A practical guide to open banking api concepts, real examples, implementation flow, security, and country differences

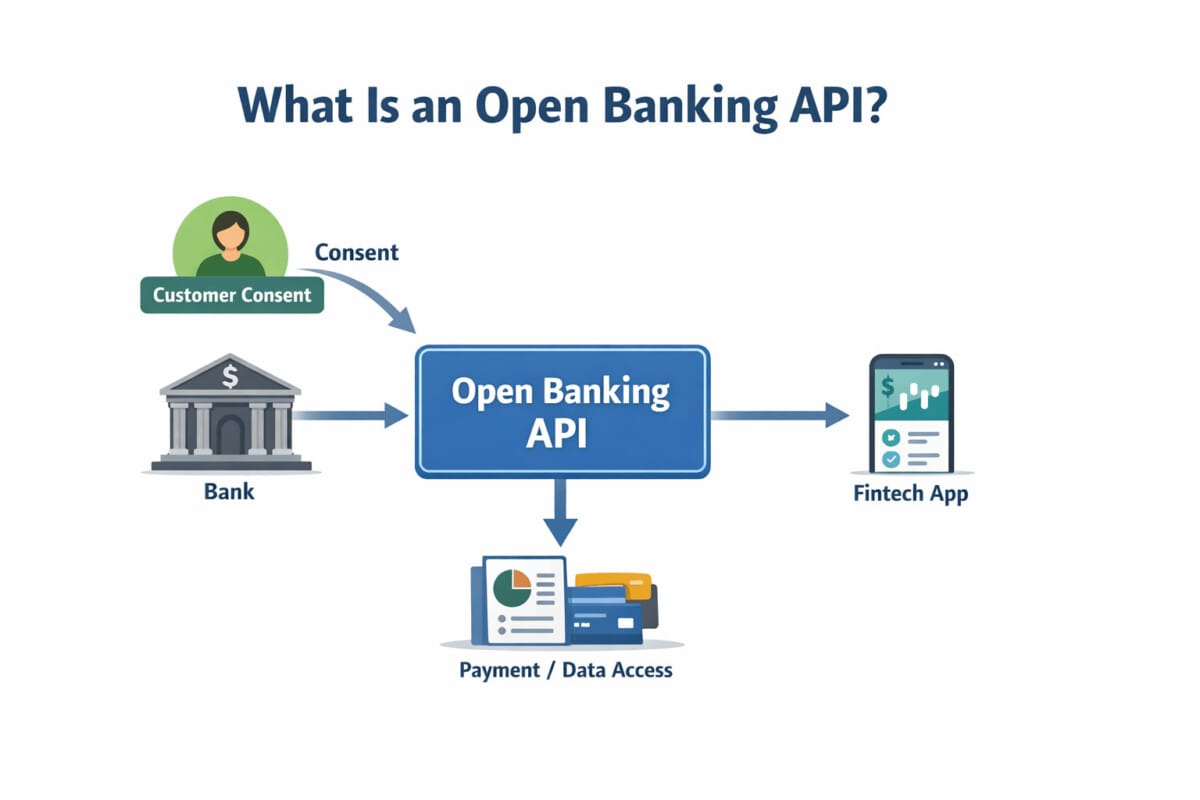

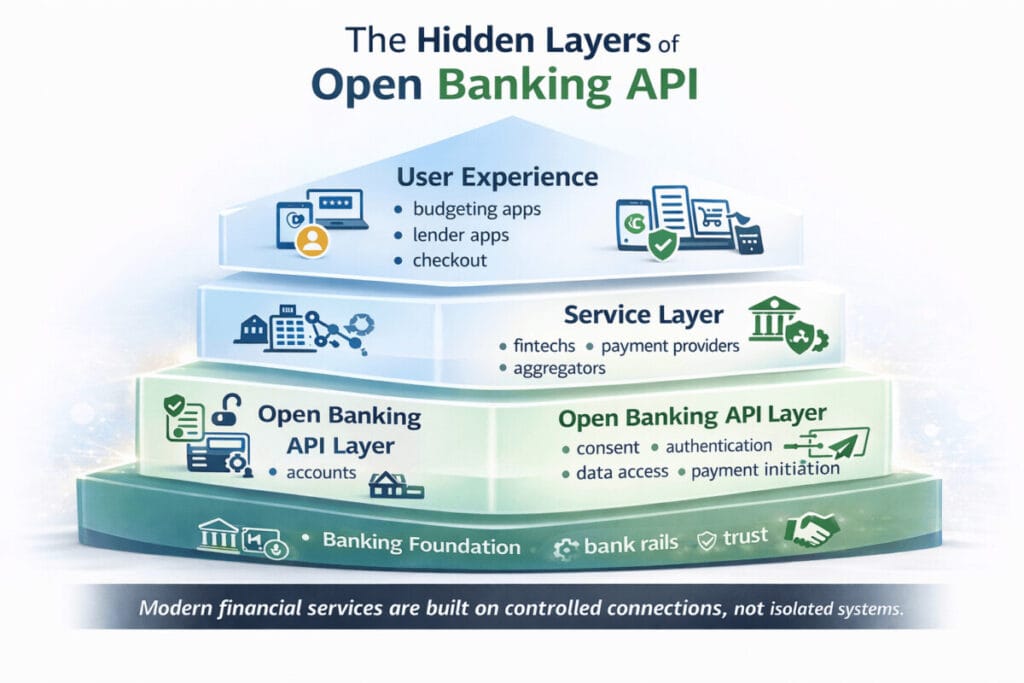

Open Banking API is a standardized interface that allows third-party services to access bank account data or initiate payments from a bank account with the customer’s explicit consent. In simple terms, it is the structure that lets banks, fintech apps, lenders, and payment services connect in a controlled and secure way.

Many people who search for open banking api are not only looking for a basic definition. They are often trying to understand how account linking works, why bank authentication is required, how pay by bank works, how fintech apps read transaction data, and why open banking looks different in the UK, the US, and Australia.

That is why a useful explanation of open banking api needs to go beyond theory. It has to explain the real workflow, the business use cases, the technical integration points, and the security logic that make the model work in practice.

What is an Open Banking API?

An Open Banking API is the connection layer that enables approved third parties to interact with bank systems through structured and permission-based requests. Instead of relying on unstable methods like screen scraping, open banking uses formal API access, customer consent, scoped permissions, and secure authentication.

At a high level, open banking api supports two major functions:

- Access to financial data, such as account information, balances, and transaction history

- Payment initiation, where a customer authorizes a payment directly from a bank account

This means open banking is not only about data sharing. It is also about creating a new way for payments and financial services to interact with bank accounts.

Why Open Banking API matters

Financial services no longer live inside one bank app. A budgeting tool may need access to multiple bank accounts. A lending platform may want to assess income and cash flow in more detail. An e-commerce checkout may want to offer direct bank payments instead of only cards.

This is where open banking api becomes important. It makes these connections possible through a more secure and standardized model.

Instead of asking for online banking credentials directly, the service redirects the customer to the bank’s own authentication flow. The customer logs in there, approves the request, and allows only the specific access needed.

This changes the structure of competition in finance. The question is no longer only who owns the data. The more important question is who can connect to it safely, with clear consent, within a regulated framework.

