Open finance, open banking, and why the difference matters

Open finance and open banking are closely related, but they are not interchangeable.

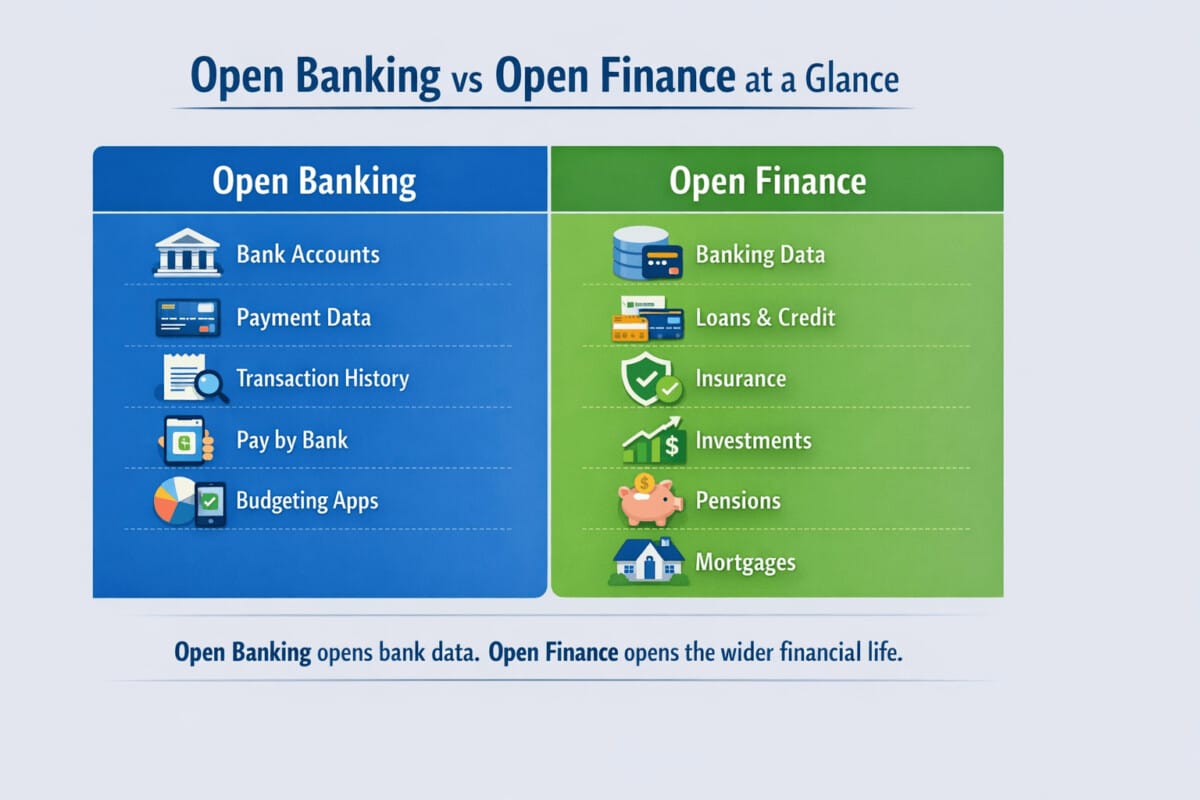

Open banking is the earlier and narrower model. It mainly focuses on allowing consumers and businesses to share certain bank account and payment data with approved third parties through secure, consent-based access. That is the framework behind services such as account aggregation, budgeting tools, and pay-by-bank experiences.

Open finance goes much further. It extends the same logic beyond bank accounts and payment data into a broader set of financial products and services. Depending on the market and regulatory framework, that can include savings, credit, insurance, investments, pensions, mortgages, and other financial data.

That is why the phrase open finance vs open banking matters so much. The difference is not just about terminology. It changes what consumers can do with their financial data, what fintech companies can build, and how competition develops across the financial sector.

What is open banking?

In simple terms, open banking allows a customer to authorize access to certain banking data so another provider can deliver a service on their behalf.

That service may be as simple as showing multiple bank accounts in one app. It may also involve analyzing transaction history, helping with budgeting, or enabling payments directly from a bank account instead of through a card network.

Open banking became important because it moved financial data away from a closed, institution-by-institution model. Instead of each bank keeping customer data locked inside its own interface, the customer could allow that data to be used elsewhere in a secure and structured way.

This created the foundation for many familiar fintech products:

- account aggregation apps

- personal finance dashboards

- cash flow analysis tools

- subscription tracking services

- pay-by-bank checkout options

In other words, open banking helped make banking data more portable and more useful.

What is open finance?

Open finance takes the same principle and applies it to a much wider part of a person’s financial life.

Instead of stopping with current accounts or payment accounts, open finance is designed to allow customer-permissioned sharing across a broader set of financial relationships. That means the conversation moves beyond just transactions and balances.

