A Simple Guide to How Stablecoin Payments Fit Into Real-World Finance

When people first hear about stablecoin payments, they often imagine a future where banks, card networks, and traditional payment systems disappear. The idea sounds simple: money moves on blockchain networks, so existing payment rails must become unnecessary.

That is not how things usually work in practice.

In the real world, stablecoin payments work with existing payment rails far more often than they replace them. In many cases, stablecoin payments are added to the current financial system as a new way to move value, especially in settlement, payouts, and cross-border transfers. The rest of the payment process often still depends on banks, card networks, payment processors, compliance systems, and merchant operations.

To understand how stablecoin payments work with existing payment rails, it helps to begin with one basic question: what is a stablecoin?

What Is a Stablecoin?

A stablecoin is a digital asset designed to keep its value relatively stable. Unlike highly volatile crypto assets, stablecoins are usually built to stay close to the value of a traditional currency such as the U.S. dollar.

Some of the best-known examples are USDT, USDC, and PYUSD. These are often described as dollar-based stablecoins because they are designed to stay close to 1 coin = about 1 U.S. dollar.

The easiest way to think about a stablecoin is this:

A stablecoin is a digital form of value that moves on blockchain networks but is designed to stay close in value to traditional money.

That relative stability is what makes stablecoins easier to use in payments. If a merchant sells a product for $20, they do not want to receive something worth $20 today and $14 tomorrow. Payment systems need predictability, and stablecoins are designed to provide more of that than highly volatile crypto assets.

Why Are Stablecoins Considered Stable?

Stablecoins are called “stable” because they are structured to stay near a reference value, usually the U.S. dollar.

A simple example makes this easier to understand.

Imagine a company issues a digital token and says that each token should always be worth about one dollar. People are more likely to trust that token if they believe there is a real system behind it that supports the value. In many cases, this includes reserves, redemption mechanisms, and a clear promise that the token can be exchanged back into fiat value.

A useful comparison is a gift card. A gift card has value not because the card itself is valuable, but because people believe it can be redeemed for something real. A stablecoin works in a similar way. Its value comes from the structure behind it, not from the digital token alone.

This is why stablecoin payments are discussed so often in commerce. Their relative price stability makes them much more suitable for payments than assets whose value changes sharply from day to day.

Why Do Stablecoin Payments Matter for Payments at All?

Stablecoin payments matter because businesses care about usable money, predictable value, and efficient transfer.

That does not mean stablecoins replace everything. It means they can improve certain parts of the payment process.

This is the key idea:

Stablecoin payments usually work with existing payment rails, not instead of them.

That is the real answer to the topic.

Where do stablecoins actually fit into normal payment systems that already use cards, banks, merchant accounts, and payout networks?

The answer is that stablecoins usually connect to the parts of the system where money is settled, moved, or paid out.

Payments Are Not One Single Action

Most people think a payment is one simple step. You click “pay,” and the transaction is done.

But actual payment systems have multiple layers.

For example, in a typical online purchase:

- the customer chooses a payment method

- the payment is authorized

- the merchant sees confirmation

- funds are later settled

- the merchant finally receives usable money

So the customer-facing payment experience and the actual movement of funds are not exactly the same thing.

This is important because stablecoins often connect to the back-end layers of payments more than the front-end layers.

That is why stablecoin payments work with existing payment rails so naturally. They do not always change what the customer sees. Instead, they often change how value moves after the transaction starts.

