From card swipes and direct deposit to wire transfers, RTP, and FedNow, here is how payment systems in us actually work

You buy a coffee on your way to class. Your paycheck lands on Friday. Your rent gets pulled automatically. A friend sends you money back for dinner. On the surface, it all feels like the same thing. Money goes in. Money goes out. Done.

But that is not what is really happening.

That is exactly why payment systems in us are more interesting than they sound. In the United States, money does not move through one giant all-purpose system. It moves through different rails built for different jobs. Some are made for everyday spending. Some are built for payroll and recurring payments. Some handle larger, more urgent transfers. And now there are newer rails trying to make money move fast enough to match the rest of digital life.

Once you notice that, payments stop looking boring. They start looking like the hidden operating system of modern life.

The U.S. does not have one payment lane

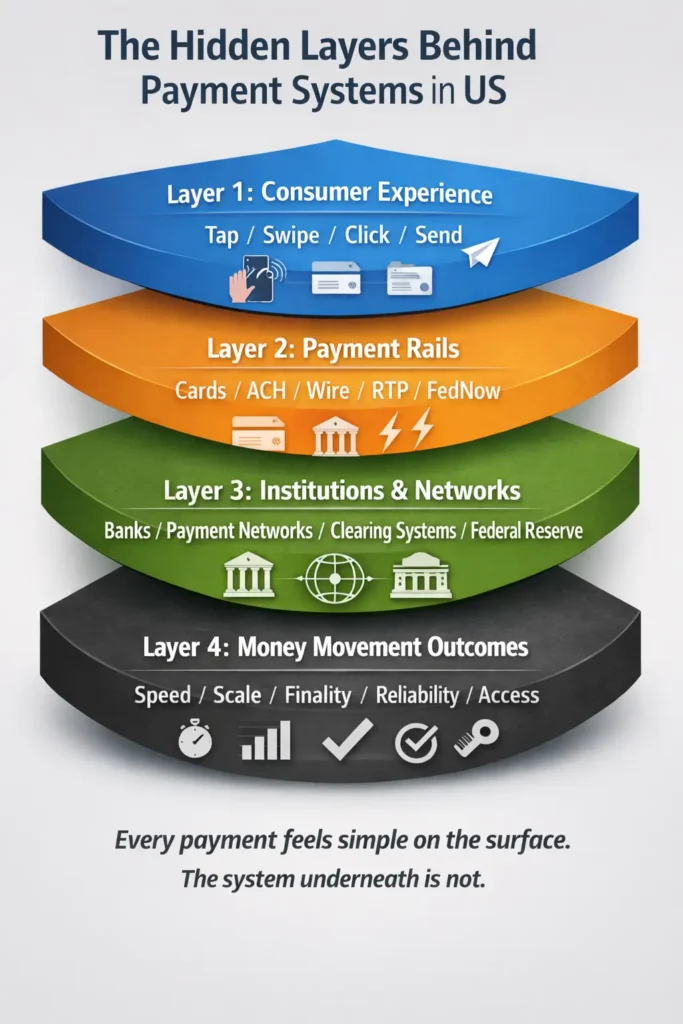

A lot of people imagine modern payments as one smooth digital flow. Tap a card, hit send, move on. But that is not really how payment systems in us work.

A better way to picture it is like a city with different train lines. One line is crowded with everyday traffic. One moves heavy stuff quietly in the background. One is for urgent trips. One is newer, faster, and trying to change expectations.

That is why two payments can feel almost identical on your phone but behave completely differently behind the scenes. One might clear quickly. Another might take longer. One might be easy to reverse. Another might feel much more final. The front end looks simple because it is designed to look simple. The back end is doing a lot more work than most people realize.

