What to know before you send money to a US bank account

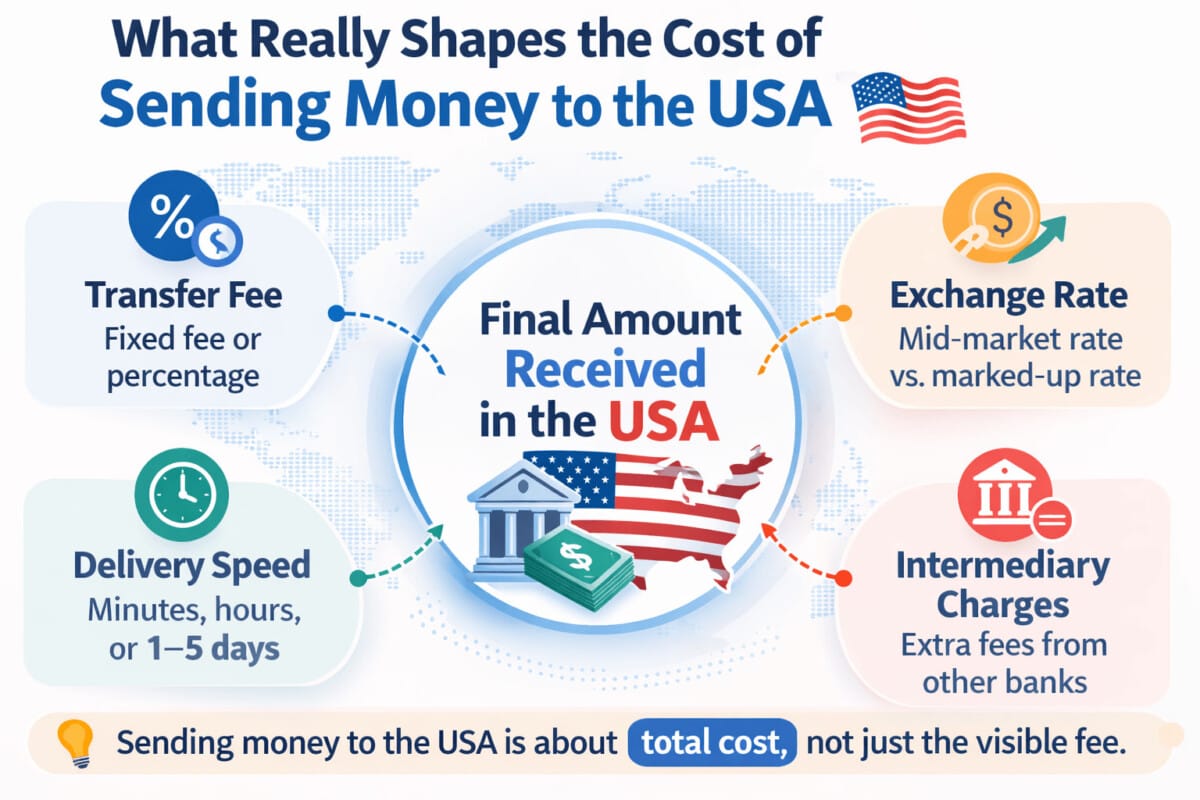

How to send money to the USA. If you need to send money to the USA, the most important question is not “Which service has the lowest fee?” The better question is: How much money will actually arrive in the United States after fees, exchange rates, and any extra charges are applied?

That is where many people make the wrong comparison. An international transfer can look cheap at first glance, but the total cost may be higher once a weaker exchange rate or intermediary fee is built into the transaction. Wise explains this clearly in its US transfer guidance by emphasizing that total cost is not just the visible fee, but also the exchange rate used for the transfer.

In other words, sending money to the USA is not just about transfer fees. It is about total cost, delivery speed, accuracy of bank details, and choosing the right transfer method for your situation.

Why sending money to the USA is more complicated than it looks

People send money to the United States for many reasons. It might be tuition for a university, rent for an apartment, support for family, payment to a freelancer, business expenses, or a transfer to your own US bank account. The reason matters because the best transfer method often depends on the type of payment.

A large tuition payment or business payment may be better suited to a traditional international wire through a bank. A smaller recurring transfer for living expenses may be easier through a fintech money transfer service. The “best option” is not universal. It depends on the amount, the urgency, the documentation required, and how the recipient wants to receive the money.

This is why articles about how to send money to the USA should go beyond generic price comparisons. Readers usually want a practical answer: What do I need, what will it cost, how long will it take, and should I use a bank or a fintech service?

What information you need to send money to a US bank account

Before you send money, you need to collect the correct recipient information. In most cases, that includes:

- Recipient’s full legal name

- Recipient’s address

- US bank name

- Bank account number

- ABA routing number for certain US bank transfers

- SWIFT/BIC code for international wire transfers when required

- Sometimes the bank’s address or an additional payment reference

Chase explains that wire transfers require information such as the recipient’s account details and routing information, while Bank of America notes that international wires typically require the recipient’s name, address, bank information, and account number. Bank of America also says international wires may take 1 to 5 business days.