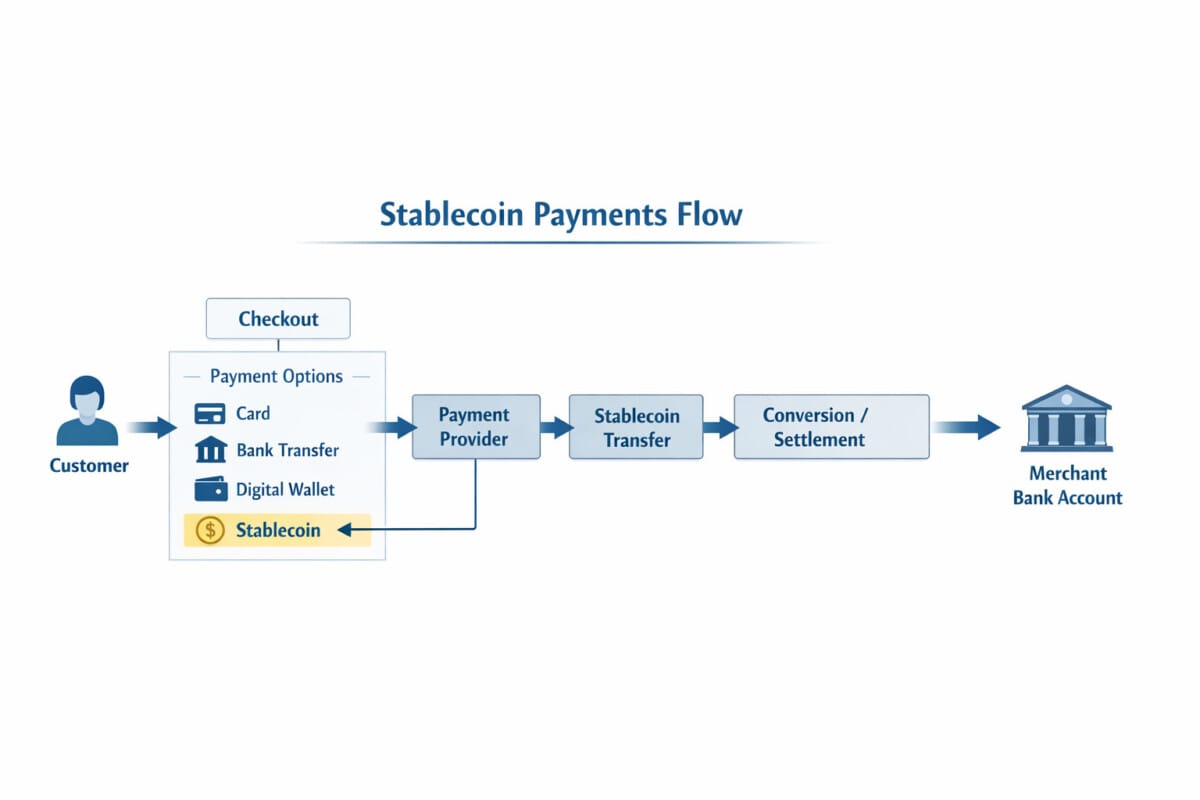

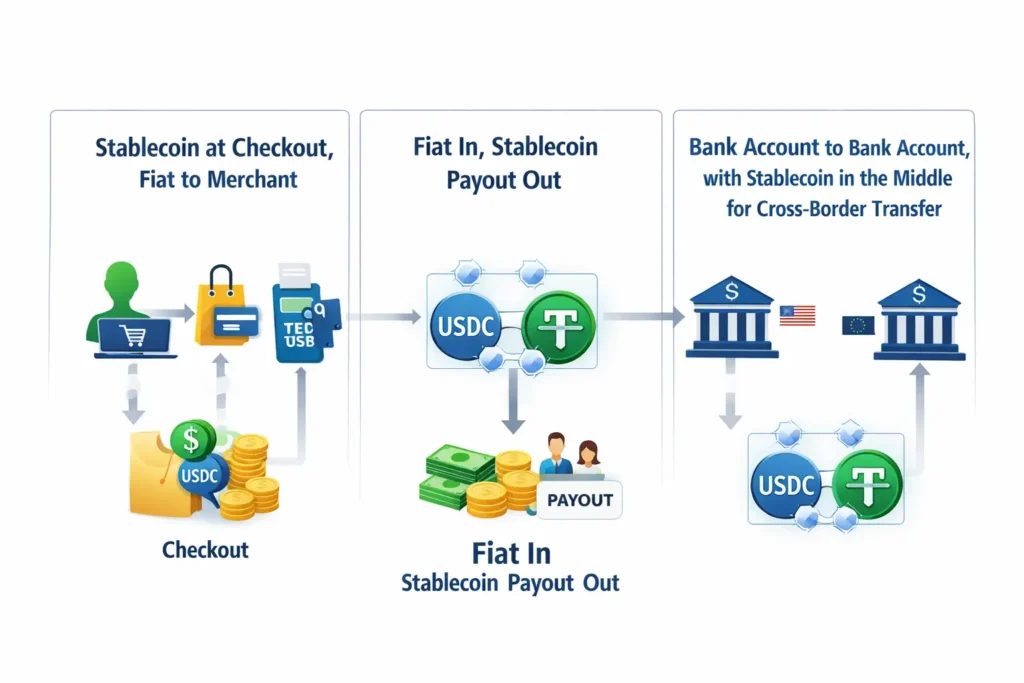

Example 1: The Customer Pays With a Stablecoin, but the Merchant Receives Fiat

This is one of the clearest examples of how stablecoin payments work with existing payment rails.

