Why fintech authentication suddenly feels more important

A few years ago, many users still thought authentication meant one thing: a password.

That world is fading fast.

Fintech apps now sit close to money, identity, account recovery, device trust, and high-risk actions like transfers or credential changes. That means login is no longer a small technical detail. It is one of the first places where trust is either confirmed or broken. NIST’s latest digital identity guidance still treats authentication as a core control area, and CISA continues to push phishing-resistant MFA because compromised credentials remain one of the most common entry points for attackers.

That is why terms like MFA, passkeys, and biometric authentication in fintech are showing up everywhere in fintech.

They are related, but they are not the same thing.

And a lot of confusion starts right there.

What MFA actually means

MFA stands for multi-factor authentication.

It means a user must prove identity using more than one category of evidence. In simple terms, authentication factors usually fall into three buckets:

- something you know

- something you have

- something you are

A password is something you know.

A phone, hardware key, or secure device-based authenticator is something you have.

A fingerprint or face scan is something you are.

CISA defines MFA as requiring an additional verification(Finteconomix : identity verification in fintech) method beyond a username and password, and recommends stronger forms of MFA because basic methods like SMS codes can still be targeted by phishing and account compromise.

In fintech, MFA matters because a single password is usually not enough protection for an account that can move money.

Why MFA is helpful but not always equally strong

This is where many people get misled.

Not all MFA is equally secure.

A password plus a one-time code sent by text message is still MFA. But it is not the same as a phishing-resistant method tied to a secure authenticator on a trusted device. CISA’s guidance makes this distinction clearly and specifically recommends phishing-resistant MFA where possible.

That matters in fintech because attackers do not only guess passwords anymore. They phish users, intercept codes, manipulate recovery flows, and trick people into approving prompts they do not understand.

So the real question is not just “Do we have MFA?”

It is “What kind of MFA are we actually using?”

What passkeys are and why people care so much

A passkey is a modern authentication method built on public key cryptography and commonly associated with FIDO-based passwordless authentication.

That sounds technical, but the user experience is much simpler than the jargon.

Instead of memorizing a password, the user signs in with a device-based credential, often unlocked through a fingerprint, face scan, or device PIN. The secret is not shared with the service in the same way passwords are. That is one of the big reasons passkeys are widely described as more resistant to phishing than traditional password flows. NIST has also issued guidance around syncable authenticators, including passkeys, as the technology becomes more important in real-world deployments.

This is why passkeys matter in fintech.

They do not just make login feel easier.

They can also reduce the kinds of password theft that create trouble later.

What biometric authentication actually is

Biometric authentication uses a person’s physical or behavioral characteristics to help confirm identity.

Common examples include:

- fingerprint

- face recognition

- iris recognition

- voice

- behavioral signals in some systems

In fintech, the most familiar forms are fingerprint and face unlock on a mobile device.

But here is the important part: biometrics are not a magic standalone answer.

NIST’s current guidance is very clear that biometrics should only be used in a limited way for authentication and must be combined with a physical authenticator. It also says a non-biometric alternative must be available. In other words, biometrics are usually part of a broader authentication design, not a complete replacement for everything else.

That is why it is more accurate to say:

Biometrics often unlock or activate a secure authenticator.

They do not automatically solve authentication by themselves.