This is where many transfers go wrong. People assume that just having a US account number is enough. In reality, the required information depends on the transfer route. A bank wire may require different details from a fintech bank deposit flow. If the payment is large, even a small mistake in the bank details can create delays, rejection, or extra costs.

Common US banks people often send money to

If you are sending money to the United States, the recipient may use one of the major US banks, such as:

- Bank of America

- Chase

- Wells Fargo

- Citibank

- U.S. Bank

- PNC Bank

- Capital One

- TD Bank US

In practice, the most commonly referenced large-bank destinations are usually Bank of America, Chase, Wells Fargo, Citibank, and U.S. Bank, all of which provide wire or transfer instructions for customers receiving or sending funds.

This matters because readers often are not asking about international transfers in the abstract. They are dealing with a real situation: a landlord with a Chase account, a relative with Bank of America, a university using Wells Fargo, or a business partner with Citibank. A useful guide should reflect that real-world context.

How traditional bank transfers to the USA work

A traditional bank transfer usually means an international wire transfer. The typical process looks like this:

- Start an international wire transfer through your bank’s app, website, or branch.

- Enter the recipient’s US bank details.

- Choose the amount and transfer currency.

- Review fees, exchange rates, and estimated delivery time.

- Provide any required documentation or payment purpose information.

- Confirm and send the transfer.

Traditional banks remain strong in formal payment situations. If you are sending a large amount, paying tuition, making a legal or property-related payment, or sending business funds, a bank wire may be the most appropriate route.

But bank transfers are not always transparent in total cost. Bank of America notes that some foreign currency transfers may have no separate wire fee while still including an exchange rate markup. That means a transfer can appear inexpensive even if the recipient ultimately receives less favorable value.

That is why fees alone do not tell the full story.

How fintech services send money to the USA

Fintech transfer platforms usually make the process easier for individuals. A typical process looks like this:

- Create an account with a transfer service.

- Enter the sending country, amount, and destination country.

- Add the recipient’s US bank account details.

- Review the fee, exchange rate, and estimated delivery time.

- Pay using a supported method such as bank transfer, debit card, or another available option.

- Track the transfer in the app or online dashboard.

Wise says it shows fees upfront and uses the mid-market exchange rate for many transfers. Western Union’s online transfer flow also starts by showing amount, destination, and payment options, and notes that identity verification may be required for some transfer methods.

For many readers, the real appeal of fintech is not only speed. It is clarity. Users can often see the expected arrival amount before confirming the transfer. That makes fintech attractive for family support, rent, recurring monthly transfers, and smaller personal payments.

Fees vs. exchange rates: what really matters?

This is the part many readers overlook.

A transfer service can advertise a low fee, but if the exchange rate is less favorable, the total result may still be worse. Wise explicitly frames the issue as fee plus exchange rate, not fee alone.

That matters even more when the amount is large. A small difference in exchange rate may barely matter on a small transfer, but it can make a meaningful difference on tuition, savings transfers, or business payments.

So when readers search for the best options to send money to the USA, they should compare:

- Total fee

- Exchange rate

- Estimated arrival amount in USD

- Delivery time

- Possible intermediary or receiving charges

That is a far better comparison than looking only at the transfer fee shown on the first screen.

Traditional banks vs fintech services

| Comparison point | Traditional banks | Fintech services |

|---|---|---|

| Typical examples | Bank of America, Chase, Citibank, U.S. Bank | Wise, Western Union, Remitly |

| Main transfer method | International wire transfer | App-based or web-based international transfer |

| Information required | Recipient name, address, account number, ABA or SWIFT details | Recipient information, US bank account details, service-specific verification |

| Speed | Often 1–5 business days for international wires | Can be faster depending on route, funding method, and service |

| Cost structure | Fee plus possible FX markup and intermediary charges | Usually clearer upfront display of fee and expected delivery amount |

| Exchange-rate transparency | Often less obvious to the average user | Often more visible during checkout |

| Best for | Large transfers, tuition, business payments, formal or document-heavy transactions | Smaller recurring transfers, family support, rent, convenience-driven use cases |

| Main advantage | Strong for formal, high-value, bank-centered payments | Strong for usability, transparency, and quick comparison |

| Main drawback | Total cost may be harder to estimate | Limits, verification steps, or route restrictions may apply |

| Key risk | Errors may be hard to reverse once a wire is sent | Speed and pricing can vary depending on payment method and country |

The point is not that one side is always better. The point is that they solve different problems well.

When a traditional bank may be the better option

A traditional bank may make more sense if:

- You are sending a large amount

- The payment is for tuition, property, legal fees, or corporate use

- The recipient specifically requests a bank wire

- You need a more formal banking record and documentation trail

Banks are especially useful when the transaction needs to look and feel like a conventional institutional payment.

