From cards and bank transfers to mobile wallets and online checkout

When people search for what is electronic payment system, they are usually not looking for a narrow dictionary definition. They want to understand how modern payments actually work. They want to know why businesses can accept money online, why a phone can replace a wallet, and what really happens after a customer taps a card or clicks Pay Now.

An electronic payment system is the structure that makes all of that possible. It allows money to move digitally between consumers, businesses, banks, and payment providers without the physical exchange of cash. That simple idea powers a huge part of modern commerce, from e-commerce and subscription billing to ride-hailing apps and international marketplaces.

This is why the topic matters. An electronic payment system is not just a fintech buzzword. It is part of the infrastructure behind the digital economy.

What is an electronic payment system?

An electronic payment system is a digital system that enables the transfer of money between parties through electronic networks rather than through physical cash. Instead of handing over notes and coins, the payment is initiated and processed through connected financial institutions, payment processors, gateways, card networks, and settlement systems.

In practical terms, an electronic payment system includes the technologies and institutions that make digital transactions possible. It covers the moment a customer pays, the approval of that payment, the processing of the transaction, and the final transfer of funds between institutions.

That is why a card swipe, an online checkout page, a QR payment, and a mobile wallet payment all belong to the same broader world of electronic payment systems. The user experience may look different, but the core idea is the same: value moves electronically.

Why electronic payment systems became so important

Cash still matters, but modern commerce increasingly depends on digital speed, remote access, and seamless user experience. A customer buying a coffee in person can use cash. But a customer paying for cloud software, an online course, a streaming subscription, or an international delivery service cannot rely on physical currency in the same way.

Electronic payment systems solve that problem. They allow transactions to happen across distance, across platforms, and often across borders. They also make it possible for businesses to automate recurring payments, reduce checkout friction, expand into new markets, and serve customers through websites and apps.

This is one reason digital payments have become more than a convenience feature. They are now central to how modern business works.

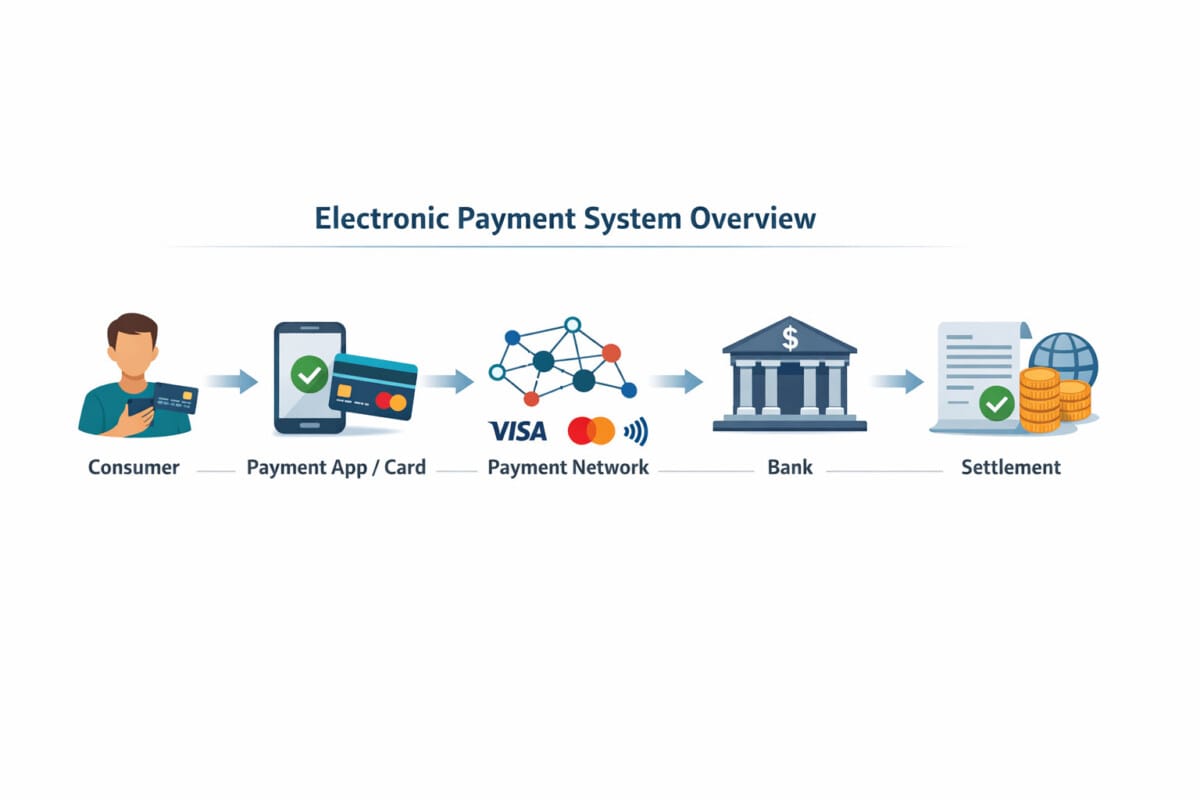

How an electronic payment system works

Most digital payments feel simple on the surface. A customer taps a card, confirms a wallet payment, or enters card details at checkout. But behind that smooth experience is a layered process.