Imagine an online store that allows customers to pay with USDC or USDT.

From the customer’s point of view, the store accepts stablecoin payments.

But the merchant may not want to hold stablecoins directly. Instead, a payment provider can accept the stablecoin payment, process it, and then settle the merchant in dollars or another fiat balance.

So the flow looks like this:

- the customer pays with a stablecoin

- an intermediary processes the transaction

- the merchant receives fiat-denominated settlement

This is a very practical model because it lets the customer use stablecoin payments while the merchant continues operating inside existing financial systems.

In other words, the stablecoin is introduced at the payment input stage, but the merchant side still runs on familiar rails such as fiat accounts, standard settlement systems, and existing business operations.

That is one of the most common ways stablecoin payments work with existing payment rails.

Example 2: A Business Receives Money Normally but Uses Stablecoins for Payouts

This example is even more relevant for many platforms and global businesses.

Imagine a company that receives customer payments through cards, bank transfers, or standard payment processors. The incoming side of the business still uses traditional payment rails.

Later, the company needs to send money to freelancers, creators, sellers, suppliers, or overseas partners.

That is where payouts become difficult. Cross-border payouts can be slow, expensive, and complicated. So instead of changing the whole customer payment experience, the company only changes the outgoing payment layer.

For example:

- customers pay through normal card or bank-based methods

- the company records revenue in fiat

- payouts to global users are made in USDC

This means stablecoins are being used not to replace the full payment system, but to improve one part of it: the payout layer.

This is another good example of how stablecoin payments work with existing payment rails. Existing rails continue to handle customer acquisition, payment acceptance, and accounting, while stablecoins improve how funds are sent out.

Example 3: Stablecoins as a Bridge in Cross-Border Payments

Cross-border transfers are another area where stablecoin payments often make sense.

But again, the important point is not total replacement. It is integration.

Imagine a transfer from one country to another.

A possible flow could look like this:

- the transfer begins from a normal bank account

- the value moves across borders using USDC

- the funds are converted back into local currency

- the recipient receives money in a normal bank account or local payout channel

So the beginning and the end of the transfer still rely on traditional rails. The stablecoin is mainly used in the middle, where moving value can otherwise be slow, expensive, or operationally difficult.

A simple travel analogy makes this easy to understand.

- you take a taxi from home to the airport

- you fly between countries

- you take a bus from the airport to the hotel

The plane does not replace the whole journey. It improves the longest and most difficult part.

Stablecoins often play the same role in cross-border payments. They do not necessarily replace the full payment route. They improve the middle section.

This is one more example of how stablecoin payments work with existing payment rails in a practical setting.

