Lower fees are attractive, but conversion, trust, and customer behavior still decide what wins at checkout

A2A payments are getting more attention for a simple reason: merchants are tired of paying card fees on every transaction. If money can move directly from one bank account to another, why keep giving up margin to card networks, issuers, acquirers, and processors?

That question sounds obvious. The answer is not.

For many merchants, A2A payments look like the smart future. They promise lower costs, faster access to funds, and a payment flow that feels more direct. Card payments, on the other hand, still dominate because they are familiar, fast, trusted, and deeply built into online shopping behavior.

So this is not really a story about old payments versus new payments. It is a story about what merchants actually need: lower cost, strong conversion, fewer failed payments, manageable risk, and a checkout experience customers do not abandon halfway through.

What A2A payments actually mean

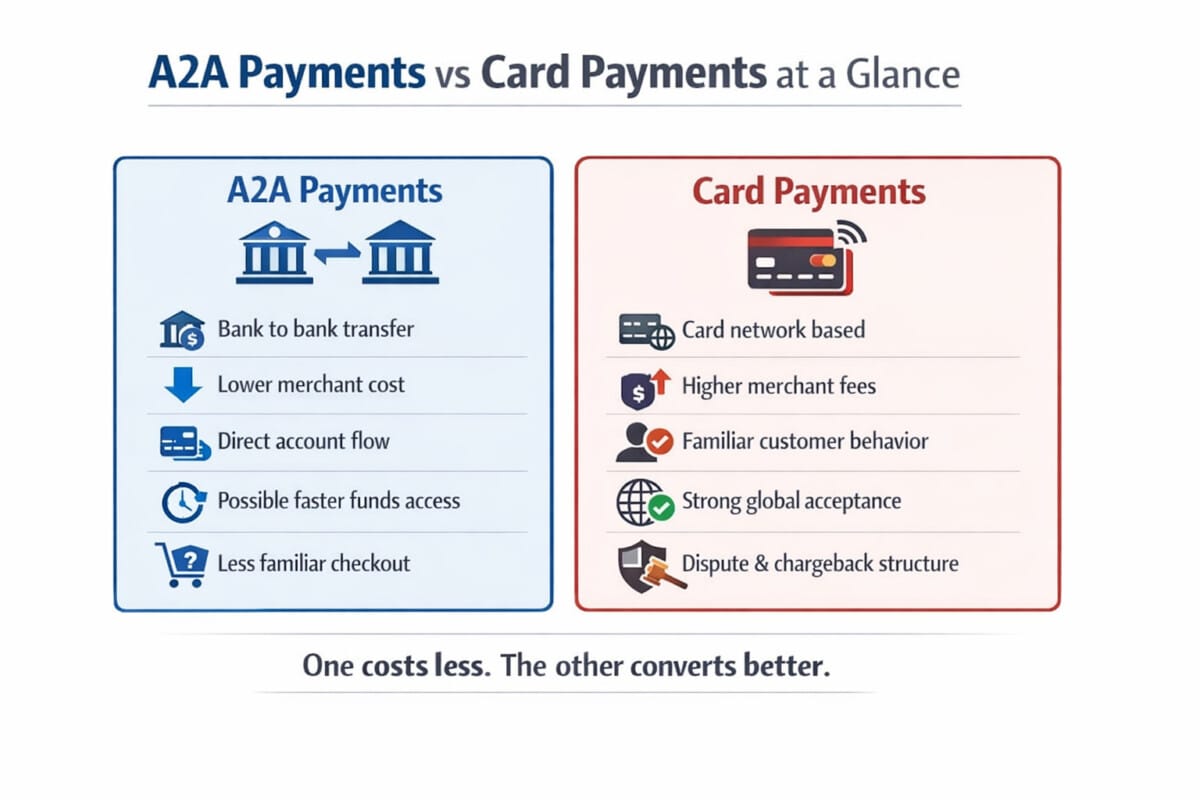

A2A stands for account-to-account payments. Instead of charging a credit or debit card, the payment moves directly from the customer’s bank account to the merchant’s bank account. In different markets, this may appear as pay by bank, bank transfer checkout, instant bank payment, or open banking payment.

