectable.

Why standards matter in finance

Finance is a network business. Money moves because systems agree on what a message means, who a party is, which currency is involved, and how a transaction should be recorded.

That is why standards in finance matter for at least three practical reasons.

1. They create interoperability

A payment message is only useful if the receiving institution understands it the same way the sending institution intended it.

That is the basic promise of interoperability.

In finance, interoperability means:

- one institution can read another institution’s message correctly

- systems can connect without custom translation every time

- cross-border transactions become easier to process

- automation becomes much more realistic

A good example is ISO 20022, the global messaging standard used across many payment and financial market infrastructures. If you want to reference it in the article, this is a good place to add the link:

When people talk about modern payment infrastructure, they are often really talking about better standardization.

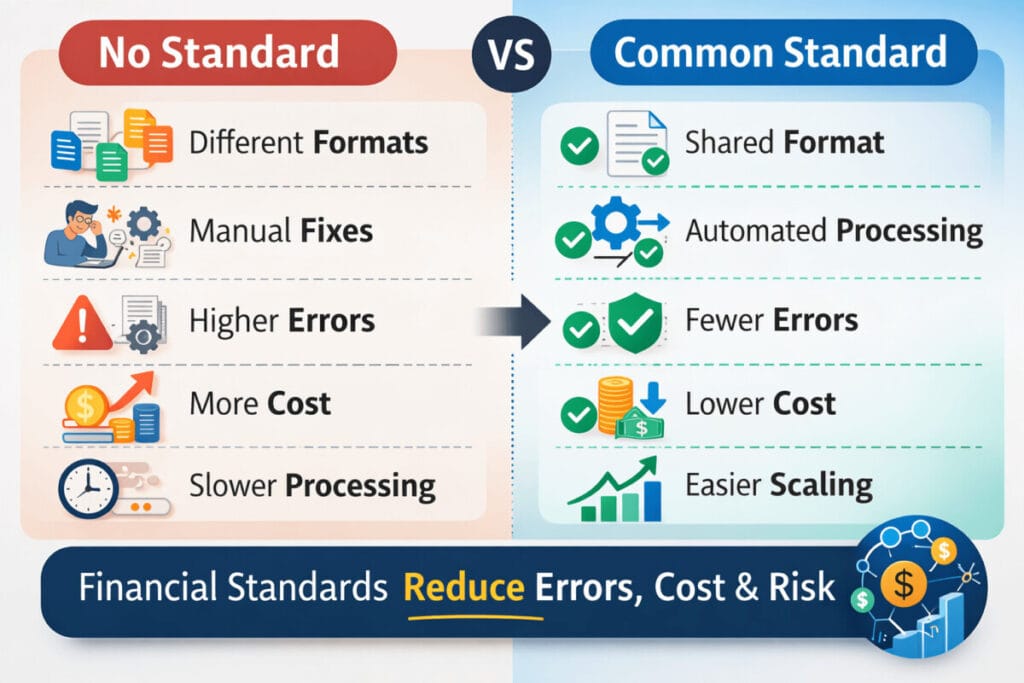

2. They reduce errors and operating costs

When data is inconsistent, operations become expensive.

Someone has to map fields. Someone has to fix exceptions. Someone has to investigate why one system read a payment instruction differently from another.

That is not innovation. That is friction.

Financial standards reduce that friction by making data more structured, more predictable, and easier to automate.

In other words, standards lower the cost of trust.

That is one of the most overlooked reasons why standards matter in finance: not because they are elegant, but because they reduce rework.

3. They make scale possible

A market cannot scale well if every new participant needs a custom integration with every existing participant.

That is true in software. It is true in telecom. And it is very true in finance.

A common standard lowers onboarding costs. It allows new banks, fintech firms, payment providers, and market infrastructures to plug into a larger network without reinventing every connection from scratch.

So while standards may look boring, they often make competition and innovation easier, not harder.

Financial standards are already part of daily life

Most people do not notice standards when they work.

They only notice them when they fail.

