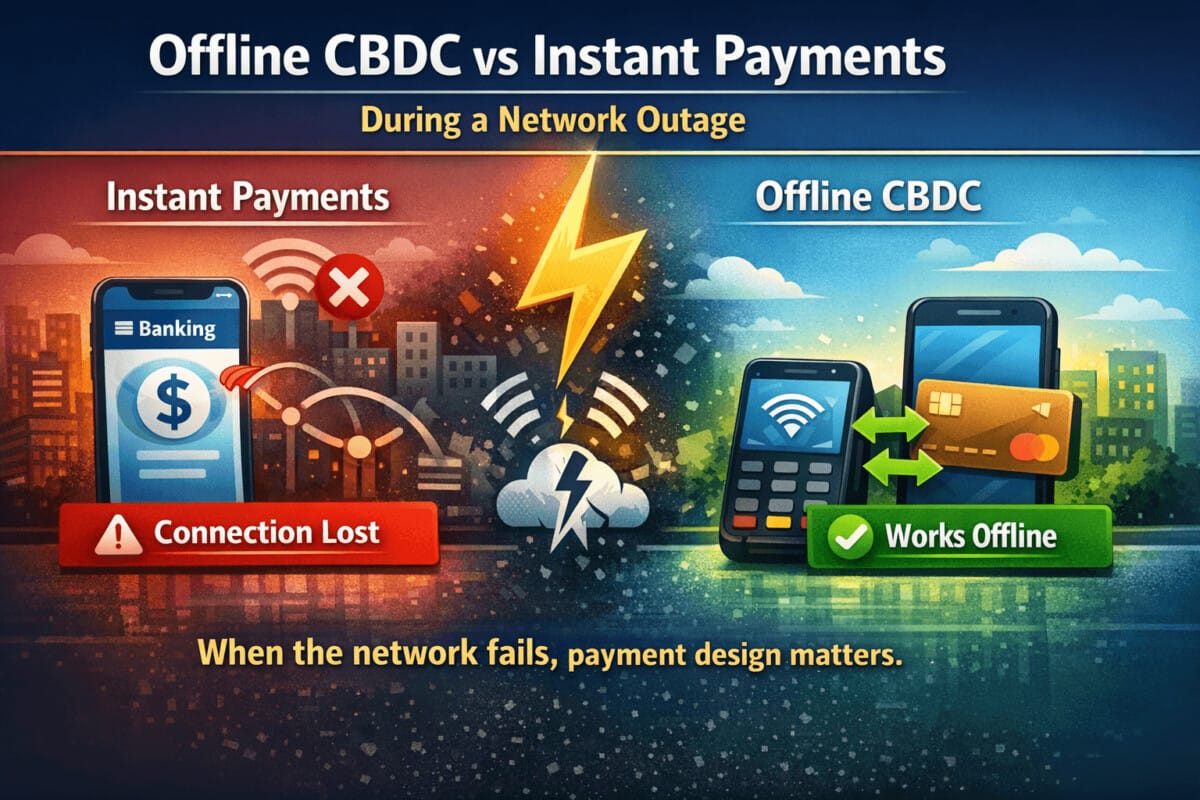

When the network fails, payment design suddenly matters

Most people do not think about payment infrastructure until it stops working. On an ordinary day, instant payments feel fast enough, reliable enough, and invisible enough that the system seems almost effortless. Money moves in seconds, QR codes work, banking apps refresh, and merchants get paid. But a network outage changes the question completely. The issue is no longer which payment method feels smoother in normal conditions. The real question becomes much simpler and more serious: which payment rail still works when connectivity breaks down?

