Payment infrastructure explained for readers searching for payment infrastructure, payment rails, and digital payment systems

When people search for payment infrastructure, they are usually trying to answer one practical question: how does money actually move behind a payment? A card tap feels instant. A bank transfer looks simple. A digital wallet makes checkout feel effortless. But none of these experiences happen on their own.

Behind every transaction is a payment infrastructure. That payment infrastructure includes the systems, institutions, networks, rules, and settlement mechanisms that make modern payments work. Without payment infrastructure, there is no reliable way to move money between consumers, merchants, banks, payment service providers, and financial institutions.

If you want to understand payment infrastructure, you need to look beyond the app and into the system underneath it.

What is payment infrastructure?

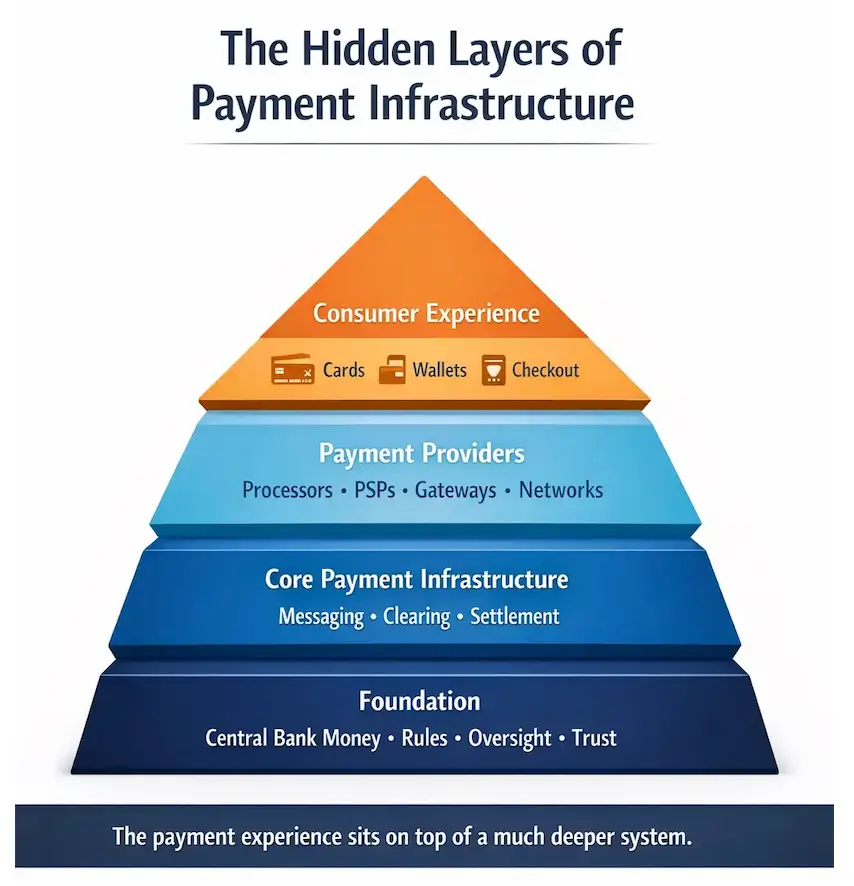

Payment infrastructure is the foundation that allows money to move safely, efficiently, and at scale. It is the hidden framework behind card payments, bank transfers, direct debits, digital wallets, real-time payments, and many cross-border transactions.

A good definition of payment infrastructure includes several layers:

- payment instruments such as cards, accounts, transfers, wallets, and direct debits

- payment networks that route payment instructions

- banks and payment service providers that connect users to the system

- clearing systems that calculate obligations between institutions

- settlement systems that move final funds

- rules, standards, compliance, and governance that make the system trusted and usable

So when someone asks, “What is payment infrastructure?” the answer is not just “the payment app” or “the payment processor.” Payment infrastructure is the full structure that makes a payment possible from start to finish.

Why payment infrastructure matters

Many people think payments are mainly about convenience. In reality, payment infrastructure is about much more than convenience. Good payment infrastructure supports commerce, improves trust, reduces friction, and keeps money moving across the economy.

Strong payment infrastructure matters because it helps deliver:

- reliable payment execution

- secure money movement

- lower operational risk

- scalable transaction processing

- better merchant settlement

- stronger system resilience

- support for innovation in fintech and digital commerce

In other words, payment infrastructure is not just a technical utility. Payment infrastructure is part of the core architecture of finance.