When a fintech service may be the better option

A fintech transfer service may make more sense if:

- You are sending living expenses or family support

- You want a clearer view of the final amount the recipient will get

- You care about app convenience and simpler setup

- You are sending smaller amounts more regularly

- You want to compare total cost more easily before confirming

For personal transfers, the convenience difference can be significant.

A simple way to choose the best option

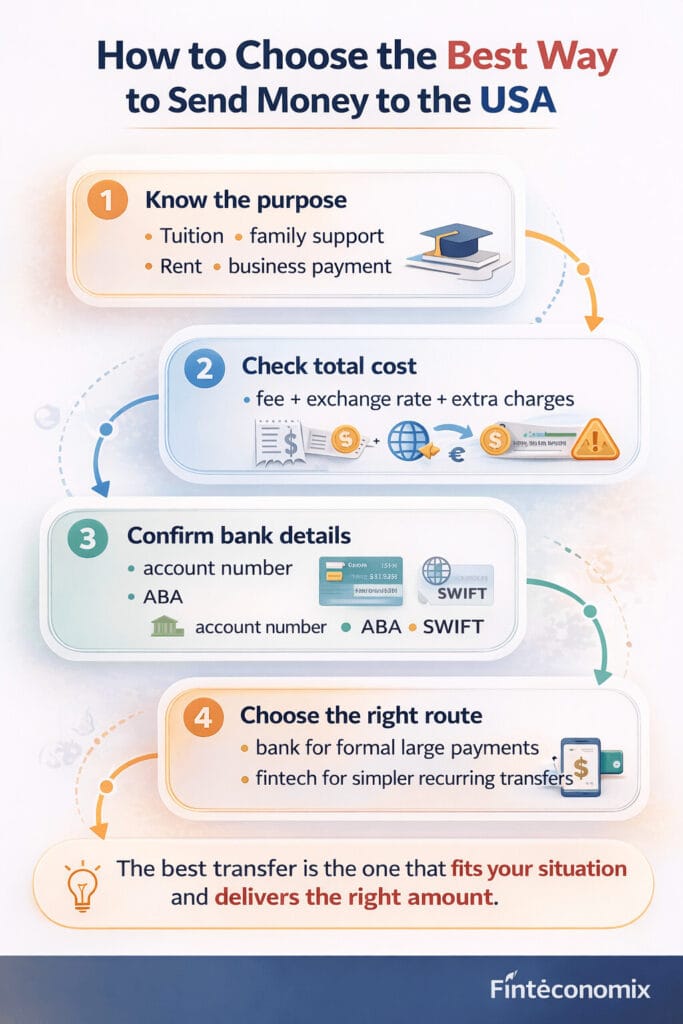

If you are unsure which method to use, make the decision in this order:

First, define the purpose of the transfer. Is it tuition, rent, family support, business payment, or a personal account transfer?

Second, compare the final amount the recipient will receive, not just the headline fee.

Third, check the delivery time and whether any intermediary charges may reduce the payment.

Fourth, make sure the recipient’s bank details are correct, especially the account number, routing number, and any SWIFT information required.

That simple process is more useful than starting with brand names alone.

What to do before you send money to the USA

Before you send money, do three things.

Decide exactly how much the recipient in the United States needs to receive. Then compare both a traditional bank and a fintech option based on the final delivered amount in USD, not just the transfer fee. Finally, confirm the bank details carefully, including the account number, ABA routing number, and any SWIFT/BIC information required for the transfer route. If the payment is large or formal, such as tuition, a contract payment, or a business transfer, a bank wire may be the better fit. If it is a personal or recurring payment, a fintech service may be simpler and more cost-effective.

Consumer protection and why details matter

For US consumers sending money abroad, the Consumer Financial Protection Bureau explains that certain remittance transfers include protections related to disclosures, cancellation, and error resolution. The CFPB states that qualifying remittance transfers generally require clear information about fees, exchange rates, and the amount the recipient will receive, and it also describes a 30-minute cancellation window in many cases.

Even if your transfer is not made from within the United States, that framework still reinforces an important principle for readers everywhere: always review the full terms before confirming an international payment.

Final thoughts

The best way to send money to the USA is not simply the cheapest-looking option on the first screen. It is the option that gives you the best combination of final delivered amount, exchange-rate fairness, speed, and fit for your situation.

Traditional banks remain important for larger and more formal transfers. Fintech platforms are often more convenient and easier to compare for smaller or recurring payments. Neither is automatically the best choice every time.

If you want to make a better decision, focus on three things: why you are sending the money, how much will actually arrive, and whether a bank or fintech route matches the payment purpose better. That approach will help you avoid hidden costs, weak exchange rates, and unnecessary transfer delays.