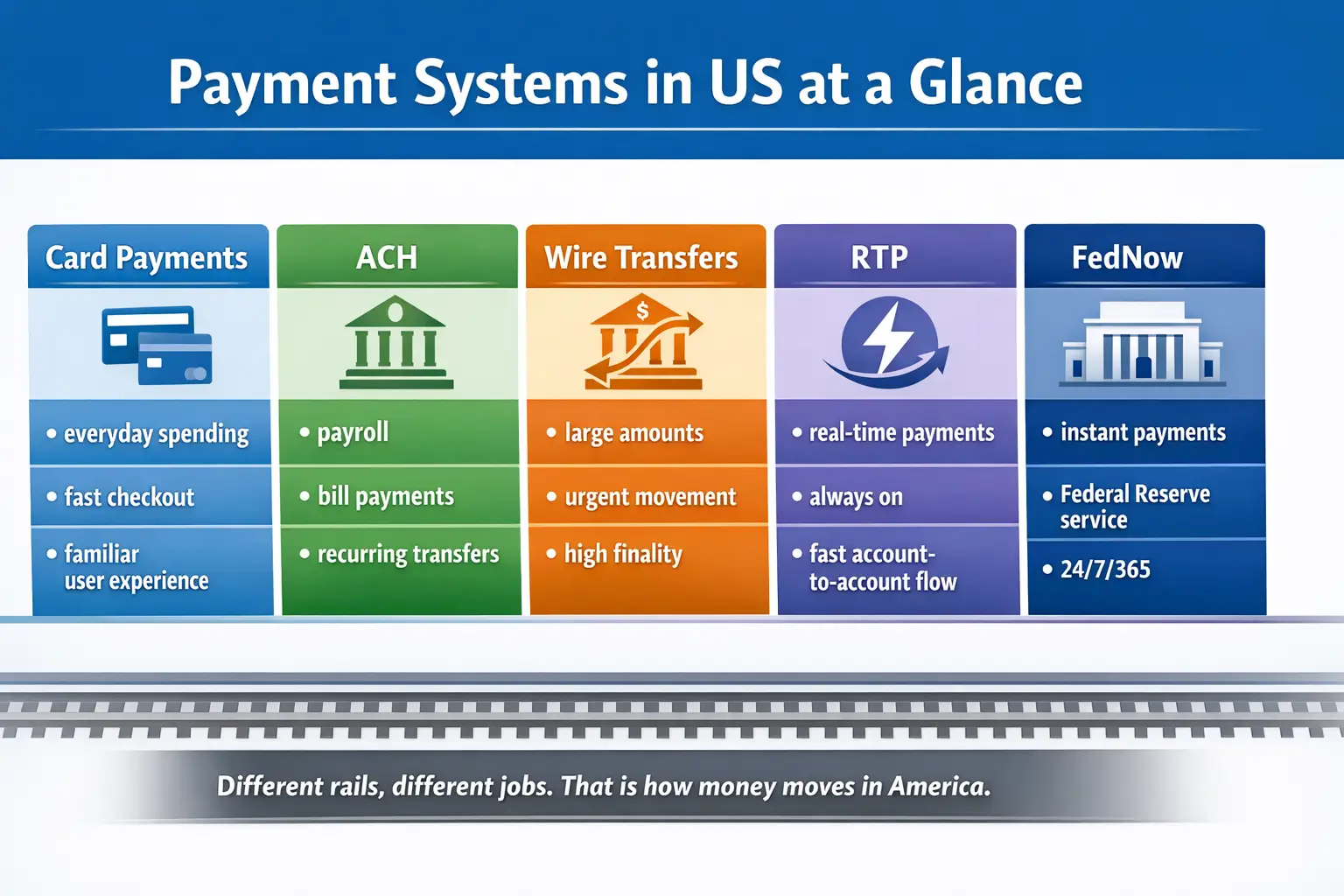

Card payments run daily life

If there is a main character in payment systems in us, it is probably card payments.

Cards are everywhere in America. Grocery stores, online shopping, streaming subscriptions, ride-sharing apps, food delivery, travel bookings, random late-night purchases that somehow felt necessary at the time. They fit daily life because they are easy. Tap, swipe, click, done.

