Why cross-border payments are suddenly everywhere again

If you have been seeing more cross-border payments news lately, that is not a coincidence. In 2026, international payments are back at the center of the financial conversation because the old problems have not gone away, and the pressure to fix them is rising again.

Cross-border payments still tend to be slower, more expensive, and less transparent than domestic payments. That gap matters more now because digital commerce is global, travel is more digital, and both consumers and businesses expect money to move with the same clarity they get from local instant payment systems. The Financial Stability Board has warned that progress under the G20 roadmap remains uneven and that some of the headline targets for retail cross-border payments are at risk of being missed.

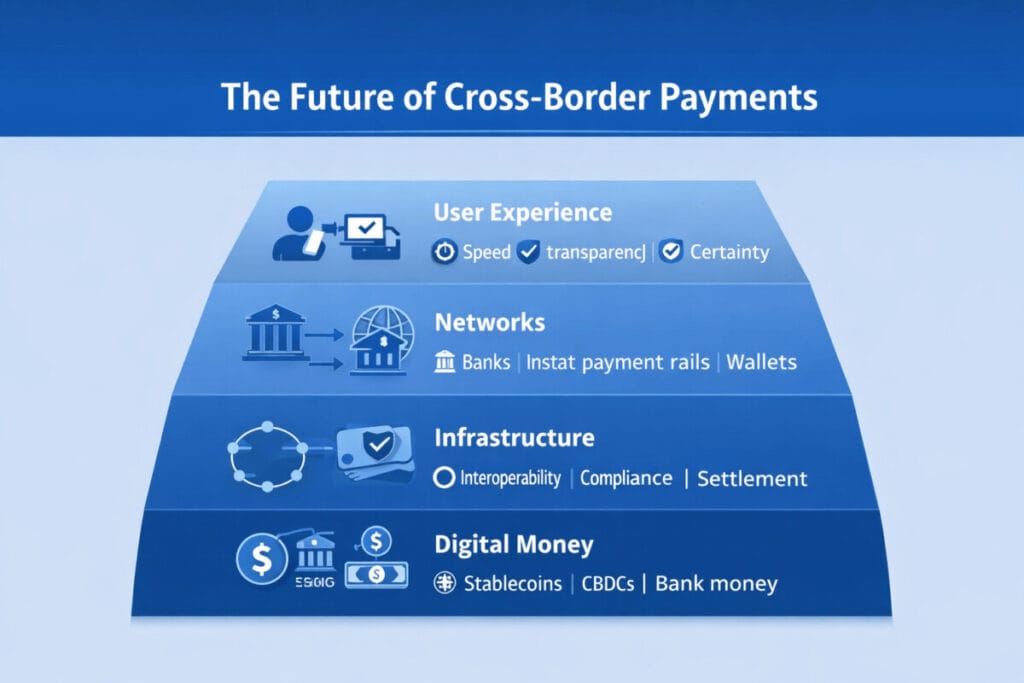

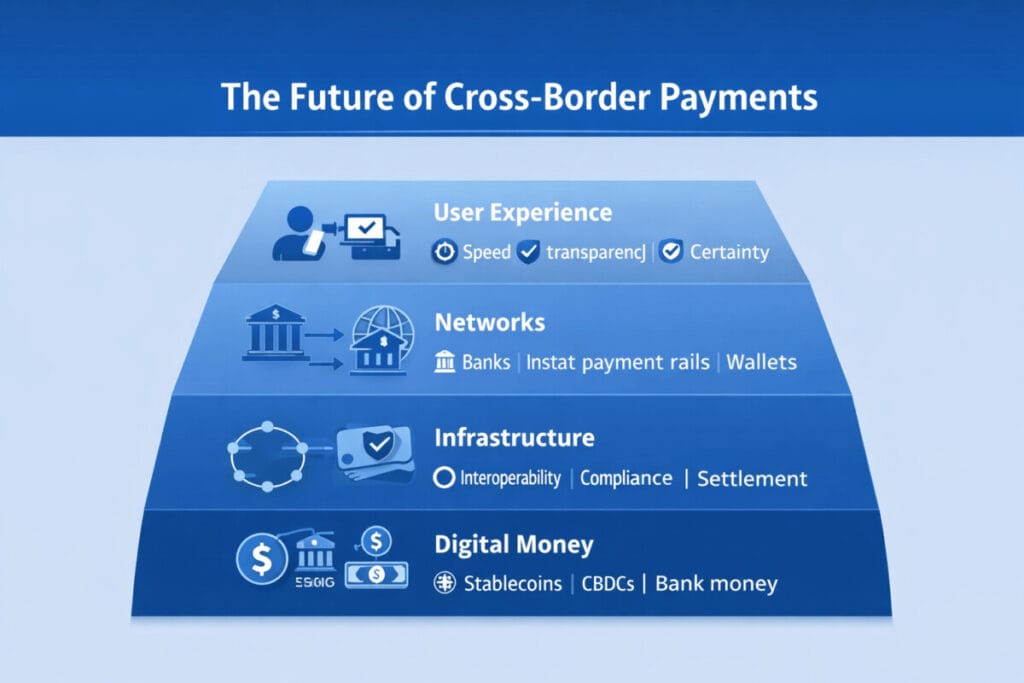

That is why the 2026 conversation is not just about “faster transfers.” It is about something bigger: how to make global payments feel more like domestic payments. The most important changes this year are happening around predictability, interoperability, payment network rules, and the growing role of digital-money alternatives such as stablecoins and CBDCs. (Reuters)

The old cross-border payment model is under pressure

For years, cross-border payments have relied heavily on layered correspondent banking relationships, fragmented compliance checks, and multiple intermediaries. That structure has not disappeared, but the market is under pressure from every direction.