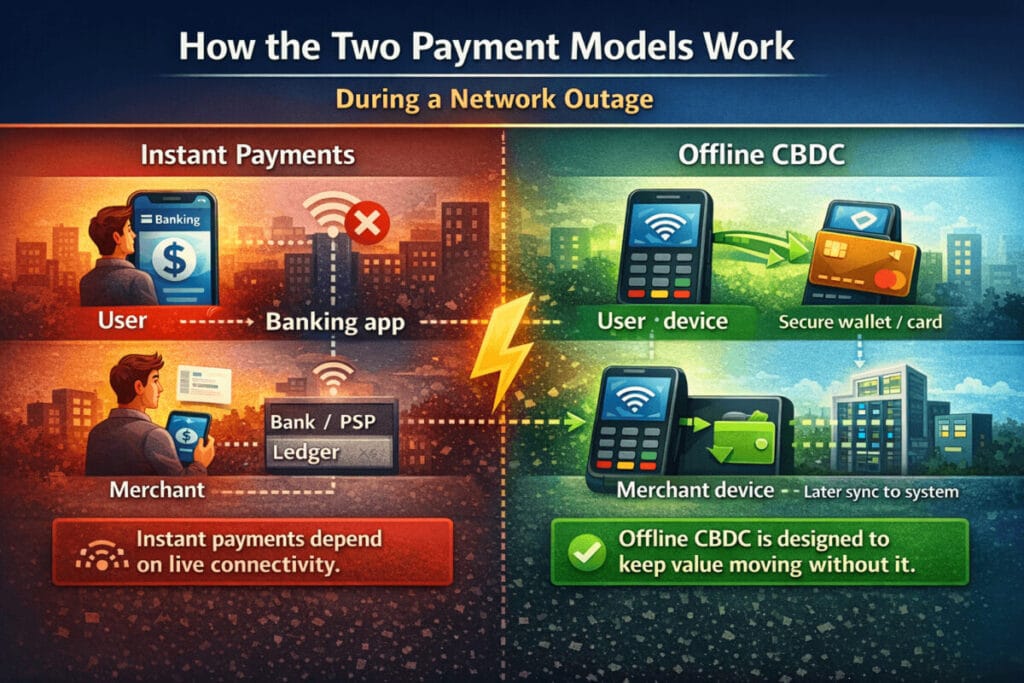

That is where the comparison between offline CBDC and instant payments becomes interesting. In normal conditions, instant payments usually look stronger. They are familiar, widely adopted, and built on top of existing banking relationships. But during network outages, offline CBDC may have a very different advantage. According to the BIS, some central banks view offline payments as easier to achieve with a retail CBDC system than with a fast payment system, because offline payments can be designed to work without a connection to any ledger system. In contrast, instant payments typically depend on communication with the bank or PSP ledger to update balances and complete the transaction.

Why are instant payments strong in normal times

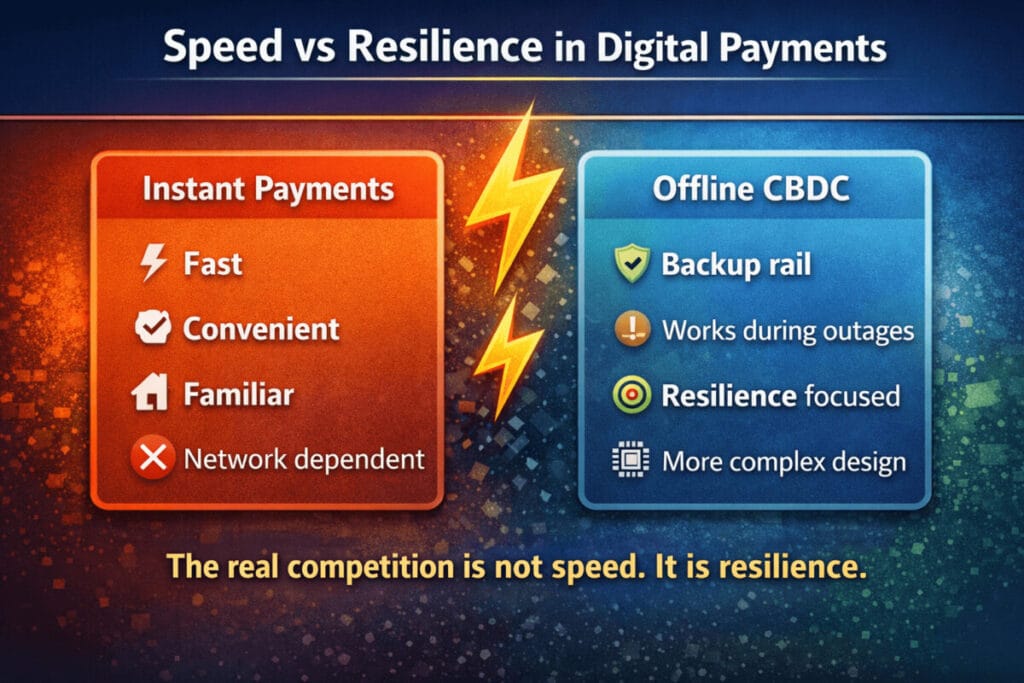

There is a reason instant payments have become one of the most important trends in modern retail finance. They are practical. They are scalable. And they usually fit into the systems people already use. Consumers do not need to learn a new form of money, and merchants do not need to rethink settlement from scratch. In many markets, instant payments already provide the thing consumers care about most: fast and easy digital transfers.