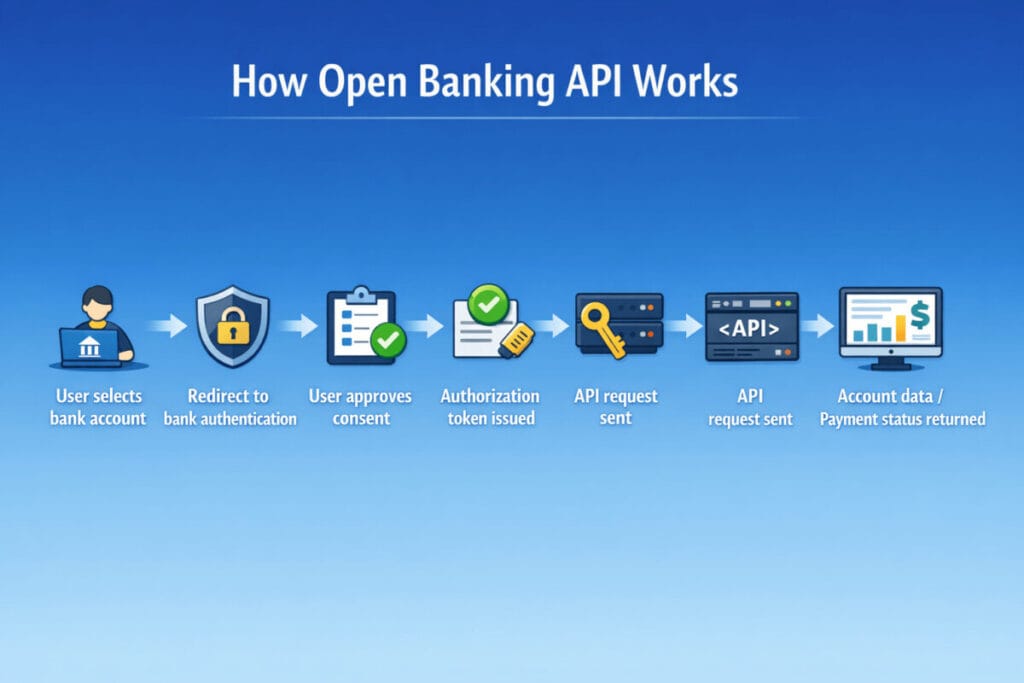

How an Open Banking API works

The core workflow is straightforward.

- A user chooses to connect a bank account inside a fintech app, payment service, or financial platform.

- The service redirects the user to the bank or approved open banking authentication page.

- The user logs in and approves the requested permissions.

- The service receives an authorization code or token.

- The service uses that token to call the bank or open banking provider API.

- Approved data or payment status is returned.

This model matters because the third-party service does not need to store the user’s internet banking password. Authentication happens in the bank-controlled environment, and the permission granted is limited in scope and duration.

What an Open Banking API can do

| Function | What it does | Common use case |

|---|---|---|

| Account information access | Retrieves account lists, balances, and account details | Personal finance apps, accounting tools |

| Transaction data access | Reads transaction history and cash flow patterns | Budgeting, underwriting, income verification |

| Payment initiation | Starts a payment directly from a bank account | Pay by bank, bill payment, checkout flows |

| Consent management | Controls what data is shared and for how long | Permission approval, renewal, revocation |

| Multi-bank aggregation | Combines data from multiple institutions | Financial dashboards, business treasury tools |

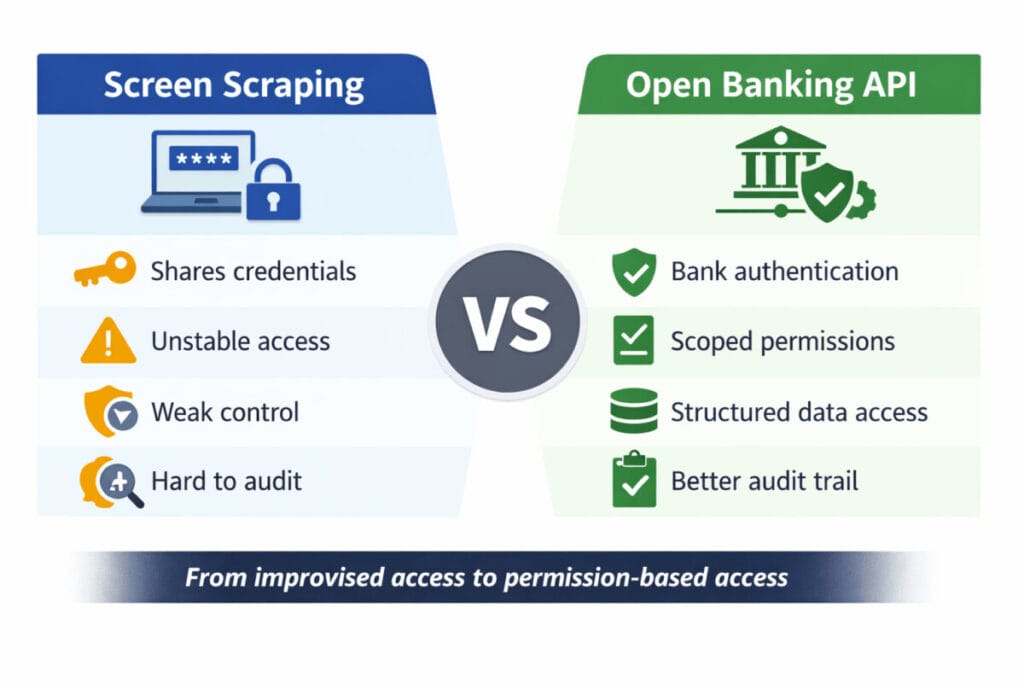

Open Banking API vs screen scraping

Before open banking became more common, many services used screen scraping. That meant collecting a user’s online banking credentials, logging in on their behalf, and reading information from the bank’s website or app interface.

This approach had obvious weaknesses. It depended on front-end layouts that could change. It created security concerns. It made auditability and permission control harder.

Open Banking API is different because it uses official interfaces, controlled authentication, and scoped access. It is more structured, more transparent, and more compatible with long-term financial infrastructure.