Consumers want to know when money will arrive. Small businesses want fewer surprises in fees. Platforms want simpler checkout and payout experiences. Regulators want better transparency and stronger control. Fintechs want more direct access to local rails. All of these pressures point to the same conclusion: the existing model is no longer good enough as the default experience.

The most revealing part of recent policy and industry discussion is that the goal is no longer only to move money across borders. The new goal is to make that movement predictable, visible, and easier to integrate into digital experiences. Swift’s recent retail payments framework makes that especially clear. Swift says many payments on its network already reach destination banks quickly, but the real friction often sits in the front end and in the final domestic leg. That means speed inside the network is not the whole story; the end-to-end user experience is now the real battleground.

The biggest changes in cross-border payments in 2026

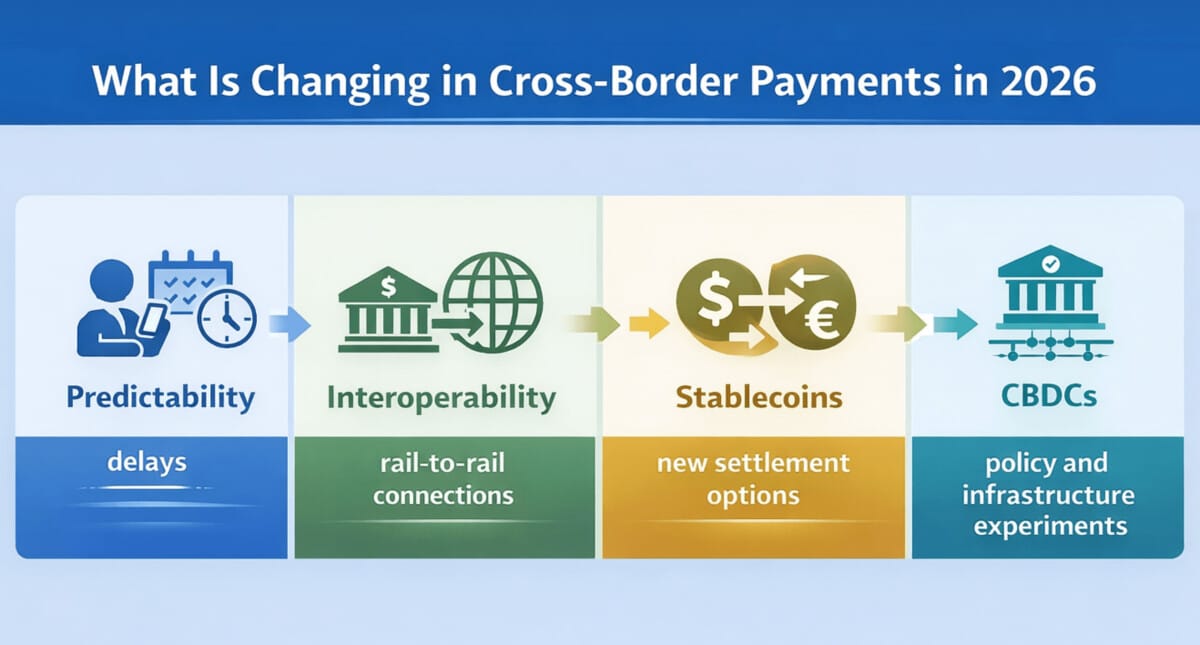

1. Predictability is becoming as important as speed

One of the clearest 2026 shifts is that predictability now matters almost as much as raw speed.

In the past, a provider could market a payment as “fast” even if the final amount received was uncertain or the timing varied from corridor to corridor. That is becoming much harder to justify. Swift’s new retail cross-border framework explicitly emphasizes full predictability on price and speed, no hidden fees, and full-value transfers where possible.

This is a major change in how the industry frames quality. Users do not experience a payment as successful merely because a message was transmitted efficiently. They experience success when they know:

- how much will arrive,

- when it will arrive,

- what fee will be charged,

- and whether anything could delay it.

That sounds simple, but in cross-border payments it is a structural shift.

2. Interoperability is becoming the real growth story

Another major 2026 theme is interoperability. Many countries now have powerful domestic instant payment systems, but those systems were not built at the same time, with the same architecture, or for the same legal environments. The result is that money can move elegantly inside national borders and still become clumsy the moment it crosses them.

