Why KYC matters far beyond compliance

KYC in Fintech sounds like one of those cold financial acronyms people skip over.

But in fintech, KYC is one of the first moments where a company proves whether it can grow safely.

A user downloads an app. They want to open an account in minutes, move money quickly, and get started without friction. The company wants that too. But before that happens, one hard question appears:

Who is this customer, really?

That is where KYC begins.

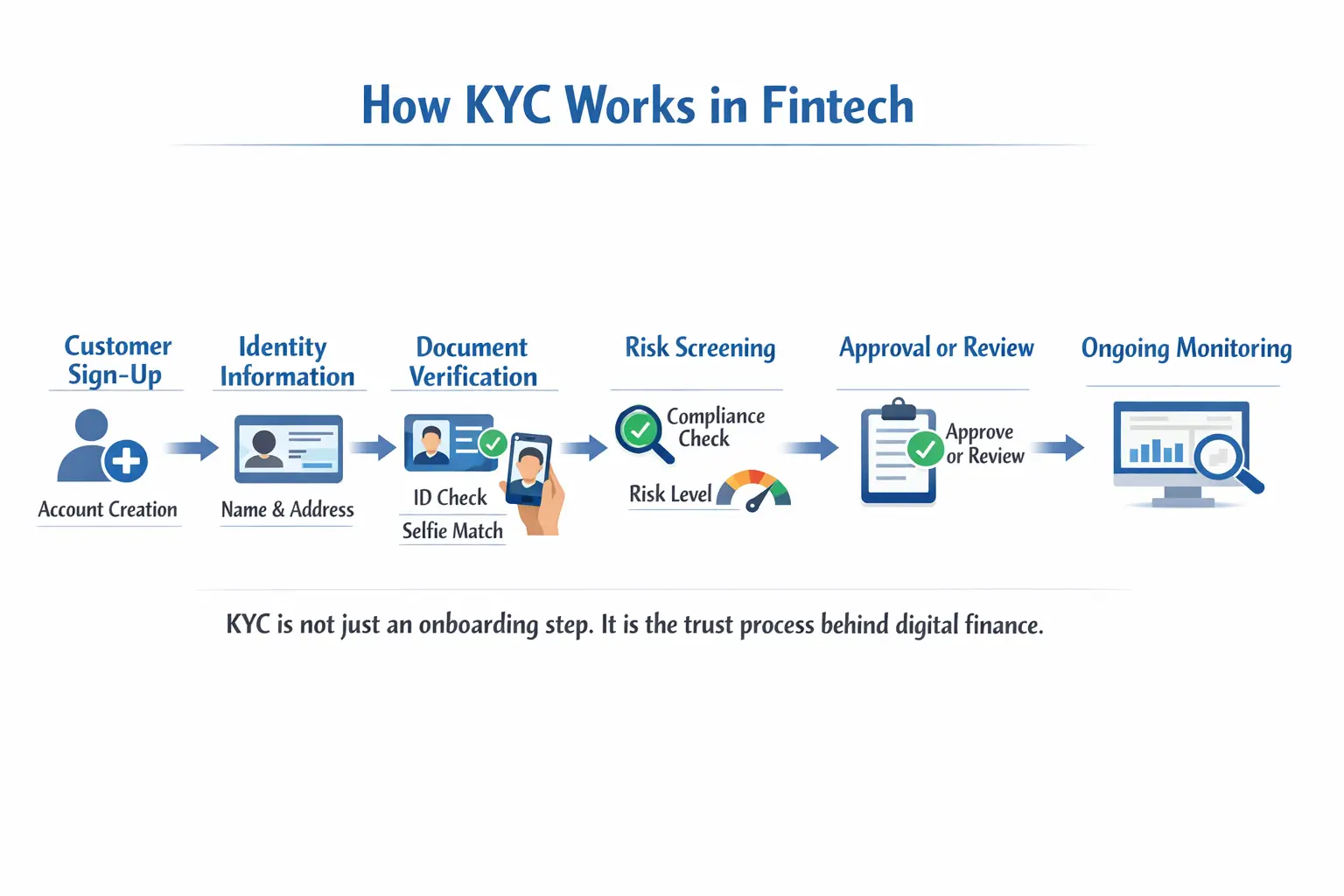

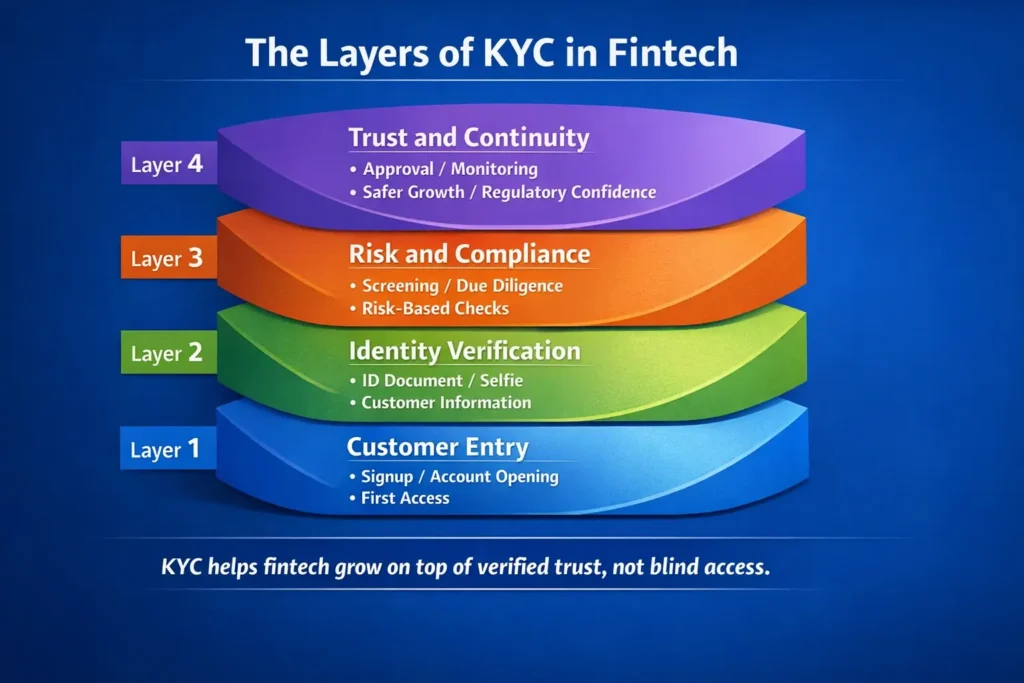

KYC, or Know Your Customer, is the process of identifying and verifying a customer before and during a financial relationship. In practice, that means checking whether the customer is real, whether the information makes sense, whether the relationship fits an expected purpose, and whether the risk level is acceptable. FATF’s global standards make that clear by requiring customer due diligence, beneficial owner checks where relevant, and ongoing monitoring based on risk. FinCEN’s CDD rule also frames customer due diligence as part of understanding the nature and purpose of customer relationships and maintaining ongoing monitoring.

