Why Finance Is Quietly Moving Inside Everything

A funny thing happened in digital finance.

For years, financial services acted like the main character. If you wanted to move money, verify an account, check a balance, or apply for a financial product, you had to go where the bank or fintech app told you to go. Their app. Their website. Their experience. Their rules.

Now the script is flipping.

Finance is no longer trying to pull users into a separate destination. It is slipping into the background and becoming part of the product itself. That shift is exactly why open banking-based embedded finance architecture matters. It is the structure that allows platforms to turn payments, account connectivity, verification, cash flow visibility, and even lending into features that live naturally inside software.

And when it is done well, users barely notice.

That is the magic.

They are not thinking, “Wow, what a beautiful financial infrastructure layer.” They are thinking, “Nice, that was easy.”

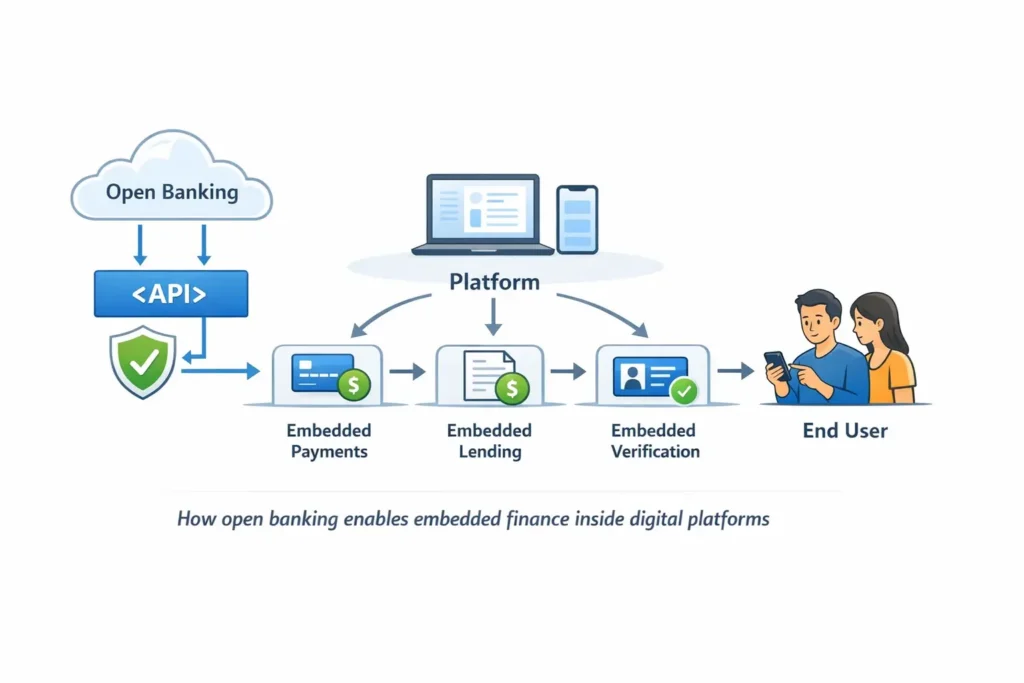

What Open Banking-Based Embedded Finance Actually Means

At its core, open banking-based embedded finance is about combining two ideas.

The first is open banking. This allows users to securely share bank account data or enable bank-connected payment actions through APIs and consent-based access.

The second is embedded finance. This is what happens when financial services are integrated directly into non-financial products like SaaS platforms, marketplaces, e-commerce tools, logistics software, procurement systems, or creator platforms.

Put them together, and you get a system where finance stops feeling like a detour.

A marketplace can let sellers connect bank accounts and receive payouts without leaving the dashboard. A procurement platform can approve invoices and initiate payment in one workflow. A software platform can verify accounts, surface financial insights, and eventually offer working capital without pushing users into another app.

That is not just convenience. That is product strategy.

Why This Architecture Feels So Powerful

The reason this model is getting so much attention is simple: it removes friction from moments where friction used to be normal.

Old world:

You do something in one platform, then leave to deal with the money somewhere else.

New world:

You do the work and the money part happens right there inside the same experience.

That sounds small until you realize how often that handoff used to break things.

Users drop off. Payments get delayed. Reconciliation becomes messy. Teams waste time checking whether something was paid, approved, settled, or verified. The more steps involved, the more chances the process has to become annoying.

Open banking-based embedded finance architecture reduces that awkward gap between action and transaction.

And in digital products, reducing awkwardness is often where the money is.

