The part of finance most people never see

Every day, trillions of dollars move through the global financial system. Salaries are paid, securities are traded, derivatives are cleared, government bonds are settled, and cross-border obligations are completed across time zones. Most of that activity looks smooth from the outside. A payment is sent. A trade is executed. A balance changes on a screen.

But none of that works on trust alone.

Behind every completed transaction sits a deeper layer of systems, rules, institutions, and risk controls that make financial markets function. That layer is called Financial Market Infrastructure, or FMI. Globally, FMI refers to the critical arrangements that support the payment, clearing, settlement, and recording of transactions, including payment systems, central securities depositories, securities settlement systems, central counterparties, and trade repositories.

The easiest way to think about Financial Market Infrastructure is this: it is the operating system of modern finance. Banks, exchanges, asset managers, brokers, payment providers, and fintech firms may be the brands people recognize, but FMI is the machinery that makes their promises final.

What financial market infrastructure actually does

A transaction is not really complete when two parties simply agree to do business. A great deal still has to happen after that point.

Cash has to move. Securities have to be delivered. Ownership has to be updated. Exposures have to be measured. Collateral has to be posted. Defaults must be handled if a participant fails. Records have to be maintained so regulators, counterparties, and the market itself can trust the result.

That is the real job of Financial Market Infrastructure. It exists to make sure financial transactions do not just begin, but actually finish in a safe, orderly, and legally reliable way. The CPMI describes its role in promoting the safety and efficiency of payment, clearing, settlement, and related arrangements in support of financial stability and the wider economy.

This is why FMI is not just a technical issue. It sits at the intersection of law, operations, liquidity, technology, governance, and risk management. If any one of those layers breaks at the wrong moment, the consequences can spread far beyond a single institution.

The core types of financial market infrastructure

The acronym-heavy language around FMI can make the topic sound more complicated than it really is. The main building blocks are straightforward once they are laid out clearly.

| Infrastructure Type | What it does | Why it matters |

|---|---|---|

| Payment System (PS) | Transfers funds between participants | Keeps money moving across the financial system |

| Central Securities Depository (CSD) | Holds securities and records ownership | Supports safekeeping and transfer of securities |

| Securities Settlement System (SSS) | Finalizes securities transactions | Ensures delivery and payment are completed correctly |

| Central Counterparty (CCP) | Becomes the buyer to every seller and seller to every buyer | Reduces bilateral counterparty risk and centralizes risk management |

| Trade Repository (TR) | Collects and stores transaction data | Improves transparency, reporting, and oversight |

These categories are the internationally recognized core types of FMIs under the PFMI framework.

Each of them plays a different role, but together they do something essential: they turn financial activity into completed financial obligations that the market can rely on.

Why financial market infrastructure matters so much

The value of FMI becomes obvious when you imagine the alternative.

Without reliable payment systems, large-value transfers would stall and liquidity would become trapped. Without securities settlement systems, trades could be agreed but never fully completed. Without central securities depositories, the market would struggle to maintain a trusted record of ownership. Without central counterparties, bilateral exposures could become more tangled and more dangerous during periods of market stress. Without trade repositories, regulators and participants would have a much weaker view of what risks are building in the system.

That is why Financial Market Infrastructure matters so much in conversations about systemic risk. FMI reduces uncertainty by creating rules, processes, and safeguards around finality, default management, collateral, liquidity, and operational continuity. But it also concentrates crucial functions in a relatively small number of infrastructures, which means strong design and oversight are essential. The PFMI were developed precisely to strengthen the robustness of the infrastructure supporting global financial markets and help it withstand financial shocks.

Finance can tolerate many kinds of noise. What it cannot tolerate for long is uncertainty about whether transactions will settle.

Payment, clearing, and settlement are not the same thing

One reason this topic confuses many readers is that payments, clearing, and settlement often get lumped together. They are related, but they are not identical.

A payment is the transfer of funds.

Clearing is the process of transmitting, reconciling, and in some cases netting obligations before final completion.