That is why power outlets are such a useful analogy. You do not think about outlet standards until your plug does not fit.

Finance is full of the same invisible infrastructure.

Think about how much depends on shared standards:

- currencies being represented consistently, such as USD, EUR, and KRW

- institutions being identified correctly

- companies being identified across markets and regulators

- card payment messages being interpreted the same way

- payment instructions flowing across domestic and international systems

Those are all examples of financial standards doing quiet but essential work in the background.

Who creates international financial standards?

This is where the topic becomes more interesting.

A lot of people assume standards appear naturally. In reality, they are usually built through long technical coordination.

In the financial sector, one important body is ISO TC68, the International Organization for Standardization’s technical committee for financial services.

A useful link to place here is:

https://www.iso.org/committee/49650.html

ISO TC68 is one of the key international forums where financial standards are developed across areas such as:

- payments

- securities

- financial identifiers

- data exchange

- information security

That matters because finance does not just need one standard. It needs a whole ecosystem of standards.

A few real examples of financial standards

To make this less abstract, here is a short table you can keep in the article.

| Standard | What it does | Why it matters |

|---|---|---|

| ISO 20022 | Standardizes financial messaging | Helps payment and financial systems exchange richer, structured data |

| ISO 4217 | Standardizes currency codes | Makes USD, EUR, JPY, KRW universally recognizable |

| ISO 9362 | Defines BIC codes | Helps identify financial institutions in messaging and routing |

| ISO 17442 | Defines the LEI framework | Helps identify legal entities consistently across markets |

| ISO 8583 | Standardizes card transaction messaging | Supports card authorization and payment processing |

| ISO 18245 | Defines merchant category codes | Helps classify merchants in card payments |

This is the key point: these standards are not about making everything identical for the sake of uniformity.

They are about making systems legible, compatible, and scalable.

Recent standards work shows where finance is heading

Another reason this topic matters: financial standardization is not old news.

It is still evolving.

Recent work around ISO TC68 shows that standards are not limited to traditional banking forms and payment files. The conversation now reaches into newer areas such as:

- richer payment data

- entity and transaction identifiers

- card and merchant data classification

- digital finance

- AI

- DeFi

- security for distributed systems

That tells us something important.

Standards are not the opposite of innovation. They are usually what allows innovation to spread safely.

If you want to include a supporting source for TC68 developments, a useful place to point readers is the TC68 materials page or committee page above.

The real lesson from power outlets

The power outlet example works because it feels trivial.

But it captures a serious truth.

When standards differ too much, users do not gain meaningful freedom. They inherit the burden of incompatibility.

In finance, that burden is much larger.

If systems cannot interpret one another cleanly, the result is not just inconvenience. It can mean:

- slower payments

- higher processing costs

- more operational risk

- weaker reporting

- more friction in cross-border finance

That is why standards in finance matter so much.

They are not glamorous. They rarely become headlines. But they make the system more understandable, more reliable, and more scalable.

Or put more simply:

Standards do not make finance boring. They make finance work.

Final thought

We usually think of standards as something imposed from above.

A better way to see them is this:

A standard is a shared agreement that reduces friction for everyone who comes later.

That is why the mismatch between power plugs feels so annoying.

And that is why financial standards matter so much.

Because in the end, every complex network faces the same question:

Will we spend our time building useful things, or wasting time trying to connect things that should have matched in the first place?

Suggested external links to place in the article

- ISO 20022 overview

https://www.iso20022.org/iso-20022 - ISO TC68 committee page

https://www.iso.org/committee/49650.html - Bank of England on ISO 20022

https://www.bankofengland.co.uk/payment-and-settlement/rtgs-renewal-programme/iso-20022 - SWIFT on ISO 20022

https://www.swift.com/standards/iso-20022/iso-20022-financial-institutions-focus-payments-instructions

Suggested meta description

Why do standards matter in finance? Using the simple example of mismatched power outlets, this article explains interoperability, ISO 20022, ISO TC68, and why financial standards reduce friction, cost, and risk.