This matters because payment adoption is rarely driven by technology alone. It is driven by habits, trust, and convenience. If a customer can already send money from a banking app in seconds, the case for a new consumer-facing payment instrument becomes harder to explain. That is one reason the BIS frames retail CBDC and fast payment systems as potentially rivals or partners, depending on the market context. Both can deliver instant transactions to end users, but they are not the same kind of money. Instant payments move private money, while retail CBDC would represent a direct claim on the central bank, more like digital cash.

In everyday life, that difference may not feel urgent. During a network outage, it can become central.

Why network outages expose the limits of instant payments

Instant payments are fast, but they are still fundamentally online systems. That sounds obvious, but it matters more than it seems. To complete a transfer safely, the system usually needs to verify balances, authenticate the transaction, update the ledger, and communicate with relevant institutions or intermediaries. If the telecom network is down, if the internet connection is unstable, or if a key bank or PSP system is unavailable, the payment experience can deteriorate very quickly.

This is the hidden trade-off of highly efficient digital finance. In good times, network dependence is barely noticeable. In bad times, it becomes the system’s main vulnerability.

That does not mean instant payments are weak. In fact, they are often the best solution for day-to-day retail payments. But they are optimized for continuous connectivity, not for disconnected operation. And that is exactly the scenario where offline CBDC begins to look less like a theoretical experiment and more like a resilience tool.

Offline CBDC is not about speed. It is about resilience.

The biggest mistake in this debate is to think of offline CBDC as just another way to make payments faster. That is not the most interesting part. The real value of offline CBDC is that it aims to preserve payment functionality when the network itself is unavailable.

The BIS Project Polaris handbook defines an offline CBDC payment as a transfer of value between devices that does not require connection to any ledger system, often in the absence of internet or telecom connectivity. That definition is crucial. Offline CBDC is not simply a faster online system. It is a design approach intended to keep value moving when a normal online payment rail cannot function. The same handbook also notes that offline payments may be needed because of system outages or the absence of internet or telecommunications connectivity.

This is why offline CBDC should be understood less as a competitor to instant payments in normal times and more as a backup payment layer. It is closer to the logic of emergency infrastructure than to the logic of everyday app convenience.

That framing also fits ongoing official work in Europe. The ECB has stated that technical work on the digital euro has focused on enabling offline payments via card or phone through secure environments, including embedded secure elements and eSIM-related approaches. The ECB also emphasizes that offline payments can improve privacy by keeping sensitive payment information on the device and inaccessible to both the Eurosystem and PSPs.

A simple comparison

| Feature | Instant Payments | Offline CBDC |

|---|---|---|

| Main strength | Speed and convenience | Resilience during connectivity problems |

| Dependency on network | High | Can be designed to operate without ledger connectivity |

| Everyday usability | Usually strong | Depends on device design and rollout |

| Infrastructure fit | Works well with existing bank rails | May require new wallet, card, or secure hardware layers |

| Role in a crisis | May struggle if networks or ledgers are unavailable | Can function as a fallback rail in some outage scenarios |

| Core promise | Fast digital transfers | Continuity of payment when online rails fail |

This table captures the core idea: instant payments are built to perform in normal conditions, while offline CBDC is built to matter in abnormal ones.

But offline CBDC is much harder than it sounds

This is where the topic gets even more interesting. Offline CBDC sounds attractive in a crisis, but it is not an easy design problem. Once a payment can happen without checking a central ledger in real time, difficult questions appear immediately.

How do you prevent double-spending?

How do you authenticate the devices?

How much value should a user be allowed to hold or transfer offline?

What happens if the device is lost, stolen, damaged, or out of battery?

Should the system use a phone, a card, or a dedicated device?

The BIS handbook makes clear that offline CBDC is not one single model. It distinguishes between fully offline, intermittently offline, and staged offline systems. In a fully offline system, payer and payee do not need to connect to a ledger system to complete a payment, and final settlement can occur offline. In an intermittently offline system, offline risk parameters may eventually require the device to reconnect. In a staged offline system, value can be exchanged offline, but final settlement for the payee occurs later when the system reconnects.

That classification matters for SEO and for substance. It shows that offline CBDC is not just a yes-or-no feature. It is a set of design choices, each with different trade-offs in security, usability, and risk.

The same BIS material also notes that limits may be needed, including restrictions on the number of offline transactions before reconnecting to the ledger system. In other words, resilience comes with constraints.

So which works better during network outages?

If the question is strictly about network outages, the answer leans toward offline CBDC.