The appeal is easy to understand. Fewer intermediaries can mean lower processing costs. Real-time payment infrastructure can also mean faster settlement or faster access to funds. For merchants that care deeply about margin, especially in low-margin sectors, that sounds like a major upgrade.

But a cheaper payment method is not automatically a better payment method. Merchants do not get paid simply because the cost per transaction is lower. They get paid when customers complete the purchase.

Why merchants are paying attention to A2A now

For years, card payments were the default answer to online commerce. They still are. But merchant priorities have changed.

Growth is harder to find. Customer acquisition is expensive. Margins are under pressure. Finance teams are looking more closely at payment costs, failed payments, chargebacks, and settlement timing. At the same time, real-time payment rails and open banking-based payment flows have made A2A more practical than it used to be.

That is why A2A is no longer just an infrastructure topic for payment insiders. It is becoming a commercial topic. Merchants are now asking whether payment choice can improve profitability, not just payment acceptance.

And that is where the comparison with cards becomes interesting.

The merchant case for A2A payments

The strongest argument for A2A is cost.

Card payments are powerful, but they are not cheap. Every card transaction carries a stack of economics that merchants feel very clearly. Even when the customer sees a smooth one-click checkout, the merchant may be looking at a very different picture in the background: fees, retries, fraud tools, chargeback exposure, settlement timing, and reconciliation work.

A2A payments offer a different path. Because the payment is based on a direct bank-to-bank movement of funds, the cost structure can be more appealing. For merchants with large transaction volumes, even a small reduction in payment cost can add up quickly.

There is also a cash-flow story here. In a world of instant payments, access to funds can matter almost as much as revenue itself. Faster availability of funds can improve working capital, reduce funding pressure, and make treasury operations easier.

That is why A2A tends to look especially attractive in use cases such as bill payments, account funding, insurance payouts, brokerage transfers, debt repayment, and other bank-native financial flows. In those environments, bank-based payment behavior already feels natural.

Why cards are still incredibly hard to replace

If lower cost were the only thing that mattered, A2A would already be much bigger.

Cards remain powerful because they solve more than one problem at the same time. They do not just move money. They reduce friction. They are familiar. They are globally accepted. They work across borders. They support stored credentials, subscriptions, tokenization, and fast repeat purchases. Most importantly, customers know how to use them without thinking.

That last point matters more than many merchants admit.

People do not buy with payment rails. They buy with habit.

A shopper who sees a card form knows exactly what to do. A shopper who sees a familiar wallet button often moves even faster. But a shopper who is asked to connect a bank account, approve bank access, switch apps, authenticate differently, or think about a new payment method may pause. And even a brief pause can damage conversion.

This is the part many payment discussions miss. The cheaper payment route is not always the more profitable one. If a lower-cost payment method introduces hesitation, confusion, or drop-off, the merchant may end up saving on fees while losing actual sales.

That is not a winning trade.

The real battle is not fees. It is conversion.

Merchants often begin the A2A conversation with cost, but they usually end up at conversion.

Imagine two payment options. One costs more but customers trust it instantly. The other costs less but creates just enough friction to reduce completion rates. Which one is better?

The answer depends on the business model.

For impulse purchases, everyday ecommerce, mobile checkout, and cross-border retail, conversion usually rules the conversation. In these environments, cards still hold a strong advantage because they are already embedded in customer behavior.

For planned payments, invoice settlement, recurring bill scenarios, account top-ups, or financial account movements, A2A may fit the customer mindset much better. In these cases, the customer is often less surprised by a bank-based flow, and the merchant has more room to trade convenience for efficiency.

That is why the future is unlikely to be a clean replacement story. A2A is not simply “the new card.” In many cases, it is a complementary rail that works better in specific moments.

Trust changes everything

There is another reason card payments remain so strong: trust.

Customers do not always understand the technical details of card payments, but they understand the feeling of protection around them. If something goes wrong, they believe there is a process. They expect disputes to be possible. They expect unauthorized transactions to be handled. They expect a structure they can lean on.

Merchants may dislike chargebacks, but consumers often see them as part of the safety net.

That creates an uncomfortable truth for merchants. One of the reasons card payments are expensive and operationally painful is also one of the reasons customers are willing to use them.