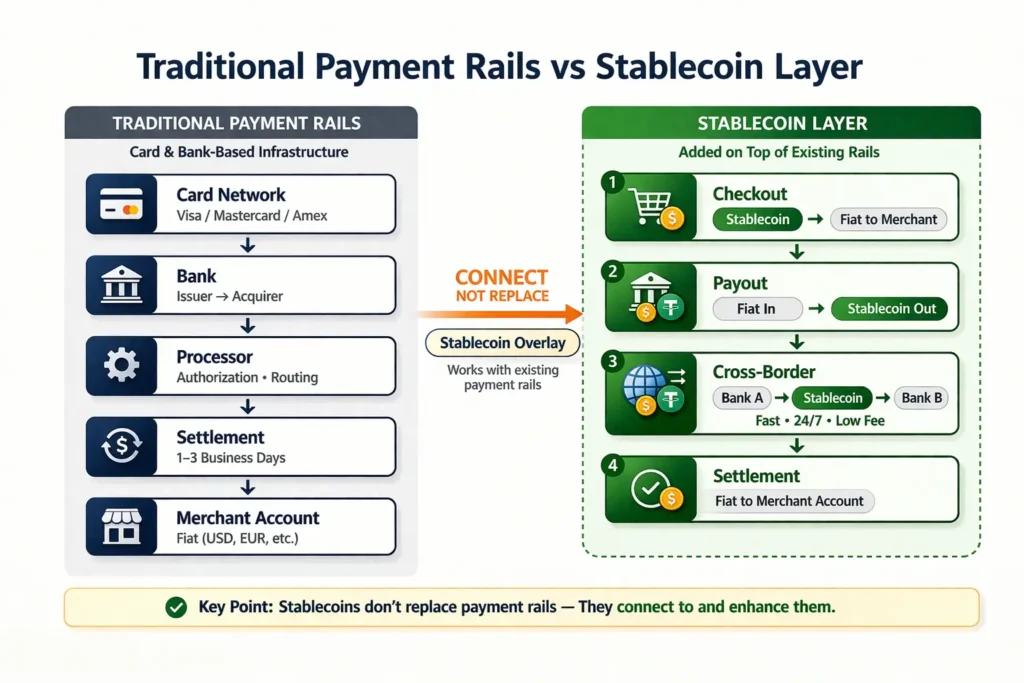

The Main Ways Stablecoin Payments Connect to Existing Payment Rails

At a practical level, there are three common ways stablecoin payments fit into the current system.

1. Stablecoins as a payment method

Customers may be allowed to pay with USDT, USDC, or PYUSD at checkout.

But the merchant may still receive fiat settlement.

2. Stablecoins as a payout method

A business may continue using traditional payment rails for incoming revenue while using stablecoins to pay contractors, sellers, or users.

3. Stablecoins as a settlement or transfer bridge

A transfer may start in fiat, move through a stablecoin network, and end in fiat again.

These patterns explain how stablecoin payments work with existing payment rails better than the idea of total disruption. Stablecoins are often inserted into specific parts of the payment stack where they solve a clear operational problem.

A Simple Table Makes It Easier to See

| Situation | What the customer or business sees | What may actually happen in the background |

|---|---|---|

| Online store accepts stablecoins | Customer pays with USDC or USDT | Merchant may still receive fiat settlement |

| Platform pays global users | Customers pay through cards or bank transfer | Business may use stablecoins only for outgoing payouts |

| Cross-border transfer | Looks like a normal international transfer | Stablecoins may handle only the middle movement of value |

| Business treasury movement | Company still manages accounts in fiat | Stablecoins may be used only for selected transfer layers |

The pattern is simple:

Stablecoin payments work with existing payment rails by improving selected layers, not by rebuilding the whole payment system from zero.

Why Existing Payment Rails Still Matter

Even if stablecoin payments become more common, traditional payment rails still matter because payments are about much more than value transfer.

Real-world payment systems also need:

- customer verification

- fraud controls

- refunds

- dispute handling

- tax reporting

- accounting

- compliance

- merchant settlement

- local bank connectivity

A blockchain-based asset transfer alone does not automatically solve all of those things.

That is why stablecoins usually operate alongside the current payment system rather than replacing it entirely.

A simple way to understand it is this:

Traditional payment rails are still the structure of the building.

Stablecoins are more like a faster new system added inside the building to improve how part of it works.

You do not need to tear down the entire structure to make one important part more efficient.

The Simplest Summary

Stablecoin payments work with existing payment rails by plugging into specific layers such as checkout, settlement, payouts, and cross-border transfers, while the rest of the payment system often continues to rely on banks, card networks, and traditional financial infrastructure.

Conclusion

The biggest mistake people make is assuming stablecoins must either replace traditional payment systems completely or fail to matter at all.

The reality is much more practical.

A customer can pay with USDC, while the merchant still receives fiat.

A platform can collect money through cards but use stablecoins for global payouts.

An international transfer can begin in a bank account, move through a stablecoin network, and end in another traditional account.

That is the clearest way to understand how stablecoin payments work with existing payment rails.

They usually do not erase the current payment system overnight.

They connect to it.

And they matter precisely because they can improve the parts of the system that are slow, costly, or difficult to operate across borders.

References

Finteconomix – Stablecoin payments for freelancers

https://finteconomix.com/stablecoin-payments-for-freelancers/

Stripe Docs – Stablecoin payouts for Connect

https://docs.stripe.com/connect/stablecoin-payouts

Circle – USDC

https://www.circle.com/usdc

PayPal – PYUSD

https://www.paypal.com/pyusd

Tether – USDT

https://tether.to/en/