What KYC in fintech actually means

In old finance, KYC often happened across a desk.

In fintech, it happens on a screen.

That changes everything.

Instead of handing documents to a branch employee, customers now upload IDs, take selfies, confirm phone numbers, connect data, and move through onboarding flows that may last only a few minutes. What feels simple on the surface is actually a layered trust process in the background.

KYC in fintech usually includes:

- identity collection

- document verification

- customer risk screening

- checks on business purpose or account use

- ongoing monitoring after onboarding

This is why KYC is not the same thing as “upload your ID and move on.” It is a broader judgment about whether a fintech can safely start and maintain a financial relationship.

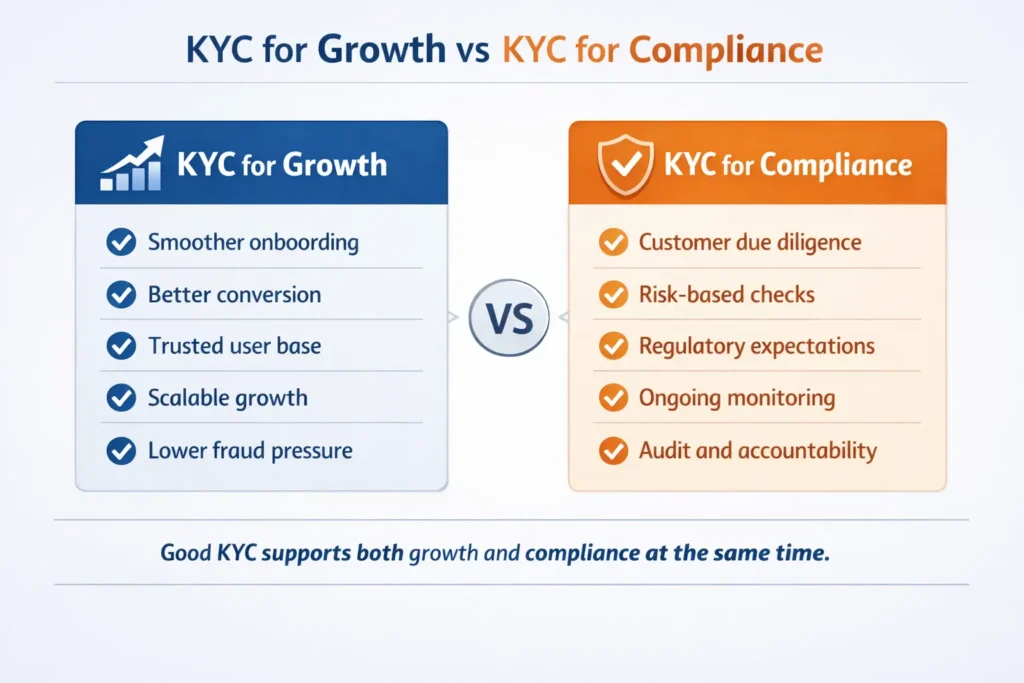

KYC is one of the first growth filters in fintech

A lot of people think KYC only slows growth down.