Payment starts with the user

Every transaction begins with a payment instruction. The customer chooses how to pay, whether through a credit card, debit card, bank transfer, mobile wallet, QR code app, or another digital method.

The payment request moves through a network

Once the payment is initiated, the request is sent through a payment gateway or processor. These intermediaries help route the transaction data securely through the correct systems. In card payments, the transaction may pass through a card network such as Visa or Mastercard. In bank-based payments, it may move through domestic transfer rails or instant payment infrastructure.

The payment is authorized

The customer’s bank or card issuer checks whether the account is valid, whether funds or credit are available, and whether the transaction should be approved. Fraud checks may also happen at this stage.

The payment is processed, cleared, and settled

Authorization is not always the same as final movement of funds. After approval, payment instructions still need to be processed between institutions. In the background, the transaction goes through clearing and settlement steps so the merchant’s side eventually receives the funds.

For users, this often feels instant. For the system, it is a coordinated process involving multiple parties.

The main parts of an electronic payment system

A better blog post does more than define the term. It explains the structure. An electronic payment system usually includes several connected elements.

The payer

This is the person or business making the payment.

The payee or merchant

This is the person or business receiving the payment.

The payment method

This includes the instrument the customer uses, such as a credit card, debit card, bank account, wallet balance, QR code app, or payment-linked mobile device.

The payment gateway

In online payments, the gateway securely transmits transaction information from the merchant to the payment processor or relevant network.

The payment processor

The processor handles the technical side of moving transaction data and helps route the payment through the necessary infrastructure.

The issuing bank

This is the bank or institution that provides the customer’s card or account.

The acquiring bank

This is the bank or institution that supports the merchant in accepting payments.

The network layer

Depending on the payment type, this can include card networks, bank transfer systems, instant payment rails, or alternative payment infrastructure.

The clearing and settlement layer

This is where the financial positions between institutions are matched and the actual transfer of funds is completed.

This broader structure is why the phrase electronic payment system means much more than one app or one card brand. It refers to the whole system that makes digital payments work.

Types of electronic payment systems

There is no single kind of electronic payment system. The payment ecosystem includes several major categories, each serving a different use case.

Card payment systems

Card payments remain one of the most familiar forms of electronic payment. Credit cards allow users to pay through borrowed credit and settle later. Debit cards draw directly from deposit balances. These systems are deeply embedded in online shopping, retail payments, travel, hospitality, and subscription commerce.

Because of their global acceptance and familiar user experience, card-based systems continue to play a major role in electronic payments.

Bank transfer systems

Bank transfers are another core category. These systems move money directly from one bank account to another. They include traditional account transfers, wire payments, ACH-style transfers, and fast or instant payment systems.

For businesses, bank-based payment systems are especially important in payroll, supplier payments, B2B settlement, and larger-value transactions.

Digital wallet systems

A digital wallet stores payment credentials electronically and makes checkout faster by reducing the need to manually enter payment information every time. Wallets can sit on top of card networks, bank accounts, or stored-value balances.

They are especially important in mobile commerce, where every extra checkout step can reduce conversion.

Mobile payment systems

Mobile payments refer to transactions completed through a smartphone or connected device. They may rely on contactless NFC, wallet apps, stored payment credentials, or in-app payment flows. In many markets, the phone has become the new payment interface.

QR code payment systems

QR payments are widely used in many Asian and emerging-market ecosystems. They often allow consumers to scan a merchant code and pay directly through an app, a wallet, or a linked bank account. This model has become especially attractive where smartphones are widespread and card acceptance infrastructure is less dominant.

Online payment platforms

These platforms help businesses accept and manage payments online. They may combine gateway functions, merchant tools, fraud management, payout tools, and integration layers for digital commerce.

This category has become increasingly important as online business models have grown.

Popular examples of electronic payment systems

A blog post targeting electronic payment system searches should include recognizable examples. Readers often search the phrase because they want to connect the concept to services they already know.

PayPal

PayPal is one of the most recognized online payment platforms in the world. It became a major early player in digital commerce by making online payments easier for both buyers and merchants.

Apple Pay

Apple Pay helped make digital wallets mainstream by allowing users to store payment cards on Apple devices and pay in stores, apps, and online.