That is why open banking api is not just a technical upgrade. It is a shift from improvised access to governed access.

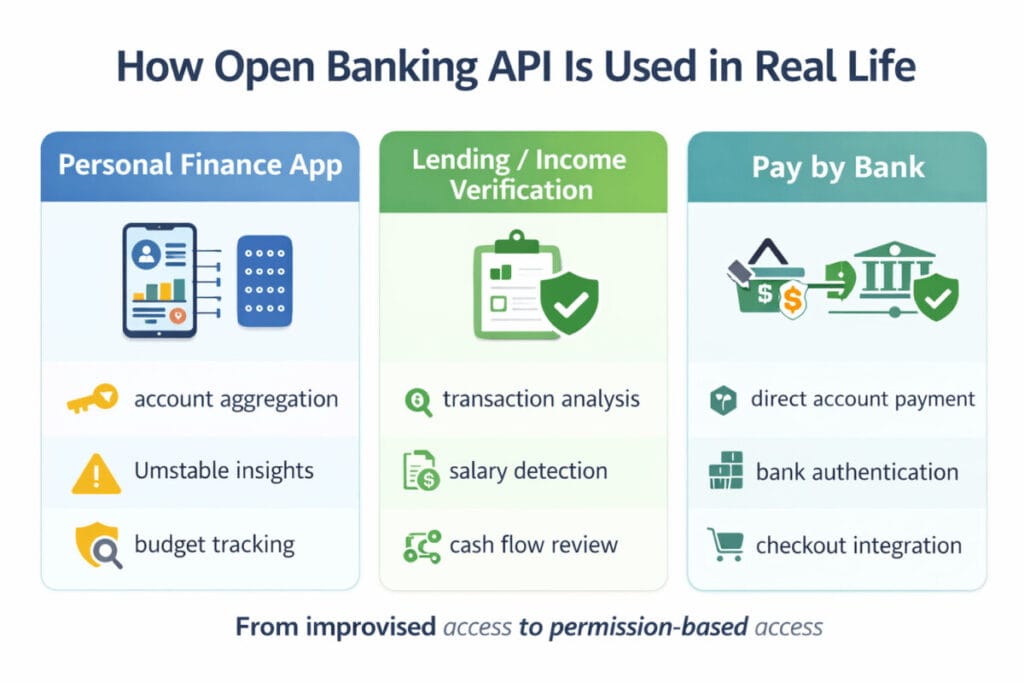

Real example 1: a personal finance app

One of the most common open banking api use cases is a personal finance or budgeting app.

A user opens the app and taps Connect your bank account. The app then redirects the user to a supported bank or open banking authorization screen. The user authenticates there and approves specific permissions such as:

- account details

- current balance

- transaction history

Once approval is complete, the app receives a token and starts calling the relevant APIs. It may pull account balances, recent transactions, salary inflows, subscription payments, and recurring bills.

That information can then be turned into practical features such as:

- monthly spending summaries

- subscription tracking

- cash flow forecasting

- category-based budgeting

- alerts for low balances or unusual payments

From the user’s perspective, it feels like one connected financial dashboard. From the service’s perspective, open banking api is the infrastructure that transforms raw account access into a product experience.

Real example 2: pay by bank at checkout

Another major use case is account-to-account payment initiation.

Imagine an online merchant that offers card payment, digital wallet payment, and pay by bank. If the customer chooses the bank payment option, the payment provider starts an open banking flow.

The customer is redirected to the bank’s authentication process, approves the payment, and the payment instruction is initiated from the bank account. In this model, the payment does not necessarily depend on a traditional card rail.

This is one reason open banking api matters in payments. It is not only about reading data. It can also support a different checkout model with different economics, operational logic, and user experience.

In practice, payment teams do not look only at payment success. They also monitor:

- drop-off during authentication

- bank-specific response times

- failure reasons

- webhook timing

- reconciliation quality

- refund and exception handling

That is why open banking payments are both a technical integration and an operational design problem.

How Open Banking API integration works in practice

In real implementations, companies do not always connect directly to every bank. Many use an intermediary open banking platform, aggregator, or provider that already handles multiple bank connections.

A typical integration flow may look like this:

- The app asks the backend to create a consent request or authorization session.

- The backend calls the open banking provider API.

- The frontend redirects the user to the bank authorization page.

- After the user approves access, the backend exchanges the authorization code for an access token.

- The backend calls endpoints such as

/accounts,/balances, or/transactions. - The service normalizes the returned data into its own internal schema.