That convenience is why cards are such a huge part of the U.S. payment experience. They feel instant, clean, and familiar. But the money is not simply teleporting from one place to another. There is a whole process under the surface involving authorization, network messaging, clearing, and settlement.

That is one of the most important things to understand about payment systems in us. The payment experience that feels the most effortless is often sitting on top of one of the most structured systems.

ACH is the quiet giant

ACH is not flashy, but it is one of the biggest reasons the system works.

A huge amount of normal financial life runs through ACH. Paychecks. Direct deposits. Bill payments. Subscription renewals. Bank-to-bank transfers. Recurring payments that people barely think about. ACH is the rail behind a lot of that routine money movement.

If card payments are the part everyone sees, ACH is the part carrying a huge amount of weight without demanding attention. It is built for repetition, reliability, and scale. That makes it perfect for the boring but essential stuff that keeps everyday finance moving.

And honestly, that is what makes it interesting. payment systems in us are not only about fast consumer checkout moments. They are also about the invisible systems that keep money moving when nobody is paying attention.

Wire transfers are the serious lane

Then there is wire transfer, which has a completely different energy.

You do not usually think about a wire transfer when you are buying lunch or paying for a movie ticket. Wire transfers show up when the amount is large, the timing matters, and nobody wants errors. Big business payments, property-related transfers, high-value movements of money — this is where wire becomes relevant.

In the bigger picture of payment systems in us, wire transfers are the serious lane. They are used when speed and finality matter more than convenience or habit. That gives them a different reputation from cards and ACH.

If ACH feels like a reliable cargo route, wire feels like a direct express route with much less room for casual mistakes.

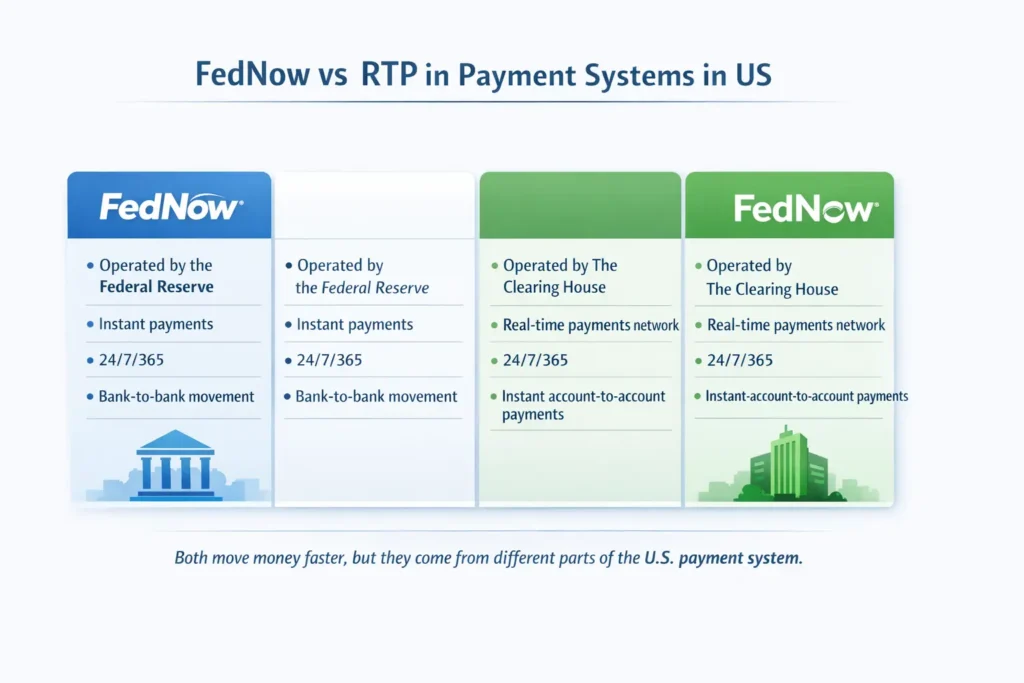

FedNow and RTP are changing expectations

This is where the story gets especially interesting.