How the payment infrastructure works behind every payment

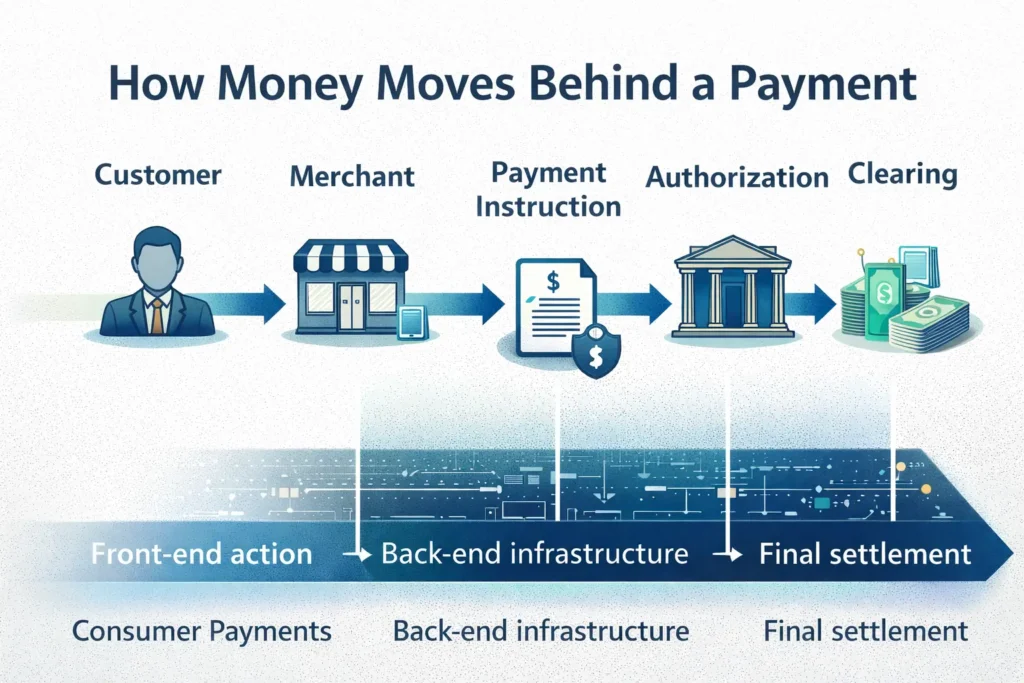

To understand payment infrastructure, it helps to break a payment into stages. Most people see only the front-end action. The real work happens in the background.

Step 1: Payment initiation

A customer starts the payment. They tap a card, enter bank details, approve a wallet payment, or click a checkout button.

This is the visible part of the process, but it is only the beginning of how payment infrastructure works.

Step 2: Authorization and routing

The payment request is sent through the relevant payment infrastructure. Depending on the transaction type, this may involve a merchant, a gateway, a processor, an acquiring bank, a card network, an issuing bank, or a transfer system.

At this stage, the system checks whether the transaction should be approved.

Step 3: Clearing

Clearing is a key part of payment infrastructure. It is the process of determining which institution owes money to another institution. Instead of moving money one transaction at a time in every case, the system can calculate obligations across many transactions.

This makes payment infrastructure more efficient.

Step 4: Settlement

Settlement is where final funds move between institutions. Settlement is one of the most important concepts in payment infrastructure, because this is the point where the transfer becomes final in the financial system.

A payment may look complete to a consumer before settlement actually happens. But from the perspective of payment infrastructure, final settlement is what matters most.

Payment infrastructure is not the same as payment rails

This is one of the most common points of confusion.

Payment rails are the pathways that carry payment messages and funds.

Payment infrastructure is the broader system that includes those rails plus the institutions, standards, risk controls, and settlement mechanisms around them.

A useful way to think about it is this:

- Payment rails are the route

- payment infrastructure is the whole transport network

That is why many fintech products do not replace payment infrastructure. In many cases, they simply build a smoother front-end experience on top of existing payment infrastructure.

The central bank plays a major role in payment infrastructure

Any serious explanation of payment infrastructure should include the central bank. The central bank is often one of the most important institutions in the entire payment infrastructure stack.

Why? Because the central bank is closely connected to final settlement, system stability, and trust in the payment system.

Central bank money supports safe settlement

In many financial systems, the safest settlement asset is central bank money. That makes the central bank highly relevant to payment infrastructure, especially for high-value transfers and systemically important payment flows.

Central banks support core payment infrastructure

In many countries, central banks operate, support, or oversee critical parts of payment infrastructure. This can include settlement systems, real-time gross settlement frameworks, and oversight of important payment systems.