- The system manages token expiry, consent renewal, revocation, and logging.

In production, the hard part is often not the first API call. The hard part is everything around it:

- token lifecycle management

- re-authentication flows

- duplicate transaction prevention

- retry logic

- rate limit handling

- consent expiry

- data minimization

- audit logs

- monitoring and alerting

That is why an open banking api project is rarely just a simple feature request. It is usually a financial systems project involving product design, backend engineering, compliance, operations, and security.

Simplified Open Banking API flow

User App

→ Backend Server

→ Open Banking Provider / Bank API

→ Consent & Authentication

← Access Token

← Account / Balance / Transaction Data

Simple API example

Below is a highly simplified example of how a service might call an open banking api after receiving an access token.

import requests

access_token = "your_access_token"

headers = {

"Authorization": f"Bearer {access_token}",

"Content-Type": "application/json"

}

# Get linked accounts

accounts_res = requests.get(

"https://api.example.com/open-banking/accounts",

headers=headers,

timeout=10

)

accounts = accounts_res.json()

# Get transactions for one account

account_id = accounts["data"][0]["account_id"]

transactions_res = requests.get(

f"https://api.example.com/open-banking/accounts/{account_id}/transactions",

headers=headers,

timeout=10

)

transactions = transactions_res.json()

print(transactions)

The code itself may look simple, but real-world implementation is much broader. A production-grade integration has to consider error handling, data mapping, token refresh, user consent changes, retry policies, and privacy constraints.

Country differences in Open Banking API

The phrase open banking api may sound universal, but the structure varies by market.

| Region | Main characteristic | What matters most |

|---|---|---|

| UK | Mature open banking standards and API specifications | Payment initiation, AIS/PIS, security profiles |

| US | Strong focus on consumer financial data rights and access rules | Consumer control, data portability, standard-setting |

| Australia | Consumer Data Right framework shapes financial data sharing | Safe sharing, switching, comparison, portability |

These differences matter because they affect how firms build products, how permissions are managed, and what type of open banking business model is realistic in each market.

Where security comes from

Open Banking API is not secure just because it uses an API. It is secure when the entire access model is designed well.

That means:

- explicit customer consent

- strong authentication

- limited permission scope

- access expiration rules

- revocation mechanisms

- auditability

- secure token handling

In other words, open banking is not about opening everything. It is about opening only what is necessary, in a traceable and controlled way.

This distinction is important for consumers, developers, lenders, and payment firms alike. Good security in open banking api is really about precision, not just restriction.

The most important questions to ask about an Open Banking API

| Question | Why it matters |

|---|---|

| Does it support only data access, or also payment initiation? | The business model changes completely |

| Can users easily revoke permissions? | Consumer protection depends on it |

| Is the security model standardized? | Operational trust and scalability depend on it |

| How are bank-level differences handled? | Product reliability depends on it |

| How good are the docs and sandbox tools? | Integration speed depends on it |

These are not only developer questions. They also matter to product managers, fintech founders, risk teams, compliance officers, and payment strategists.

Why Open Banking API will keep growing

The future of open banking api goes beyond account aggregation. It will likely play a bigger role in:

- account-to-account payments

- income verification

- credit decisioning

- treasury automation

- merchant checkout

- financial comparison tools

- embedded finance

As financial systems become more connected, the quality of the connection layer becomes more important. Open banking sits exactly in that layer.

It is the infrastructure that allows customer-controlled data sharing and bank-connected services to function at scale.

Final thoughts

Open Banking API is not just a technical term for developers. It is one of the key building blocks behind modern financial connectivity.

It explains how fintech apps connect to bank accounts, how data sharing is structured, how consent is managed, and how direct bank payments can be initiated without relying only on cards.

Anyone searching for open banking api is ultimately asking a bigger question: how does the modern financial system connect safely across institutions, apps, and payment flows?

That is exactly what open banking is trying to solve.

References

- UK Open Banking Standards, API Specifications: https://standards.openbanking.org.uk/api-specifications/

- CFPB, Required Rulemaking on Personal Financial Data Rights: https://www.consumerfinance.gov/rules-policy/final-rules/required-rulemaking-on-personal-financial-data-rights/

- ACCC, The Consumer Data Right: https://www.accc.gov.au/by-industry/banking-and-finance/the-consumer-data-right

- Stripe, Open banking APIs explained: https://stripe.com/resources/more/open-banking-apis-explained-what-they-are-and-how-they-work

- Stripe, What is open banking and how does it work?: https://stripe.com/resources/more/open-banking-explained