Settlement is the final discharge of those obligations through the transfer of cash, securities, or both.

This distinction matters because a transaction can appear complete at one stage while still carrying risk at another. A trade can be executed but not yet settled. A payment message can be sent but not yet final. A derivatives position can be economically agreed while the associated exposures are still being managed through clearing arrangements.

Financial Market Infrastructure is what organizes these stages so that the market does not have to rely on informal trust or improvisation.

Where PFMI fits in

Any serious discussion of Financial Market Infrastructure eventually arrives at PFMI, the Principles for Financial Market Infrastructures.

PFMI is the global standards framework issued by CPMI and IOSCO for key financial market infrastructures. It is not a side note. It is the international benchmark that gives structure to the field. The PFMI apply to payment systems, CSDs, SSSs, CCPs, and TRs, and they are treated internationally as a key standard for preserving financial stability. (IOSCO)

What makes PFMI so important is that it moves the FMI discussion beyond vague phrases like “safe and efficient” and turns them into concrete expectations. The framework covers governance, credit risk, liquidity risk, collateral, settlement, default management, operational resilience, access, efficiency, transparency, and the responsibilities of authorities. BIS materials summarizing PFMI note that the framework contains 24 principles organized across major themes, along with responsibilities for central banks, regulators, and other relevant authorities.

That means when a market talks about whether an infrastructure is robust, resilient, well-governed, or systemically important, it is often using PFMI logic, whether it says so directly or not.

Why central counterparties get so much attention

Among all forms of Financial Market Infrastructure, CCPs often attract the most attention because they sit so directly at the center of market risk.

A central counterparty stands between the original buyer and seller in a transaction. Instead of each side relying on the other directly, both sides face the CCP. This structure reduces bilateral counterparty risk and can improve the manageability of defaults, but it also concentrates risk in one critical node. If that node is poorly managed, the consequences can be serious.

That is why CCPs are often discussed in the same breath as margin, default waterfalls, stress testing, and recovery planning. They are a powerful example of the broader FMI story: infrastructure can reduce risk across the market, but only if the infrastructure itself is exceptionally strong.

Why trade repositories matter more than they seem to

Trade repositories rarely get public attention because they do not sit in the consumer-facing part of finance. But they matter enormously in modern markets.

A TR stores transaction data, especially in areas like derivatives markets where visibility is essential. That may sound like a dry administrative function, but better data changes the quality of oversight. It helps authorities monitor exposures, identify concentrations, and understand how risk is building across the system. It also supports market transparency in environments where bilateral transactions might otherwise remain difficult to track.

In a financial system increasingly shaped by complexity and speed, the ability to see the market clearly is its own form of resilience.

Why financial market infrastructure becomes visible during stress

In calm conditions, good infrastructure disappears into the background. In stressed conditions, it becomes the story.

A serious outage in a major payment system can delay critical transfers and leave liquidity stuck in the wrong place at the wrong time. A settlement disruption can create uncertainty around who actually owns which assets. Stress at a central counterparty can force urgent questions about margin sufficiency, liquidity access, default resources, and continuity of service. Weak reporting systems can leave supervisors and participants flying blind just when visibility matters most.

This is why Financial Market Infrastructure is one of the most important foundations of financial stability. It is not simply back-office support. It is where market confidence becomes operational reality.

Financial market infrastructure in a more digital world

FMI is sometimes discussed as though it belongs to an older era of finance, but the opposite is true. As finance becomes faster, more digital, and more interconnected, FMI becomes even more important.

Real-time payment expectations put pressure on settlement design and liquidity management. Cross-border frictions raise fresh questions about interoperability and coordination. Cloud reliance increases the significance of operational resilience and third-party dependencies. Tokenization and digital money projects force a new round of debate around settlement finality, legal structure, governance, and risk allocation.