Central banks help preserve trust and resilience

Payment infrastructure is not just about speed. It is also about legal certainty, operational continuity, liquidity management, and systemic safety. Central banks matter because failures in payment infrastructure can create wider financial instability.

Central banks matter in the future of payment infrastructure

As the market discusses CBDCs, tokenized money, stablecoins, and new digital payment models, the role of the central bank becomes even more important. Many innovations in front-end payments still depend on trusted back-end payment infrastructure.

Who operates payment infrastructure?

No single company runs all the payment infrastructure. Modern payment infrastructure is a shared system with several participants.

Banks

Banks are central to payment infrastructure because they hold accounts, move deposits, and connect customers and businesses to payment systems.

Payment service providers

Processors, gateways, acquirers, and fintech platforms are all part of the broader payment infrastructure landscape. They help merchants and users access payment functionality.

Card networks and transfer networks

These networks are important pieces of payment infrastructure because they transmit information, apply rules, and coordinate transaction flows.

Clearing houses and settlement institutions

These institutions are core components of payment infrastructure because they calculate obligations and support final money movement.

Central banks

Central banks anchor the most critical layer of payment infrastructure through settlement assets, system oversight, and resilience standards.

Types of payment infrastructure

When people search for payment infrastructure, they often imagine only card networks. But payment infrastructure covers many payment types.

Card payment infrastructure

This includes issuers, acquirers, card networks, processors, merchant systems, and settlement flows.

Bank transfer infrastructure

This includes ACH-type systems, wire systems, domestic account-to-account transfer systems, and real-time bank payment infrastructure.

Real-time payment infrastructure

Real-time payment infrastructure is designed to move payment messages and often funds much faster, sometimes within seconds, while operating on a continuous basis.

Cross-border payment infrastructure

Cross-border payment infrastructure includes correspondent banking relationships, international messaging systems, FX layers, compliance controls, and settlement arrangements across jurisdictions.

Digital wallet infrastructure

Wallets may look simple to consumers, but the wallet experience still depends on underlying payment infrastructure such as account connectivity, card tokenization, transfer rails, and settlement systems.

Why payment infrastructure is becoming more important in fintech

In fintech, many of the biggest changes are not just happening at the app layer. They are happening deeper in the payment infrastructure.

This is why payment infrastructure is now a major topic in:

- real-time payments

- open banking

- embedded finance

- merchant acquiring

- cross-border payment modernization

- wallet ecosystems

- stablecoin payments

- CBDC discussions

As competition in digital payments grows, companies are trying to improve not only the user interface but also the underlying payment infrastructure. Better payment infrastructure can improve speed, cost, reliability, interoperability, and control over the payment experience.

What makes a good payment infrastructure?

Not all payment infrastructure is equally strong. Good payment infrastructure usually has a few important qualities.

Reliability

The system must work consistently, even under heavy volume.

Security

A good payment infrastructure must protect payment instructions, sensitive data, and final funds.

Scalability

As transaction volume grows, payment infrastructure must keep up without breaking down.

Finality

A payment system needs clarity on when settlement is legally and operationally final.

Resilience

Good payment infrastructure must continue operating during outages, fraud attempts, cyber risks, and operational disruptions.

Interoperability

Modern payment infrastructure increasingly needs to connect with other systems, institutions, and payment models.

Payment infrastructure is the invisible layer behind digital commerce

Consumers often remember the app they used, the wallet they tapped, or the checkout flow they liked. But what actually makes digital commerce possible is payment infrastructure.

That is why payment infrastructure matters so much. It is the layer that supports trust, movement of value, and large-scale economic activity. It is also the layer where major strategic questions are being decided:

- Who controls customer access?

- Who owns the payment relationship?

- Who handles the final settlement?

- Who carries liquidity and operational risk?

- Who defines the standards of modern payment infrastructure?

These are not small questions. They shape the future of payments.

Final thoughts

If you searched for payment infrastructure, the most important takeaway is this: payments are never just about the button, the app, or the card. Payments depend on a deeper system that makes money movement possible.

That deeper system is the payment infrastructure.

Payment infrastructure includes the rails, the institutions, the messaging, the clearing, the settlement, the rules, and the trust architecture behind every payment. Whether you are looking at bank transfers, card payments, real-time payments, wallets, or new digital money models, payment infrastructure is the foundation that holds the system together.

If you want to understand how money actually moves behind every payment, you need to understand payment infrastructure first.

References

Principles for Financial Market Infrastructures (PFMI)