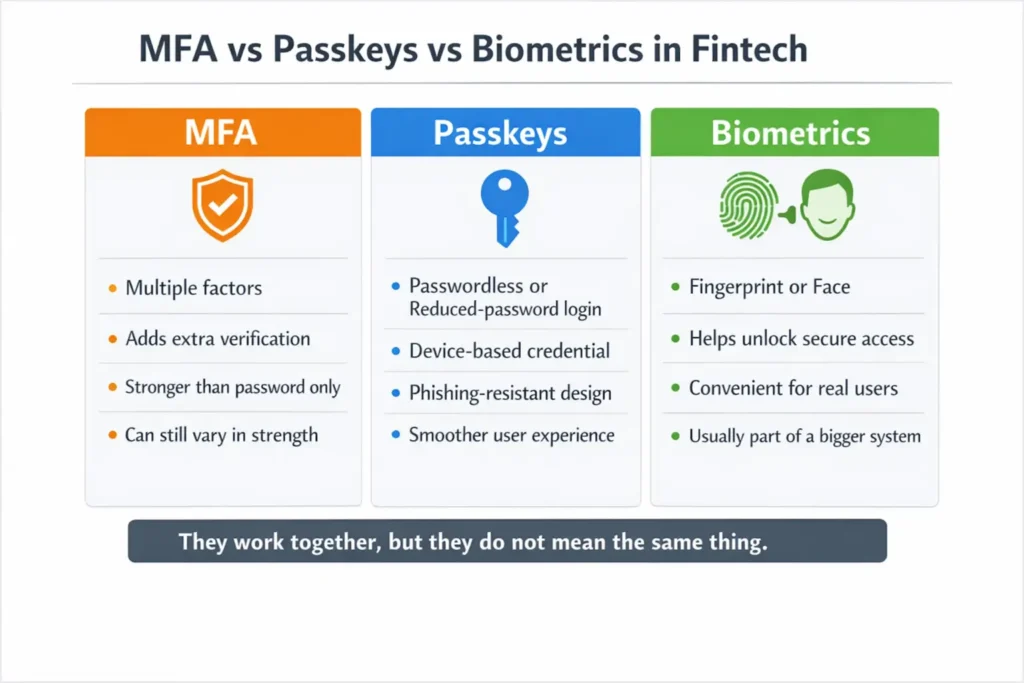

MFA, passkeys, and biometrics are not the same thing

This is the point that clears up most confusion.

| Term | What it means | Main role |

|---|---|---|

| MFA | Using more than one authentication factor | strengthens account access |

| Passkeys | Passwordless or reduced-password authentication based on public key cryptography | improves usability and phishing resistance |

| Biometric authentication | Using fingerprint, face, or similar traits as part of authentication | makes secure access easier for the real user |

A biometric login can be part of MFA.

A passkey can be used with biometrics.

But none of these terms means exactly the same thing.

That distinction matters in fintech because product teams, fraud teams, and users often talk past each other when they use one label for three different ideas.

Why passkeys fit fintech especially well

Fintech products live in a difficult balance.

They need:

- low friction

- strong account security

- high user trust

- fewer account takeover opportunities

- better conversion during login and sensitive actions

Passwords work badly with that combination.

People forget them. Reuse them. Enter them into phishing pages. Store them badly. Reset them through weak recovery paths. That is exactly why passkeys are so attractive. FIDO materials consistently frame modern passwordless authentication as stronger than shared-secret approaches like passwords and OTP-based flows because it relies on public key cryptography and device-based authenticators.

For fintech, that means passkeys are not just a design trend.

They are becoming a practical answer to a very old problem: how to make strong authentication feel less painful.

Why biometrics feel easy but still need care

Users love biometrics because they feel fast.

Touch the screen. Look at the phone. Open the app.

That simplicity is powerful in fintech, especially on mobile. It reduces login friction and can help keep legitimate users inside the flow instead of pushing them into password resets or support tickets.

But biometric authentication still needs careful design.

There are important questions behind the scenes:

- Is the biometric match happening securely on the device?

- Is the biometric only unlocking a trusted authenticator?

- What happens if the biometric cannot be used?

- How does recovery work if the user changes device?

- How does the system avoid false trust from a weak fallback path?

This is exactly why biometric authentication should be understood as a convenience and security layer inside a broader authentication system, not as a standalone miracle.

Why fintech companies increasingly care about phishing resistance

The phrase phishing-resistant authentication sounds technical, but the idea is straightforward.

A good authentication method should not be easy to replay, steal, or trick out of the user through a fake website or fake prompt.

That is why CISA emphasizes phishing-resistant MFA, and why passkeys are getting so much attention. They are designed to reduce the weakness of password-based systems that depend too heavily on shared secrets and user vigilance alone.

For fintech, that is a big deal.