That is one reason CPMI and IOSCO have continued extending PFMI-related thinking into newer areas. IOSCO and CPMI have published guidance on the application of PFMI to systemically important stablecoin arrangements, showing that infrastructure standards are now being actively connected to emerging forms of digital finance.

The form of finance may evolve. The need for trusted infrastructure does not.

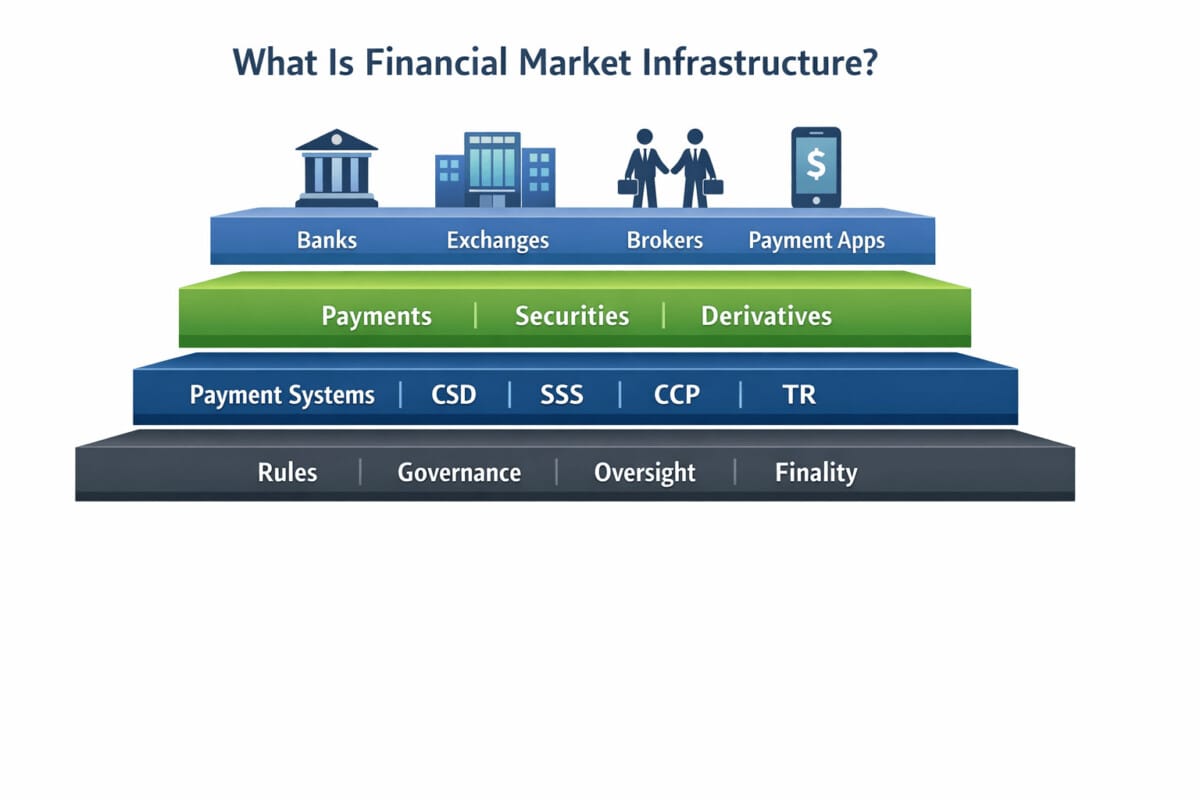

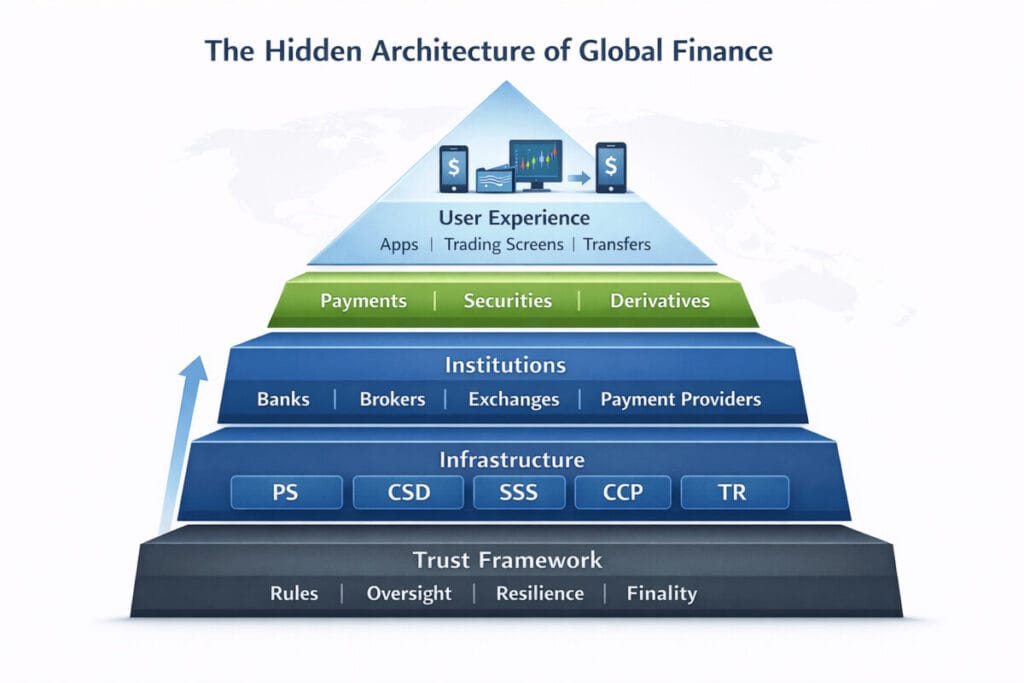

A simple way to see the hierarchy

The modern financial system can be understood in layers.

At the top are the user-facing experiences: banking apps, brokers, exchanges, card payments, treasury dashboards, corporate payments platforms, and digital wallets.

Below that sit the institutions and markets: banks, dealers, asset managers, payment providers, exchanges, and counterparties.

Beneath them is the real foundation: payment systems, securities settlement systems, central securities depositories, central counterparties, and trade repositories.

And beneath all of that sits the governance layer: laws, oversight, standards, central bank roles, supervisory expectations, and international principles such as PFMI.

That layered view helps explain why Financial Market Infrastructure feels invisible until it suddenly does not. It is not designed to be flashy. It is designed to be dependable.

The future of financial market infrastructure

The future of FMI will not be defined by one technology alone. It will be shaped by a combination of resilience, interoperability, data quality, governance, and the ability to adapt without sacrificing trust.

