Faster payments are easy to love

24/7 Instant payments look like an obvious upgrade. Money moves in seconds, weekends stop mattering, and bank transfers finally feel as fast as the rest of the internet. That is exactly why fast payment systems keep spreading. The BIS describes fast payment systems as infrastructure that ensures the immediate availability of funds for the recipient, and notes that these systems are increasingly built around near-constant availability rather than traditional business hours.

For consumers and businesses, that sounds like pure progress. A supplier gets paid on Saturday night. A family member receives emergency funds at midnight. A gig worker does not have to wait until Monday morning. In product terms, instant payments solve a very visible pain point: time. But once banks promise payments that move every hour of every day, they create a less visible problem behind the scenes. They need liquidity that is ready every hour of every day too.

That is where the story gets more interesting. The real challenge of 24/7 instant payments is not just speed. It is liquidity.

The hidden cost of “always on” payments

A bank can make a payment look instant on a mobile screen. It cannot magically make liquidity frictionless. Every payment system still depends on settlement, account balances, funding windows, and operational constraints. When payment activity shifts from “during banking hours” to “at any time,” liquidity management becomes much harder.

In the old world, banks could manage funding and payment flows around a predictable day. Treasury teams knew when core systems were open, when central bank money could be moved, and when large outflows were likely to happen. In the new world, customers can push funds out on a Sunday evening just as easily as on a Tuesday morning. The payment instruction may be immediate, but the bank’s ability to adjust liquidity is not always equally immediate. That mismatch is the new pressure point.

The Federal Reserve’s design for the FedNow Service makes this point especially clear. FedNow includes a dedicated liquidity management transfer capability so participants can move funds to support payment activity. That feature exists for a reason: instant payments do not work smoothly unless liquidity can also be repositioned quickly and reliably.

Why settlement design matters more than most people think

Not all instant payment systems create the same liquidity burden. The pressure depends heavily on how settlement is structured.

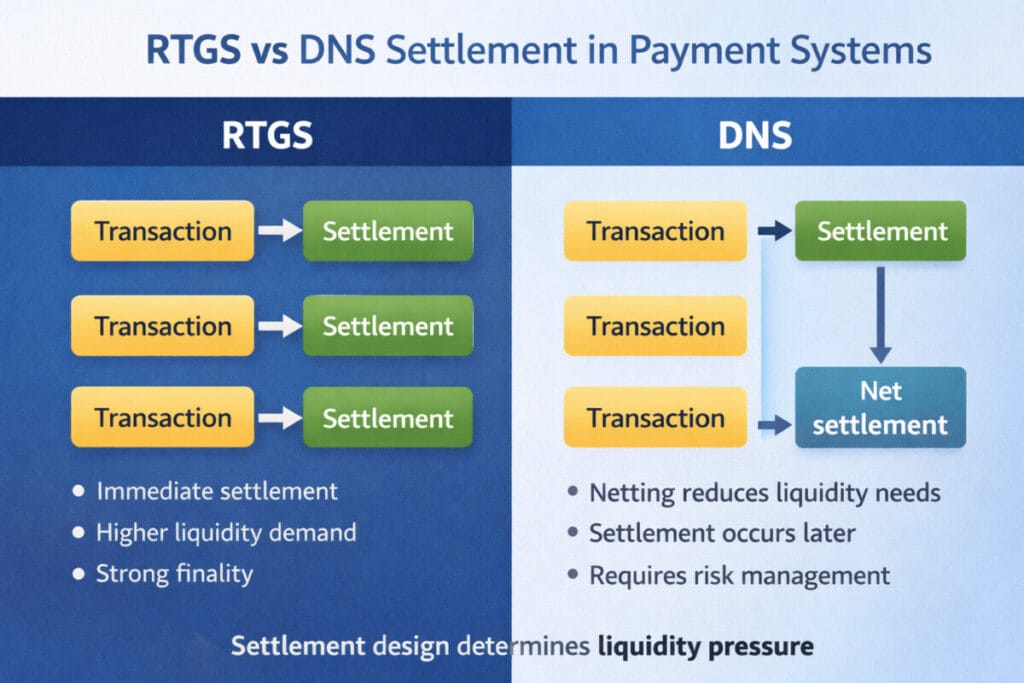

Some systems lean toward real-time gross settlement logic, where transactions are settled individually and quickly. Others rely more on deferred net settlement, where payment obligations are offset and settled later on a net basis. Both models can support fast user experiences, but they create very different liquidity consequences for banks. The BIS has explicitly noted that fast payments can be built with different settlement arrangements, including deferred settlement approaches.