A2A can feel different. In many bank-based payment flows, the payment experience is more immediate and more final. That can be operationally attractive, but it can also make customers wonder what happens if there is a mistake, a scam, or a problem with the purchase.

Trust at checkout is not just a compliance matter. It is a commercial asset.

A payment method that feels slightly less safe can underperform even if it is cheaper and technically efficient.

Where A2A payments can outperform cards

This does not mean A2A is weak. It means it wins in different places.

A2A can shine when the merchant wants to reduce cost on high-volume transactions, when the payment amount is large enough that card economics hurt, or when the use case already feels connected to banking behavior.

It can work well in recurring account-based relationships, invoice and bill payment journeys, wallet funding, brokerage account transfers, insurance disbursements, utility payments, rent, education payments, and other scenarios where the customer is already thinking in terms of bank accounts rather than shopping carts.

In those environments, A2A may not feel like a compromise. It may feel like the natural option.

And when real-time payment infrastructure is available, the speed advantage can become much more meaningful from a treasury and operations perspective.

Where cards still dominate

Cards remain strongest where convenience and certainty matter most.

They are hard to beat in consumer ecommerce, digital goods, international commerce, subscription models with mature credential-on-file strategies, and high-frequency online shopping behavior. They are also deeply supported by payment platforms, fraud tools, orchestration layers, and merchant reporting systems.

A merchant may dislike card costs and still keep cards front and center because removing them would immediately hurt sales.

That is the practical reality. Payment leaders may admire efficiency, but revenue teams usually protect conversion first.

A simple side-by-side view

| Category | A2A Payments | Card Payments |

|---|---|---|

| Cost to merchant | Often more attractive | Usually higher |

| Customer familiarity | Still growing in many markets | Extremely high |

| Checkout friction | Can be higher depending on flow | Usually lower |

| Settlement speed | Can be very fast with real-time rails | Often separate from authorization |

| Consumer protection feel | Varies by market and structure | Strong and familiar |

| Cross-border reach | More limited | Much stronger |

| Best fit | Bank-native payments, bills, transfers, account funding | Ecommerce, global commerce, fast checkout, repeat purchases |

So what should merchants actually do?

Most merchants should stop asking which payment method is better in absolute terms.

That is the wrong question.

The better question is: which payment method is better for this customer, this transaction type, and this moment in the buying journey?

For many merchants, the smartest strategy is not replacing cards with A2A. It is using both more intentionally.

Cards can protect conversion, support familiar checkout behavior, and keep cross-border acceptance strong. A2A can reduce cost, improve economics on selected flows, and create better outcomes in bank-native payment contexts.

That is where payment strategy becomes more interesting. The goal is not to choose a winner. The goal is to design a payment mix that improves profit without damaging revenue.

In other words, merchants do not need a payment ideology. They need payment judgment.

Final thoughts

A2A payments are not just a cheaper alternative to cards. They are part of a bigger shift in how merchants think about payment performance. Cost matters more than it used to. Speed matters more than it used to. Control matters more than it used to.

But card payments are not standing still, and they are not easy to displace. They still win on familiarity, reach, and trust. In many parts of commerce, those strengths are worth paying for.

That is why the real future is unlikely to be A2A versus cards in a dramatic winner-takes-all battle.

The real future is more selective than that.

Some payment moments will belong to cards because customers want speed, familiarity, and reassurance. Others will belong to A2A because merchants want better economics and more direct payment flows.

The merchants who benefit most will not be the ones who chase the newest rail. They will be the ones who understand exactly where each rail performs best.

References

- Open Banking Limited. Open Banking in 2025: Now Part of the UK’s Everyday Financial Life. January 29, 2026. https://www.openbanking.org.uk/insights/open-banking-in-2025-now-part-of-the-uks-everyday-financial-life/

- Federal Reserve Financial Services. About the FedNow Service. https://www.frbservices.org/financial-services/fednow/about.html

- Board of Governors of the Federal Reserve System. Pay-by-Bank and the Merchant Payments Use Case: Benefits, Risks and Potential Impacts on Consumer Payment Behaviors in the U.S. July 7, 2025. https://www.federalreserve.gov/econres/notes/feds-notes/pay-by-bank-and-the-merchant-payments-use-case-benefits-20250707.html