Some infrastructures will modernize through better messaging, richer data, and faster settlement capabilities. Some will evolve through stronger cross-border coordination. Others will face pressure from new forms of digital money, tokenized assets, and expectations around continuous availability.

But the core questions will remain familiar:

Can obligations be completed with legal certainty?

Can risk be measured and contained?

Can the infrastructure continue functioning under stress?

Can participants and authorities trust the process when market conditions become difficult?

Those questions are what make Financial Market Infrastructure so central to global finance. Markets may innovate at the edges, but the system still depends on whether the underlying infrastructure can carry the weight.

Final thoughts

Financial Market Infrastructure is the hidden framework that allows finance to move from agreement to completion. It is the difference between a transaction that looks done and one that is actually final. It supports payments, securities markets, derivatives activity, transparency, and systemic stability all at once.

That is also why PFMI belongs in the conversation. It gives global finance a common language for what good infrastructure should look like: safe, efficient, resilient, transparent, and capable of withstanding pressure when it matters most. CPMI and IOSCO state that the PFMI are designed to help ensure the safety, efficiency, and resilience of the infrastructures that support global financial markets, and that full and consistent implementation is fundamental. (IOSCO)

The institutions people see may define the surface of finance. Financial Market Infrastructure defines whether the system underneath them actually works.