A fuller open finance environment may include:

- credit products and loan history

- insurance products and coverage details

- investments and portfolio data

- pensions and retirement information

- mortgage-related data

- other financial product information linked to the customer

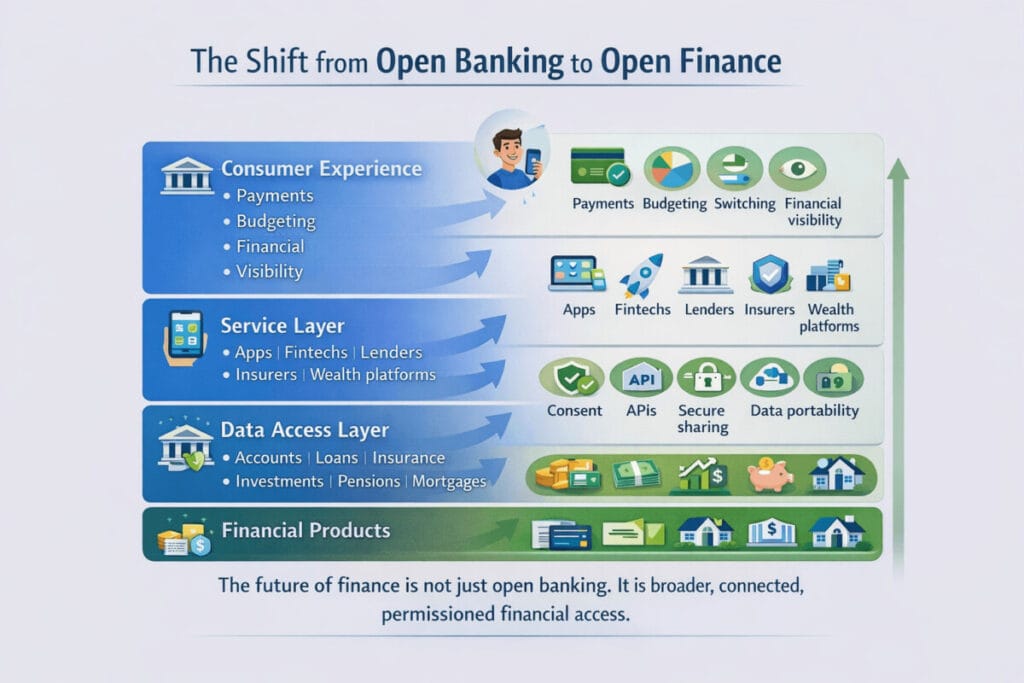

That is why open finance is often described as the next stage after open banking. Open banking connects the banking layer. Open finance aims to connect the wider financial layer.

Open finance vs open banking: a quick comparison

| Category | Open Banking | Open Finance |

|---|---|---|

| Main focus | Bank account and payment data | Broader financial data across multiple product categories |

| Typical products involved | Current accounts, balances, transaction data, payment initiation | Banking, savings, loans, credit, insurance, investments, pensions, mortgages |

| Main goal | Easier payments, data portability, better money management | Wider financial visibility, smarter comparison, more tailored financial services |

| Consumer value | Budgeting, account aggregation, pay-by-bank | Holistic financial management, richer recommendations, broader comparison |

| Fintech opportunity | Payments, personal finance apps, account-based services | Cross-product platforms, advisory tools, integrated financial experiences |

| Complexity level | Lower relative complexity | Higher technical, legal, and operational complexity |

The simplest way to understand the difference is this:

Open banking opens banking data.

Open finance opens financial data more broadly.

Why consumers should care about open finance vs open banking

For consumers, the shift from open banking to open finance can be very meaningful.

A person’s financial life is never limited to one checking account. Most people interact with multiple products at the same time. They may have a salary account, credit cards, loans, insurance policies, investment accounts, and retirement plans. Open banking helps with one part of that picture. Open finance aims to connect more of it.

That can change the consumer experience in several important ways.

Better comparison across financial products

In a narrow system, consumers often compare products one by one. A savings product is compared only with other savings products. An insurance product is compared only with other insurance products.

Open finance creates the possibility of better comparison because services can work with a wider financial context. Instead of asking, “Which product looks cheapest?” the question becomes, “Which product fits my broader financial situation best?”

That is a much more useful question.

More personalized recommendations

A basic budgeting app built on open banking data can tell you where your money goes each month. A broader open finance service could do much more.

It could highlight whether your insurance coverage appears weak, whether your debt mix is becoming expensive, whether your savings strategy is too conservative for your goals, or whether your long-term retirement position looks out of balance with your current income and spending.

That moves the conversation from basic data access to more meaningful financial guidance.

Easier switching and onboarding

Consumers often face friction when moving from one provider to another. They repeat forms, resend documents, and rebuild their financial profile again and again.

A stronger open finance framework could reduce that friction. With customer permission, information can move more easily between providers, making it simpler to apply for new services, compare offers, or switch to a better option without starting from zero each time.

A more complete view of financial life

This may be the biggest long-term benefit.

Many people still manage their finances through separate apps and separate institutions. Banking happens in one place. Insurance is viewed elsewhere. Investments sit in another dashboard. Retirement information may be hidden in yet another portal.