| Settlement model | How it works | Liquidity impact | Main trade-off |

|---|---|---|---|

| Real-time gross style | Payments are settled transaction by transaction | Higher liquidity demand | Strong immediacy and finality |

| Deferred net settlement | Payments are offset and settled later on a net basis | Lower liquidity demand | More focus on risk controls before final settlement |

| 24/7 instant environment | Customers can send funds any time | Liquidity must be available outside normal funding windows | Time mismatch becomes the core challenge |

This is why faster payments do not automatically mean cheaper or easier payments for banks. Real-time settlement can reduce certain risks and strengthen finality, but it also forces participants to keep more funds ready. Deferred net settlement can save liquidity, but it shifts attention toward risk controls, settlement timing, and exposure management. The customer sees the same “money arrived instantly” message either way. The bank sees two very different liquidity problems.

TIPS shows the problem in the clearest way

Europe offers one of the best real-world examples. The ECB’s TIPS platform settles instant payments in central bank money on a 24/7/365 basis. It is built precisely to support round-the-clock instant payments with final and irrevocable settlement. That sounds like the ideal future of payments. And for users, in many ways, it is.

But the liquidity detail is where the real tension appears. According to ECB documentation, TIPS operates continuously, yet inbound and outbound liquidity transfers between TIPS and the RTGS environment can take place only during T2 operating hours. In plain English, the settlement engine never sleeps, but some of the key liquidity channels still follow opening hours.

That means banks must prepare in advance. If they expect payment activity while the broader RTGS window is closed, they need to prefund. In other words, they have to park liquidity ahead of time so instant payments can keep flowing overnight, on weekends, and during holidays. This is not just an operational detail. It changes the economics of instant payments.

The more liquidity a bank sets aside, the safer and smoother its instant payment performance becomes. But that money is then tied up. It cannot be used as flexibly elsewhere. If the bank sets aside too little, it risks disruption or defensive limits. If it sets aside too much, it hurts efficiency. This is exactly why 24/7 instant payments create a new liquidity problem: they turn time into a balance sheet issue.

Instant payments are becoming a treasury story

This is why instant payments are no longer just a payment product story. They are increasingly a treasury and liquidity architecture story.

A bank that wants to compete well in instant payments now needs more than a polished app. It needs stronger intraday and overnight liquidity forecasting. It needs better limit management. It needs smarter rules for prefunding. It may need stronger connectivity to central bank accounts or joint-account structures. It may also need automated tools that move liquidity before small operational issues become payment failures. FedNow’s liquidity transfer functionality reflects exactly this reality.

That shift matters for strategy. In the early stage of faster payments, the visible competition was about speed and customer experience. In the next stage, the real competition is about who can sustain that experience with the least trapped liquidity and the fewest operational bottlenecks. The winning banks may not be the ones with the flashiest payment journey. They may be the ones with the best liquidity design.

Why this matters even more from an SEO and market perspective

Search interest around instant payments often focuses on customer benefits: speed, convenience, real-time payroll, lower friction, and 24/7 availability. But the more valuable long-tail conversation sits underneath that surface. Questions like instant payments liquidity management, 24/7 bank liquidity, RTGS vs DNS for instant payments, and prefunding risk in instant payment systems point to a topic that is narrower, less crowded, and much more useful for decision-makers.

That is also why this issue is worth writing about now. Instant payments are no longer a niche infrastructure. The BIS has highlighted their global spread and the growing importance of 24/7 availability of funds, while the ECB and the Federal Reserve have both made liquidity management features central to how real-world instant payment infrastructure works. This is not theoretical. It is already shaping how payment systems are built.

The real takeaway

The future of payments is clearly faster. But faster does not mean simpler.

A 24/7 instant payment promise sounds like a front-end innovation. In practice, it is a back-end liquidity commitment. Banks are no longer just offering customers a better transfer experience. They are offering to stand ready with funds at all times, even when traditional funding windows are narrower than customer demand.

That is why 24/7 instant payments create a new liquidity problem for banks. The payment moves instantly. Liquidity often does not. And the more the industry pushes toward always-on settlement, the more that gap becomes the real battleground in modern banking.

References and Further Reading

- European Central Bank – TARGET Instant Payment Settlement (TIPS)

https://www.ecb.europa.eu/paym/target/tips/html/index.en.html - Bank for International Settlements – Real-Time Gross Settlement Systems

https://www.bis.org/cpmi/publ/d22.htm - Federal Reserve – FedNow Instant Payment Service

https://www.frbservices.org/financial-services/fednow - European Payments Council – SEPA Instant Credit Transfer Scheme

https://www.europeanpaymentscouncil.eu/what-we-do/sepa-instant-credit-transfer