Because once an attacker gets through login, the problem is no longer just “bad authentication.” It becomes account takeover risk, fraud risk, and customer trust risk very quickly.

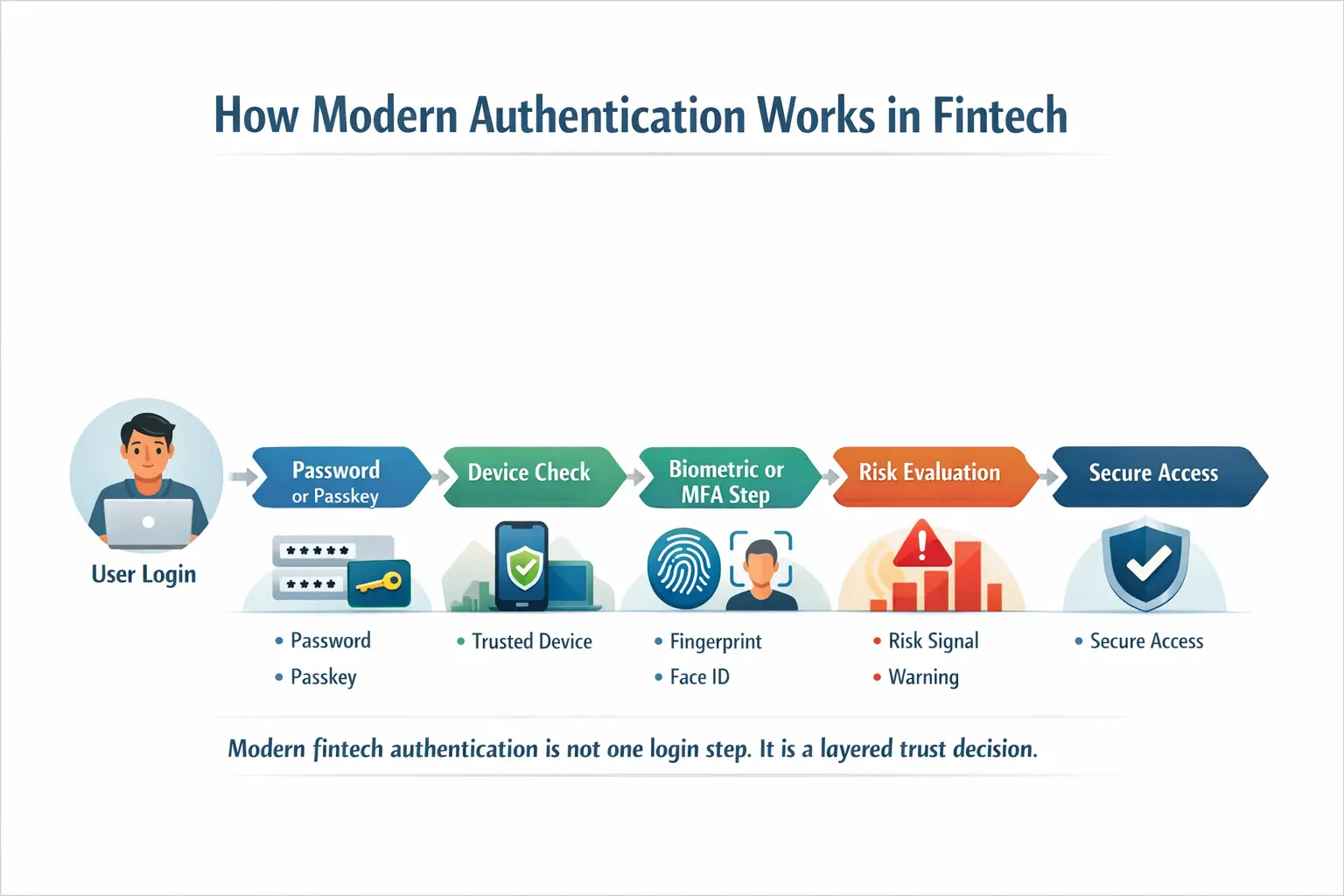

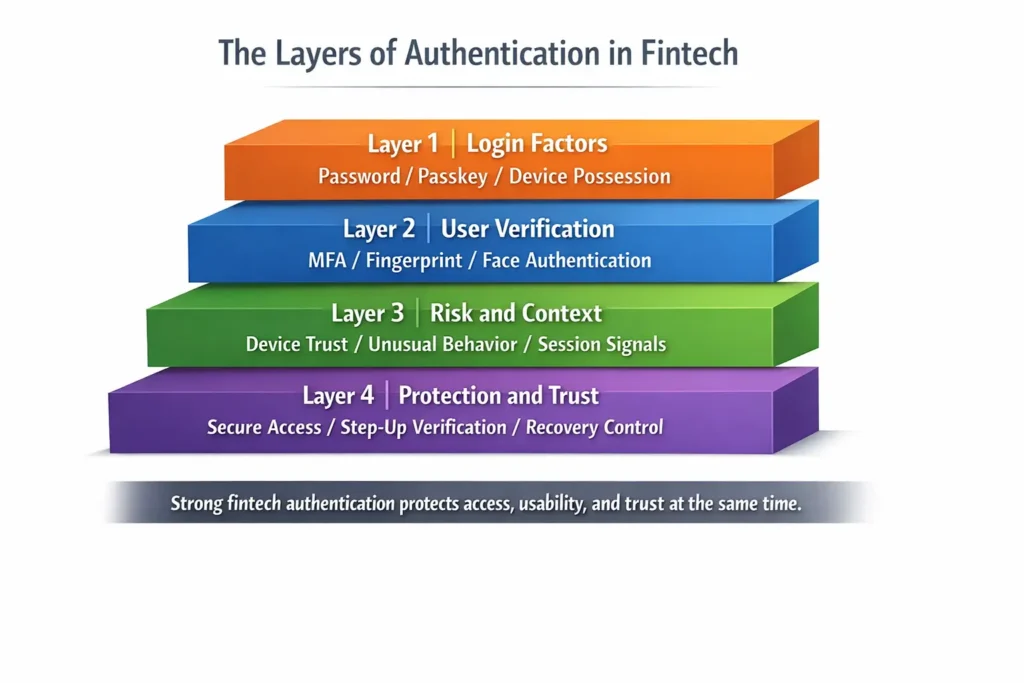

What good authentication in fintech usually looks like

The strongest fintech authentication models do not rely on one control.

They layer trust across:

- device

- credential

- biometric unlock

- session behavior

- recovery controls

- step-up verification for risky actions

That means a user may sign in smoothly with a passkey and device biometric for normal access, but still face an extra step when changing contact details, linking a new bank account, or moving a large amount of money.

That is not overkill.

That is good risk design.

Authentication should feel lighter when risk is low and stricter when risk rises.

Why recovery still matters even in a passkey world

A lot of authentication discussions focus too much on login and not enough on recovery.

That is dangerous.

A fintech app can build a modern sign-in flow and still get exposed if recovery is weak. If a fraudster cannot break the front door, they may try the side door instead through email change, device migration, phone number takeover, or support-assisted recovery.

NIST continues to emphasize authenticator lifecycle and recovery because strong authentication can be quietly weakened by weak fallback processes.

So even if passkeys and biometrics improve the front end of authentication, fintech still has to protect the recovery path with the same seriousness.

The real takeaway

MFA, passkeys, and biometric authentication all matter in fintech, but they solve different parts of the same trust problem.

MFA raises the security bar.

Passkeys reduce dependence on passwords and improve phishing resistance.

Biometrics make secure access more usable for real people.

That is why the future of fintech authentication is not just “add one more login feature.”

It is about building an authentication model that is:

- strong enough to resist modern attacks

- smooth enough for normal users

- flexible enough for mobile finance

- careful enough to protect recovery and high-risk actions

In fintech, authentication is no longer just a login choice.

It is part of the product, part of the fraud strategy, and part of the trust model.

References

NIST Digital Identity Guidelines

NIST SP 800-63B-4, Authentication and Authenticator Management