Open Banking vs Cards in Subscription Payments

Subscription businesses live and die by recurring payments. Streaming platforms, SaaS tools, memberships, and monthly delivery services all depend on one thing: getting paid again next month without making the customer think too hard about it.

That is why cards became the default. They are familiar, global, and easy to plug into existing subscription billing systems.

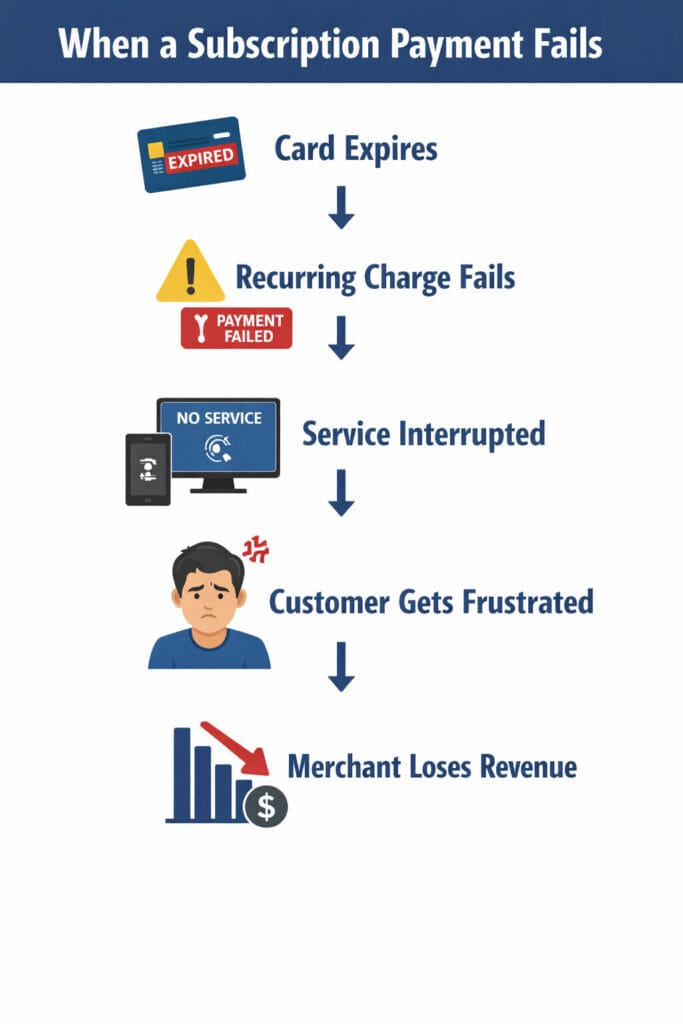

But cards also create a quiet problem. A card expires. A bank declines a charge. A replacement card is issued after suspicious activity. The customer never meant to cancel, but the payment fails anyway. Stripe describes this as involuntary churn and notes that it often comes from payment issues such as expired cards, declined transactions, and bank errors.

Why cards still dominate subscription payments

Cards still win on habit.

Most customers already know how card checkout works. Most merchants already have card rails, retry logic, tokenization, and billing tools in place. If your business wants fast signup and broad international reach, cards are still the easiest answer.

That convenience is powerful. In subscription payments, fewer steps at signup usually means fewer lost conversions. And for many businesses, that matters more than almost anything else.

The real weakness of card-based recurring billing

The problem is that card-based recurring billing depends on something that changes more often than businesses want: the card itself.

A customer may love the service and still churn because the renewal failed. That is what makes subscription payments different from one-time checkout. The goal is not just to collect money once. The goal is to keep collecting it smoothly, month after month.

For merchants, that means failed payments are not just an operations issue. They are a revenue leak.

If you want a good background read for this angle, Stripe’s guide on involuntary churn is worth linking in the published version. Stripe explicitly ties involuntary churn to expired cards, declined transactions, and payment failures in subscription businesses.

What open banking changes

This is where open banking for subscription payments becomes interesting.

Instead of relying on stored card credentials, open banking can let customers connect a bank account and authorize payments more directly. In the recurring payments context, one of the most important concepts is Variable Recurring Payments (VRP).

According to Open Banking Limited, VRPs let customers connect authorized payment providers to their bank account so payments can be made within agreed limits. Open Banking Limited also highlights subscription payments as a key use case and says VRPs can offer more control and transparency than card-on-file instructions.

That is a big deal for subscription billing.

With cards, the merchant stores a payment credential and hopes future renewals go through.