Not because offline CBDC is simpler. It is not.

Not because offline CBDC is more scalable today. It often is not.

Not because consumers would necessarily prefer it in everyday life. Many might not.

It works better during network outages because it is designed for exactly that kind of stress scenario. Instant payments depend on live communication with account-based infrastructure. Offline CBDC, if implemented well, is specifically meant to preserve value transfer even when that communication is disrupted. The BIS explicitly notes that offline payments can be made in the absence of internet or telecom connectivity, while such conditions make it difficult to communicate with a fast payment system and update the ledgers of the payer and payee.

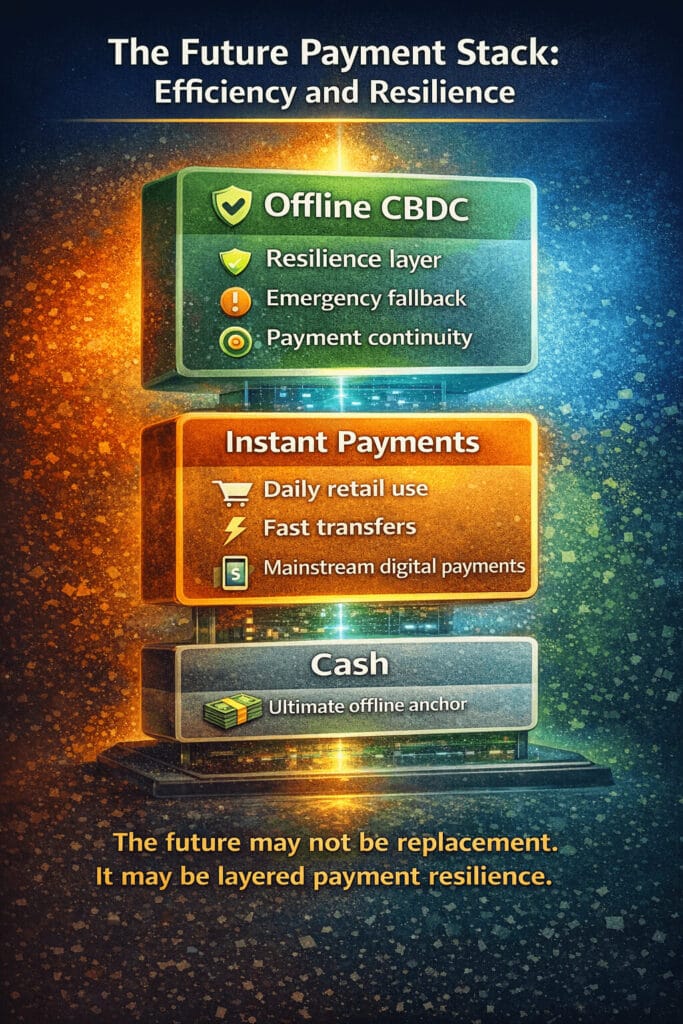

That makes offline CBDC less of a flashy replacement for modern payments and more of a digital continuity mechanism.

The more useful way to think about this debate

The wrong way to frame this topic is to ask which system should “win” in all circumstances. That framing is too simple.

A better question is this:

Which payment rail is optimized for ordinary life, and which one is optimized for failure scenarios?

Instant payments are optimized for ordinary life. They are efficient, fast, and already embedded in the current financial system. Offline CBDC is optimized for a narrower but increasingly important problem: how to keep payments running when the network does not cooperate.

That is why the two systems may not be true enemies. In some markets, they may end up serving different layers of the same payment ecosystem. Instant payments can remain the default rail for normal retail activity. Offline CBDC can exist, if it is introduced at all, as a resilience layer, a public fallback, or a digital cash-like option for outage scenarios.

That also makes this topic highly searchable from an SEO perspective. Users looking for terms such as offline CBDC vs instant payments, payments during network outages, offline payments without internet, or CBDC resilience are often looking for a very specific answer: not whether CBDC is fashionable, but whether it solves a real infrastructure problem.

The real takeaway

The best payment systems are not only fast. They are also resilient.

In normal times, instant payments will usually feel more practical than offline CBDC. They are already integrated, familiar, and effective. But during network outages, the comparison changes. In that environment, offline CBDC has a stronger conceptual advantage because it is built around the possibility that the online world may temporarily fail.

So the most accurate conclusion is not that offline CBDC will replace instant payments. It is that instant payments and offline CBDC solve different problems.

One is about everyday efficiency.

The other is about payment continuity under stress.

And when the network fails, continuity becomes the more important test.