For a long time, one of the biggest frustrations in payment systems in us was that digital life felt fast, but money did not always move that way. You could send a message instantly, stream video instantly, and order food in seconds, yet money itself could still feel like it was stuck in a slower era.

That is why real-time payments matter so much.

In the U.S., two names stand out here: RTP and FedNow. RTP is a real-time payments network. FedNow is the Federal Reserve’s instant payment service. Together, they represent something bigger than just new technology. They reflect a change in what people now expect money to do.

People do not just want digital payments. They want digital payments that feel immediate.

That is what makes FedNow such an important part of payment systems in us. It signals that the U.S. payment landscape is moving more seriously into real-time money movement. It does not replace cards. It does not replace ACH. It does not replace wire. But it adds a new layer to the system and pushes the whole conversation forward.

The same is true for RTP. The existence of real-time rails changes how people think. Once users know money can move within seconds, waiting starts to feel less normal. That changes product design, user expectations, and the way payment innovation gets discussed.

Why the U.S. keeps multiple rails

At first glance, the whole setup can look messy. Why not just replace everything with one perfect system?

Because different payments need different things.

Buying lunch is not the same as receiving payroll. Sending a friend money is not the same as closing on a home. A subscription renewal is not the same as a high-value corporate transfer. Cost, timing, scale, convenience, certainty, and speed do not matter in the same way for every payment.

That is why payment systems in us stay layered. The system reflects real life, and real life is not one use case. It is a collection of very different payment moments that happen to use the same word: payment.

So instead of building one rail that tries to do everything, the U.S. ended up with several rails doing different jobs.

Why this matters more than people think

Once you understand payment systems in us, a lot of things start making more sense.

A delayed transfer feels less random. Direct deposit feels less mysterious. Payment apps stop looking like magic and start looking like products built on top of specific rails. The difference between “payment confirmed” and “money fully settled” starts to click.

It also makes fintech stories easier to follow. A lot of what gets called innovation in finance is really about improving what happens on top of payment rails, between payment rails, or around them. Once you understand the rails, the whole industry starts looking much less confusing.

And that is what makes this topic worth reading. It is not just about banks. It is about how daily digital life is organized behind the scenes.

Final thoughts

The simplest way to understand payment systems in us is this: America does not run on one payment path. It runs on several.

Cards power everyday spending. ACH keeps routine and high-volume payments moving. Wire handles larger and more urgent situations. RTP and FedNow are pushing the system toward a faster future.

So the next time money shows up instantly, lands tomorrow, or arrives through direct deposit like clockwork, it is worth remembering that none of it happens by accident. Behind every tap, click, transfer, and autopay, there is a system choosing the rail that fits the job.

References

- Finteconomix – What is payment infrastructure and how does it work https://finteconomix.com/what-is-payment-infrastructure-and-how-does-it-work/

- Federal Reserve Board – Payment Systems

https://www.federalreserve.gov/paymentsystems.htm - Federal Reserve Board – Fedwire Funds Service

https://www.federalreserve.gov/paymentsystems/fedfunds_about.htm - The Clearing House – RTP

https://www.theclearinghouse.org/payment-systems/rtp

Read the Full Payment Systems Series

| Country / Region | Main Focus | Read More |

|---|---|---|

| United States | Cards, ACH, wire transfers, RTP, FedNow | Payment Systems in US |

| India | UPI, QR payments, NEFT, RTGS, RuPay | Payment Systems in India |

| Brazil | Pix, QR payments, cards, boleto | Payment Systems in Brazil |

| Europe | SEPA, instant payments, SCT Inst, TIPS | Payment Systems in Europe |

| Singapore | PayNow, FAST, SGQR, cross-border links | Payment Systems in Singapore |