That is the wrong way to look at it.

Bad KYC slows good growth down.

Good KYC protects scalable growth.

A fintech that approves the wrong users too easily may grow fast at first, but it also opens the door to fraud, fake accounts, mule activity, sanctions exposure, and support costs. A fintech that makes onboarding too painful may lose legitimate users before they ever experience the product.

That is why the best fintech companies do not treat KYC as a box-ticking exercise. They treat it as a growth filter.

The real goal is not “verify everyone the hardest way possible.”

The real goal is “verify the right customers with the right level of confidence and the right level of friction.”

That balance matters because onboarding is often where conversion and risk meet for the first time.

Why KYC is so important for compliance

KYC is also one of the clearest places where fintech meets regulation.

Financial firms are expected to understand who their customers are, assess risk appropriately, and monitor activity over time rather than only at sign-up. FATF’s standards are explicitly risk-based, which means firms are not expected to treat every customer in exactly the same way, but they are expected to apply stronger measures where risk is higher. FATF’s 2025 financial inclusion guidance also emphasizes that well-designed, risk-based AML/CFT controls can support inclusion rather than simply create blanket friction.

That matters because fintech companies often want two things at the same time:

- faster onboarding

- broader customer reach

Regulators care about something else at the same time:

- safe onboarding

- appropriate due diligence

- ongoing monitoring

- accountability when risks appear

KYC sits right in the middle of those goals.

Why KYC matters for user trust too

Here is the part that is easy to miss.

Customers do not usually log into a fintech app thinking, “I hope this company has a strong customer due diligence framework.”

But they absolutely care about the results.

They care that fake users do not flood the platform.

They care that stolen identities do not get approved too easily.

They care that the app feels safe enough to link a bank account, store money, or receive payments.

So KYC is not just about satisfying regulators. It is also about creating a product people trust.

In digital finance, trust is often invisible until it breaks.

KYC helps stop that break from happening too early.

Why digital KYC can also support financial inclusion

KYC is often described like a barrier, but it can also become an access tool when it is designed well.

The World Bank has pointed out that digital ID systems can improve the reliability, security(Finteconomix – fintech security), privacy, and efficiency of identifying individuals, and that digital financial inclusion depends on reaching underserved users in responsible and affordable ways. In simple terms, better digital identification can help more real people enter formal finance without relying on old branch-heavy models.

That matters in fintech because the right onboarding model can do two things at once:

- reduce unnecessary friction for legitimate users

- keep risk controls strong enough to block abuse

This is one of the most important shifts in modern finance. KYC no longer has to mean slow paper-based exclusion. In the best cases, it becomes part of smarter, faster, more accessible onboarding.

What weak KYC looks like in practice

Weak KYC does not always look like a dramatic failure.

Sometimes it looks like:

- too many accounts approved with weak checks

- fraud showing up months after onboarding

- support teams overwhelmed by suspicious cases

- compliance teams constantly cleaning up bad entry decisions

- partners and banks losing confidence in the platform

The damage is rarely limited to one team.

Weak KYC creates pressure across fraud operations, customer support, platform trust, compliance reviews, and even growth strategy.

That is why customer verification is not just a legal requirement. It is operational infrastructure.

What strong KYC looks like in fintech

Strong KYC in fintech usually has a few clear qualities.

It is:

- fast for legitimate users

- harder to manipulate for bad actors

- risk-based instead of blindly identical for everyone

- connected to fraud monitoring, not isolated from it

- reviewed and improved over time

That last point matters a lot.

KYC is not a one-time setup project. Fraud changes. regulations evolve. products expand. customer behavior shifts. A fintech that grows into lending, payments, wallets, cross-border transfers, or embedded finance may need a much more mature KYC design than it needed on day one.

The real takeaway

KYC in fintech matters because customer verification is not just a compliance step.

It is one of the first decisions a fintech makes about trust.

It shapes who gets through onboarding, how safely the platform can grow, how confidently regulators and partners view the business, and how secure the customer experience feels over time.

A fintech cannot scale well if it does not know who it is serving.

And it cannot build lasting trust if it treats customer verification like a paperwork chore.

In modern digital finance, KYC is not just about checking identity.

It is about building growth on top of verified trust.

References

World Bank, Digital ID to Enhance Financial Inclusion