The Architecture Behind the Curtain

The front end may look sleek and effortless, but under the hood this architecture has several layers working together.

| Layer | Role | What It Really Means |

|---|---|---|

| User Experience Layer | Handles bank linking, consent, payment actions, and status views | The part users see and judge immediately |

| Platform Logic Layer | Controls workflow rules, triggers, routing, and reconciliation logic | The brain of the product |

| Open Banking API Layer | Connects the platform to bank data and payment capabilities | The pipe connecting software to money |

| Consent and Compliance Layer | Manages permissions, authentication, privacy, and auditability | The trust layer nobody can afford to ignore |

| Financial Services Layer | Supports payments, payouts, verification, lending, and more | The revenue-producing capability layer |

| Partner Ecosystem Layer | Includes banks, BaaS providers, fraud vendors, and compliance partners | The supporting cast that makes scale possible |

This is why the topic is more interesting than it first appears.

A clean user journey may be powered by APIs, yes. But it is also powered by consent design, exception handling, ledger logic, fraud checks, orchestration, and operational discipline. Embedded finance is never just about adding a button that says “Pay now.”

That button has a lot of emotional support behind it.

How the Flow Works in Practice

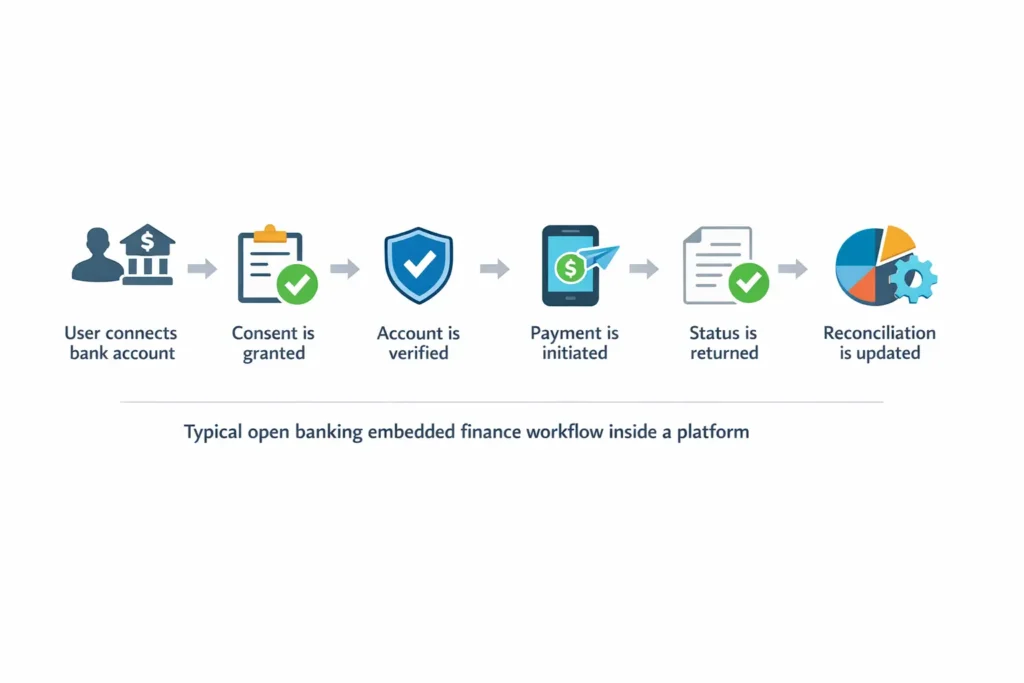

Imagine a B2B platform used by finance teams to manage suppliers and invoices.

A buyer reviews an invoice and clicks approve. Instead of downloading the file, opening a separate banking portal, re-entering payment details, and then sending a confirmation screenshot to someone who will probably still ask if it went through, the platform lets the user connect a bank account and initiate payment directly inside the workflow.

The user grants permission.

The account is verified.

The payment is triggered.

The status is returned.

The records are updated.

The reconciliation process begins automatically.

From the user’s perspective, it feels smooth and logical.

From the platform’s perspective, the system has just coordinated authentication, authorization, account data access, payment initiation, status tracking, internal record updates, and permission management in one journey.

That is what good architecture does. It makes complicated things feel obvious.

Open Banking Is the Engine. Embedded Finance Is the Experience.

These terms are often mashed together like they are interchangeable, but they are not.

Open banking is mostly about secure access to financial data and bank-connected payment functionality.

Embedded finance is about where financial services show up and how they are presented to the user.

