Why account takeover fraud feels so dangerous

Some types of fraud begin with a fake identity.

Account takeover fraud begins with a real one.

That is what makes it so unsettling. The account already exists. The customer is legitimate. The onboarding may have been clean. The device history may look normal for months. Then one day, a fraudster gets access and starts acting like the real user.

In fintech, that can turn into damage very quickly. A compromised account can be used to change credentials, link new devices, move funds, cash out balances, or abuse trust that the platform has already built with the legitimate customer. FinCEN explicitly treats account takeover as a reportable suspicious activity category and notes that it often involves unauthorized access to PINs, account numbers, and other identifying information.

What account takeover fraud actually means

Account takeover fraud, often shortened to ATO fraud, happens when a criminal gains unauthorized access to a real customer account and uses that access for fraudulent purposes.

That access may be used to:

- move money

- change contact details

- reset credentials

- add a new device

- link external accounts

- make purchases or transfers

- lock the real user out

In simple terms, account takeover fraud is what happens when a fraudster does not create a fake account from scratch. They hijack a trusted account that already has history, permissions, and user legitimacy. (Finteconomix – Fraud prevention in Fintech)

How account takeover usually happens

Account takeover rarely begins with one dramatic hack.

It usually starts with a chain of smaller weaknesses.

A customer clicks a phishing message. A reused password is exposed in another breach. A one-time code is shared with the wrong person. A SIM swap breaks phone-based verification. A device looks familiar enough to avoid an instant block. A fraudster gets inside quietly, then moves fast.

That is why account takeover is not just a login problem. It is a full trust problem across credentials, authentication, recovery flows, devices, and transaction behavior.

Common paths include:

- stolen usernames and passwords

- credential stuffing with reused passwords

- phishing and social engineering

- SIM swap or phone number takeover

- weak account recovery flows

- malware or session theft

- support-channel manipulation

Why account takeover is such a big fintech problem

Fintech platforms are especially exposed because they combine speed, digital onboarding, mobile usage, and direct access to financial actions.

A user may be able to sign in, verify, transfer funds, link accounts, and update settings in minutes. That convenience is part of what makes fintech attractive. It also means that once an account is compromised, the window for damage can be short.

This is one reason digital identity guidance puts so much emphasis on authentication strength, authenticator management, and account recovery. NIST’s current SP 800-63-4 framework specifically treats authentication and account recovery as core control areas in digital identity systems.

Why account takeover is different from identity fraud at onboarding

It is easy to confuse these two.

They are related, but they are not the same.

| Fraud type | What happens | Main weakness |

|---|---|---|

| Identity fraud | A fake or stolen identity is used to open an account | onboarding and verification |

| Account takeover fraud | A real customer account is hijacked after it already exists | login, recovery, or session trust |

That difference matters because a company can have strong onboarding and still struggle with account takeover later.

A clean KYC process does not eliminate ATO risk. It only means the platform started with a real customer. The problem comes later, when the wrong person gains control of that real customer relationship.

The warning signs fintech companies usually watch

Account takeover fraud often shows up as a mismatch between the account’s history and its current behavior.

A fintech company may look for signals like:

- login from a new or unusual device

- sudden location change

- password reset followed by money movement

- change in phone number or email right before a transfer

- new payee or linked account added quickly

- failed login attempts followed by a successful one

- activity at an unusual time or in an unusual sequence

One of these signals alone may not be enough.

Several together can tell a very different story.

That is why good ATO detection is not only about whether a password was correct. It is about whether the full pattern still makes sense for that specific user.

Why recovery flows can be as risky as login flows

A lot of people think the biggest risk is password theft.

Sometimes the bigger risk is account recovery.

If a fraudster cannot log in directly, they may try to reset the account instead. They may target password reset, email change, phone number change, customer support verification, or any fallback path that gives them a second route into the account.

NIST’s current guidance gives specific attention to account recovery because recovery is often where strong authentication is quietly weakened. A company can build a decent login experience and still leave a dangerous back door in the recovery process.