Open finance points toward a more unified model where consumers can see a fuller view of their financial position in one place, or at least across better-connected services.

Why fintech should care about open finance vs open banking

For fintech companies, the jump from open banking to open finance is not just an expansion in data. It is an expansion in business possibilities.

Open banking allowed fintech companies to build strong products around bank connectivity. That supported the growth of payment initiation, account dashboards, spending analysis, and cash flow tools.

Open finance expands the field.

From narrow tools to broader platforms

A fintech that once built a simple budgeting product could evolve into something much larger. Instead of helping users track spending only, it could help them understand debt structure, insurance gaps, investment allocation, and long-term financial planning.

That is a major business shift.

The winning fintech products in an open finance environment may be the ones that understand the customer’s overall financial life, not just one part of it.

Better underwriting and smarter decision support

When data moves beyond bank transactions, fintech providers gain more context.

A lender can potentially evaluate a borrower with more nuance. A wealth platform can better understand risk tolerance and long-term capacity. An insurance platform can deliver more relevant product recommendations. A financial dashboard can become more than a reporting tool and turn into a decision-making tool.

The advantage is not just more data. The advantage is better context.

Higher expectations around trust and consent

Open finance also raises the bar.

The more data a company wants to access, the more clearly it must explain why that access benefits the user. Consumers may accept bank account connectivity more easily than broader access across investments, insurance, pensions, and credit history.

That means fintech firms need stronger consent design, better privacy explanations, and a much clearer value proposition.

In open finance, trust is not a marketing add-on. It becomes a core product feature.

More opportunity, but also more complexity

Open finance is harder to build than open banking.

Different financial products use different data structures, standards, and legal rules. A pension is not the same as a brokerage account. A mortgage is not the same as an insurance contract. Expanding data access across these areas means more technical integration work, more governance challenges, and more questions about liability and responsibility.

So while the opportunity is larger, the execution challenge is also much larger.

The practical difference: from payments to financial life

The easiest way to think about open finance vs open banking is to look at the kind of questions each model is best suited to answer.

Open banking is strong when the questions are:

- How much did I spend this month?

- Can I view all my bank accounts together?

- Can I pay directly from my bank account?

- What are my recent cash flow patterns?

Open finance becomes more useful when the questions are:

- Is my total financial setup efficient?

- Am I paying too much across debt, insurance, and other products?

- Is my investment strategy aligned with my income and obligations?

- Which provider gives me the best overall product fit, not just the cheapest single product?

- How does my financial situation look when I connect banking, credit, savings, and long-term planning together?

That is the real transition.

Open banking improves access to banking services.

Open finance improves visibility into financial life.

Risks and concerns behind open finance

The broader the model becomes, the more important the risks become.

Privacy

Open finance can involve much more sensitive and much more revealing financial information than open banking alone. That means customers need clear explanations of what is being shared, who is using it, how long it will be retained, and how consent can be withdrawn.

Security

As the data universe expands, security expectations also rise. Consumers may hesitate to allow wider access unless they believe the system is safe, understandable, and properly governed.

Data quality and standardization

This is one of the hardest issues in open finance. Banking data already presents standardization challenges. Broader financial data is even more complex.

Different product categories have different formats, different meanings, and different operational structures. Making that information portable and useful across providers is not simple.

Liability and accountability

If something goes wrong, consumers need clarity. Who is responsible if data is inaccurate, misused, or exposed? As open finance expands, those questions become more important, not less.

Is open finance replacing open banking?

Not exactly.

A better way to say it is that open finance builds on open banking. Open banking remains important because it established the first practical model for permissioned financial data sharing. It created the early structure, the early standards, and the early consumer use cases.

Open finance takes that foundation and expands it.

So the question is not whether open banking disappears. The question is whether financial markets evolve from opening one part of the data landscape to opening much more of it in a structured, trustworthy way.

Final thoughts

The real story behind open finance vs open banking is the shift from product-specific access to broader financial connectivity.

Open banking changed how consumers and fintech companies use bank account and payment data.

Open finance has the potential to change how they understand and act on the entire financial relationship.

For consumers, that can mean:

- better comparison

- more personalized financial experiences

- easier switching

- a more complete view of money, debt, risk, and long-term planning

For fintech, that can mean:

- broader business models

- better product design

- richer decision support

- stronger competition based on intelligence, trust, and user value

The opportunity is significant, but so is the responsibility. The companies that succeed in open finance will not simply be the ones with the most integrations. They will be the ones that turn broader financial data access into something that feels genuinely useful, safe, and easy to trust.

References

- Finteconomix, What Is an Open Banking API? How Financial Data and Account-to-Account Payments Connect (Finteconomix)

- FCA, Research Note: Open Banking and Open Finance in the UK (FCA)

- European Commission, Framework for Financial Data Access (Finance)

- CFPB, Finalizes Personal Financial Data Rights Rule (Consumer Financial Protection Bureau)

- CFPB, Required Rulemaking on Personal Financial Data Rights (Consumer Financial Protection Bureau)