Open banking gives the platform access to the rails. Embedded finance gives the platform a reason to use them in a meaningful, contextual way.

If open banking is the engine, embedded finance is the car.

And nobody brags about owning a great engine if the car itself is ugly, confusing, and stalls at traffic lights.

The Real Business Advantage

What makes this architecture so powerful is not just the technology. It is the business effect.

When finance becomes part of the product, platforms can do several things better at once.

They can improve conversion because users do not need to jump across systems.

They can improve retention because the product becomes more deeply embedded in daily operations.

They can create new revenue streams from payments, premium tools, financing, or workflow automation.

They can improve data visibility and reduce operational mess.

They can make the overall experience feel smarter, faster, and more complete.

This is why so many platforms are suddenly interested in becoming “financially enabled,” even if they have no intention of becoming a bank in the traditional sense.

They do not want to be banks.

They want to own the moment where money moves.

That is a different ambition, and in many cases, a smarter one.

Where This Model Works Best

Open banking-based embedded finance is especially effective in products where money is already adjacent to workflow.

Marketplaces

Marketplaces can connect buyers, sellers, payouts, and settlement reporting inside one product environment. Instead of handling money as an external process, they can make it part of the core transaction experience.

B2B SaaS Platforms

Accounting software, procurement tools, expense platforms, and invoicing products can embed bank connectivity, payment initiation, account verification, and reconciliation support.

E-commerce and Merchant Platforms

Platforms can use bank-based payment methods, account verification, payouts, and cash flow tools to create a more integrated merchant experience.

Vertical SaaS

Industry-specific software in logistics, healthcare, hospitality, property management, or education can add finance in ways that feel highly relevant to the user journey.

Creator and Gig Platforms

Fast payouts, linked accounts, income visibility, and short-term financial products can be embedded directly into the app environment.

The common thread is simple: embedded finance works best when it solves a real problem at the exact moment the user has it.

Why the Hard Part Is Not the API

Here is where many teams get humbled.

They assume the challenge is getting connected. In reality, the challenge is what happens after the connection.

The tricky part is not just plugging into an open banking provider. The tricky part is designing for reality.

Reality includes:

- users abandoning the flow halfway through

- permissions expiring at annoying times

- payment status updates arriving late

- duplicate events showing up when no one invited them

- reconciliation mismatches that create finance team headaches

- confusing consent experiences that kill trust

- bank-specific inconsistencies

- fraud risks that grow as money movement becomes easier

This is why strong architecture matters.

Not because it sounds impressive in a strategy deck, but because weak architecture becomes painfully visible the second real users start doing real things with real money.

And real money has a way of exposing bad design faster than almost anything else.

What Good Design Looks Like

If a platform wants to build open banking-based embedded finance properly, a few design principles matter more than the rest.

Make Consent Feel Clear, Not Threatening

Users should understand what they are agreeing to, why access is needed, how long it lasts, and what they can control. Confusion destroys trust faster than almost anything in finance.

Treat Reconciliation as a First-Class Citizen

If the system cannot reliably match payment events, invoices, balances, and settlement records, scale quickly becomes painful.

Build for the Messy Cases

Happy paths are nice in product demos. Real systems need to survive broken flows, missing updates, expired permissions, interrupted sessions, and edge cases that arrive at the worst possible moment.

Start With One Strong Use Case

A focused launch usually beats a bloated one. Account verification, payout setup, or pay-by-bank can be a far smarter starting point than trying to launch five financial products at once.

Keep the Stack Modular

The best systems do not paint themselves into a corner. They allow expansion into payouts, recurring payments, lending, treasury tools, or richer data services without forcing a total rebuild.

Good architecture is not about stuffing in every possible feature.

It is about leaving room for the product to grow up properly.

Why This Space Keeps Getting More Interesting

There is something oddly satisfying about watching finance become less visible and more important at the same time.

That is exactly what is happening here.

The future of digital finance may not belong to the loudest standalone app with the flashiest branding. It may belong to the platforms that make financial actions feel so natural, so embedded, and so frictionless that users no longer think of them as “financial services” at all.

They just think of them as part of getting things done.

And that may be the biggest shift of all.

Because once finance becomes infrastructure inside everyday software, the winners are no longer the companies that shout the loudest about innovation. They are the ones that quietly remove the most friction from how people and businesses move money.

That is what open banking-based embedded finance architecture really is.

Not just a technical model.

Not just an API story.

Not just another fintech buzzword trying to sound expensive.

It is the design pattern behind a world where finance stops interrupting the user and starts helping them.