With open banking, the model can be framed more clearly around customer permission, limits, and bank-based recurring payment rules.

That does not automatically make it better. But it does make it different in a way that matters.

A useful source to link here is Open Banking Limited’s page on Variable Recurring Payments, because it explains why subscription services are one of the clearest real-world use cases.

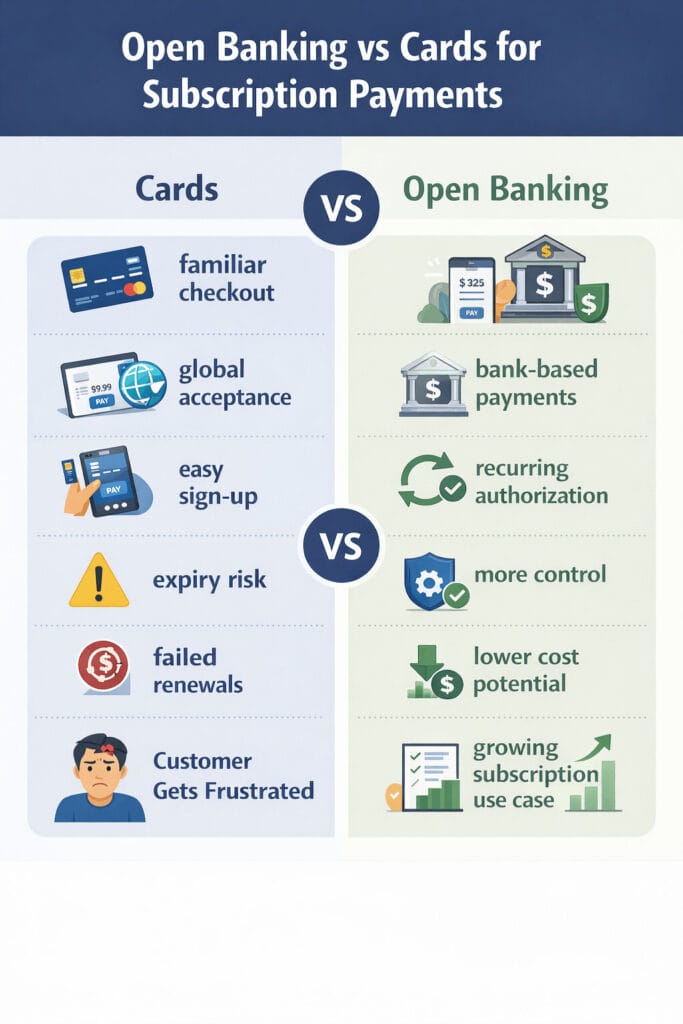

Open Banking vs Cards for Subscription Payments

| Category | Cards | Open Banking |

|---|---|---|

| Customer familiarity | Very high | Still growing |

| Signup friction | Usually low | Can be higher if the bank connection flow is clunky |

| Recurring billing model | Card-on-file | Bank-connected recurring authorization |

| Common failure point | Expired card, reissued card, declined transaction | UX friction, consent flow, local infrastructure limits |

| Merchant economics | Often more expensive | Potentially lower-cost account-to-account payments |

| Customer visibility | Often passive | Can be clearer around limits and permission |

| Best fit | Broad, proven, global use | Specific markets and cost-sensitive subscription models |

The short version is simple:

Cards win on familiarity. Open banking competes on structure, control, and potential cost efficiency.

A real-life example

Imagine someone pays for a music streaming service with a card.

The first signup is easy. They enter card details once, and the service renews every month. That feels effortless, until the card expires or gets replaced. Then the payment fails, the subscription pauses, and the customer gets an email asking them to update billing details.

Now imagine the same service using a strong open banking recurring payments flow.

The customer approves a bank-based setup once, within clear limits. If that experience is smooth, the merchant may have a recurring payment model that is less exposed to card lifecycle problems. The customer may also have better visibility into who can collect payments and under what rules. Open Banking Limited specifically presents subscriptions such as entertainment services, software, and gyms as examples where VRPs could help customers see who has payment permission and what limits apply.

That does not mean customers will instantly prefer open banking. It means the trade-off becomes more interesting.