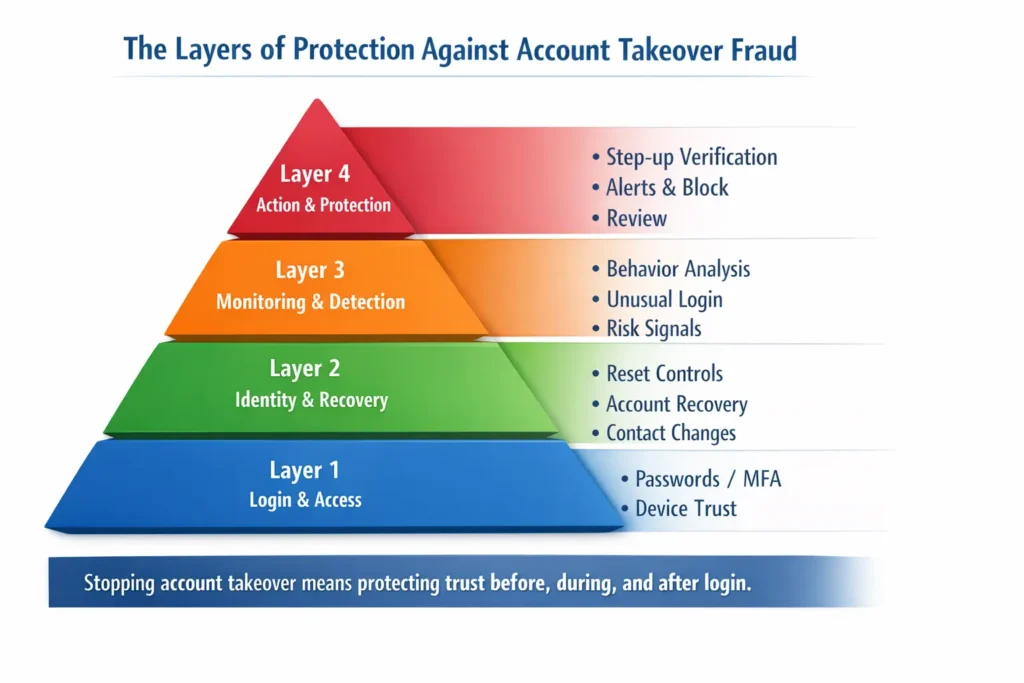

How fintech companies reduce account takeover risk

The best defenses do not rely on one control.

They layer trust.

That usually means:

- stronger authentication for sensitive actions

- device recognition and device trust checks

- risk-based step-up verification

- tighter controls on password resets and recovery

- alerts for account changes and unusual activity

- behavioral monitoring after login, not only before

- session controls and token protection

- delay, review, or challenge for high-risk actions

This is important because account takeover is often not detected at the login screen alone. Sometimes the login succeeds, but the behavior after login starts to look wrong.

That is why the strongest fintech fraud systems keep evaluating trust during the session, not just at entry.

Why customer education still matters

Technology helps a lot, but customers still sit inside the risk picture.

A user who shares a one-time code with a fake bank caller can unintentionally help the takeover happen. A user who reuses passwords across services can make credential theft much easier. A user who ignores account alerts may not notice a compromise until the money has already moved.

FTC guidance on identity theft consistently emphasizes practical defensive steps like watching for misuse, protecting credentials, and acting quickly when identity information is abused.

That means good fintech security is not only about building internal controls. It is also about helping customers avoid being manipulated in the first place.

The real goal is not to add friction everywhere

This is where product teams and fraud teams often collide.

If a company adds too little friction, account takeover becomes easier.

If it adds too much friction, real users get annoyed, blocked, or driven away.

The real goal is not maximum friction. It is intelligent friction.

Low-risk activity should feel smooth.

High-risk activity should feel harder.

Very high-risk activity may need to stop completely.

That balance is one of the hardest things to get right in fintech. But it is also one of the most important. The safest product is not the one that blocks everyone. It is the one that protects real users without treating every user like a criminal.

The real takeaway

Account takeover fraud in fintech matters because it attacks trust after trust has already been built.

That is why it feels so dangerous.

The account is real. The user is real. The relationship is real. What changes is control.

Once a fraudster gets that control, the platform may still look normal on the surface while the risk underneath is already rising.

That is why reducing account takeover fraud is not just about passwords or MFA in isolation. It is about protecting the full chain of trust across login, recovery, device signals, behavior, and high-risk actions.

In fintech, account takeover is not just an access problem.

It is a live test of whether digital trust can hold under pressure.

References

NIST, Digital Identity Guidelines (SP 800-63-4)

NIST SP 800-63B-4, Authentication and Authenticator Management