That is why recent developments around payment network linkages matter so much. Reuters reported that India has been in discussions about allowing Alipay+ to connect with UPI for cross-border digital payments. Even beyond the specific geopolitical complexities of that case, the broader point is clear: the future of cross-border payments may depend less on inventing entirely new rails and more on connecting major domestic and regional rails more intelligently.

This is also why the market keeps paying attention to projects involving UPI, wallet networks, regional payment linkages, and other real-time retail infrastructures. The key question is no longer just, “Who owns the network?” It is increasingly, “Which networks can connect without creating new friction?”

3. Stablecoins are moving from crypto talking point to payment infrastructure debate

Stablecoins continue to appear in cross-border payments news because they promise something the traditional system often struggles to provide: continuous availability, fewer intermediaries, and potentially cheaper settlement for some use cases. Reuters noted that pressure is growing from the crypto sector to ease regulation around stablecoins, while regulators continue to warn about financial stability and monetary sovereignty risks.

This is where 2026 becomes especially interesting. Stablecoins are no longer discussed only as speculative digital assets. They are increasingly being discussed as part of the payment stack, especially for international transactions and certain emerging-market use cases. At the same time, central banks and regulators are clearly not treating this as a simple technology story. The debate is now about who can issue trusted digital money, under what rules, and with what safeguards.

That does not mean stablecoins will replace bank-based cross-border payments in the near term. It does mean they are now part of the competitive and regulatory landscape in a more serious way than before.

4. CBDC conversations are becoming more cross-border

Retail CBDCs often dominate public attention, but in 2026 another important theme is cross-border linkage. Reuters reported that India’s central bank proposed linkages between BRICS digital currencies for trade and tourism payments, following broader discussions on payment system interoperability.

This matters because it shows that CBDC discussions are no longer just about domestic digitization. They are also about international settlement design, regional influence, and payment sovereignty. Whether these initiatives succeed or not, they reveal a growing truth: digital currency strategy and cross-border payment strategy are becoming harder to separate.

A simple table: what is actually changing in 2026?

| Theme | What is changing | Why it matters |

|---|---|---|

| Predictability | Networks are focusing more on transparent fees, timing, and full-value delivery | Users want certainty, not just speed |

| Interoperability | More attention is shifting to linking domestic real-time payment systems and wallet networks | Growth depends on connection, not only on new rails |

| Stablecoins | Stablecoins are being discussed more seriously as payment tools in some cross-border use cases | They challenge legacy payment models and regulatory frameworks |

| CBDCs | Cross-border linkage and interoperability are gaining more attention | Digital currency policy is becoming part of payment infrastructure strategy |

| Regulatory pressure | Global bodies still see gaps in execution against payment reform goals | Reform is no longer optional for the industry |

The common thread is simple: 2026 is not about one winner replacing all others. It is about multiple models competing to reduce friction in different ways.

Why this matters for banks, fintechs, and merchants

For banks

Banks can no longer rely on the idea that international payments are naturally complex and therefore acceptable as they are. Corporate clients and retail users increasingly compare the cross-border experience with local instant payments. If banks cannot offer more transparency and better integration, they risk losing parts of the user relationship to platforms, fintechs, or new orchestration layers. Swift’s retail push is, in part, a recognition of that pressure.

For fintechs

Fintechs still benefit from being more flexible in user experience design and corridor expansion. But fintech advantage now depends less on clever front-end design alone and more on how well they plug into local rails, compliance frameworks, and partner ecosystems. In other words, cross-border fintech is becoming more infrastructural.

For merchants and platforms

Merchants do not care much about theoretical payment architecture. They care about abandoned carts, unexpected fees, and payout uncertainty. Platforms care about conversion, dispute management, and local trust. That means the winners in cross-border payments will often be the players who make global payments feel boringly reliable, not necessarily technologically flashy.

The most important takeaway from cross-border payments news in 2026

The biggest shift in 2026 is not that one new technology has solved international payments. It is that the market has become much clearer about what “better” actually means.

Better cross-border payments now mean:

- faster where possible,

- predictable by default,

- transparent on cost,

- easier to connect across systems,

- and more compatible with digital commerce flows.

That is why the biggest stories this year are not random. They all point in the same direction. The FSB is warning that reform needs to move faster. Swift is redesigning the retail cross-border experience around predictability. Countries and networks are exploring more interoperability. Stablecoins and CBDCs are becoming part of the real payment-policy conversation rather than side topics.

Final thoughts

Cross-border payments in 2026 are shifting from a messaging problem to an experience problem.

The old system focused on transmitting payment instructions. The new competition is about delivering a payment experience that feels clear, reliable, and globally connected. That is the real story behind the headlines, and it is why this topic is likely to stay relevant far beyond a single news cycle.

References

- Reuters, FSB’s Bailey calls for international action on payment reforms (Reuters)

- Swift, Swift accelerates transformation of consumer payments as banks roll out new framework for retail transactions (Swift)

- Reuters, India in talks about allowing Alipay+ link to its instant payment systems (Reuters)

- Reuters, India’s central bank proposes linking BRICS’ digital currencies (Reuters)