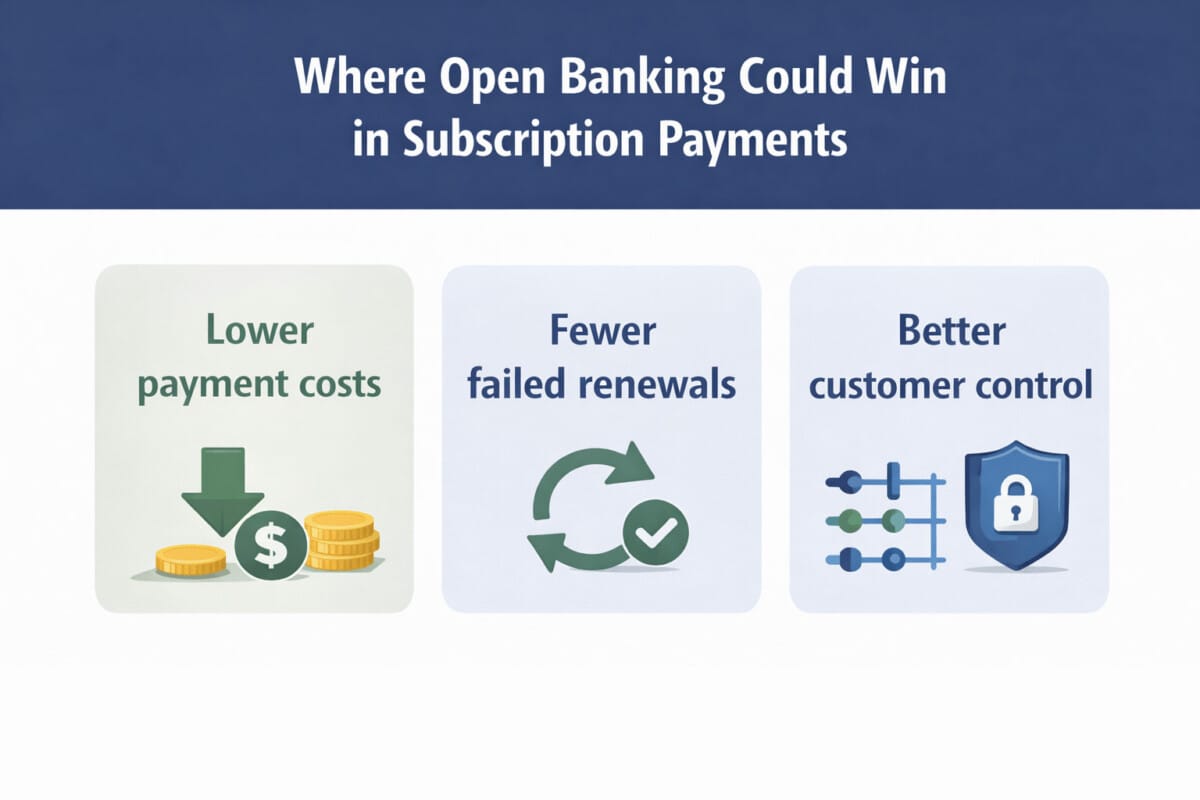

Where open banking could actually win

Open banking is most compelling when a subscription business cares a lot about these three things:

Lower payment costs

If margins are thin, even a modest cost difference matters. Open Banking Limited says VRPs may offer lower transaction costs than card payments and Direct Debits.

Fewer payment failures

Cards fail for reasons that have nothing to do with customer intent. If a bank-based recurring setup reduces dependence on card expiry and reissue cycles, that can help stabilize revenue. This is especially important in businesses hurt by failed subscription payments.

Better customer control

Open Banking Limited says VRPs can give customers more control and transparency than existing alternatives, including card-on-file instructions. For some businesses, that is not just a compliance story. It is a trust story.

Why cards are still hard to beat

Even if open banking has a stronger structure in some cases, UX still decides the winner.

If card checkout takes ten seconds and open banking setup takes multiple redirects, extra approvals, and too much explanation, cards will keep winning. Most users do not care about payment architecture. They care about whether signup feels easy and whether the service keeps working.

That is why the future of open banking vs cards for subscription payments will probably not be a full replacement story.

It will be a selective adoption story.

Cards will remain the default in many subscription businesses.

Open banking will be stronger where local infrastructure is mature, merchants are cost-sensitive, and recurring payment failure is a serious pain point.

Final take

Can open banking beat cards in subscription payments?

Yes, in some cases.

Not because cards are broken, but because subscription billing has specific pain points that open banking is well positioned to address: failed renewals, merchant cost pressure, and weak customer visibility.

Cards still own the advantage in familiarity, scale, and low-friction signup.

But open banking has a credible path in recurring payments where merchants want more control, better economics, and a model that is less tied to the life cycle of a plastic card.