Google Pay

Google Pay extends the digital wallet model across Android and web-based commerce, helping simplify payment across devices and merchant environments.

Visa

Visa is one of the most important global payment networks. It does not issue cards directly as a bank would, but it provides the network layer that helps electronic card payments move between issuers, acquirers, processors, and merchants.

Mastercard

Mastercard plays a similar role, powering a large share of global digital card payments across industries and geographies.

Alipay

Alipay is one of the biggest digital payment platforms in the world and a major example of how electronic payment systems can evolve into broader commerce ecosystems.

WeChat Pay

WeChat Pay shows how payments can become deeply integrated into daily digital life, linking messaging, commerce, and financial activity in one environment.

These examples matter because they show that an electronic payment system can be a network, a wallet, a platform, or an integrated payment ecosystem.

Electronic payment system vs cash payment

One of the most useful ways to deepen the article is to compare electronic payment systems with physical cash.

Cash is a direct, electronic payment is infrastructure-based

Cash works through direct physical transfer. One person hands value to another, and the transaction is complete. An electronic payment system depends on institutions, technology, and network connectivity.

Cash is physical, and electronic payment is digital

Cash exists as notes and coins. Electronic payments exist as digital balances, account entries, and payment messages moving across networks.

Cash works offline, digital payments often need systems to function

A cash transaction can happen without a terminal, network, or internet connection. Many electronic payment systems rely on devices, software, and financial networks.

Cash offers limited data, electronic payments generate records

Cash is often associated with immediacy and a degree of anonymity. Electronic payments create transaction histories that can support receipts, accounting, fraud analysis, budgeting, and business intelligence.

Cash settles instantly between people, digital payments settle through institutions

When cash changes hands, settlement is direct. With electronic payments, customer confirmation can happen immediately, but institution-to-institution settlement may happen later.

This comparison adds depth because it shows that electronic payment systems are not simply digital versions of cash. They are a different model of moving value.

Why businesses care so much about electronic payment systems

For businesses, an electronic payment system is not just a utility. It can directly affect conversion, customer experience, geographic reach, and operational efficiency.

A merchant that supports more payment methods often reduces checkout abandonment. A SaaS company needs recurring billing. A marketplace needs split payouts and onboarding. A global seller may need local payment methods, multicurrency support, and cross-border acceptance. A subscription business needs retries, renewals, and payment visibility.

In other words, payments shape revenue. That is why businesses do not think about electronic payment systems only as back-office plumbing. They think about them as part of growth strategy.

Why this topic matters in fintech

The fintech sector has spent years trying to improve friction points in traditional payments. Better user interfaces, faster onboarding, embedded payments, real-time transfers, mobile-first experiences, and API-based integrations all sit on top of the same underlying problem: how to move money more efficiently.

That is why electronic payment systems are one of the most useful foundational topics in fintech content. They connect consumer behavior, platform economics, payment infrastructure, and financial innovation in one keyword area.

A beginner may search the topic to understand digital payments. A founder may search it to understand checkout infrastructure. A policy reader may search it to understand how payment systems shape the economy. That range gives the topic strong evergreen value.

The future of electronic payment systems

Electronic payment systems are still changing, and the next stage of payment development is likely to be shaped by several clear trends.

Real-time payment infrastructure

More countries are building instant account-to-account payment rails that allow money to move within seconds rather than in batch-based cycles.

Embedded payment experiences

Payments are increasingly disappearing into the user experience. People do not always think about “making a payment” as a separate step anymore. The payment is built into the platform flow.

More direct account-based models

In some markets, there is growing interest in reducing dependence on card rails and expanding direct bank-based payment options.

Stronger security and identity layers

As digital payments scale, fraud prevention, tokenization, authentication, and trust frameworks become even more important.

Cross-border modernization

Global business continues to push for payment systems that are faster, cheaper, and more interoperable across countries and currencies.

These trends suggest that electronic payment systems will become even more important, not less.

Final thoughts

So what is an electronic payment system?

It is the digital structure that allows money to move without physical cash by connecting users, merchants, banks, payment providers, and networks. It supports card transactions, bank transfers, digital wallets, mobile payments, QR code payments, and online checkout experiences.

But the more important point is this: an electronic payment system is not just a payment method. It is part of the infrastructure of modern commerce. It helps power e-commerce, recurring subscriptions, digital services, cross-border trade, and platform-based business models.

That is why the topic deserves more than a short definition. To understand the digital economy, you have to understand how digital payments work. And to understand digital payments, you need to understand the electronic payment system behind them.

References

World Bank – Payment Systems and Financial Market Infrastructure

https://www.worldbank.org/en/topic/paymentsystemsremittances

Federal Reserve – Payment Systems

https://www.federalreserve.gov/paymentsystems.htm

McKinsey – Global Payments Report

https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-report