What Actually Happens When You Pay Digitally

Every day we make payments without thinking much about them.

We buy coffee, shop online, or send money through a mobile app and simply assume that the payment is complete.

But behind that simple moment lies a vast digital payment infrastructure.

When you tap a card or confirm a payment on your smartphone, multiple financial institutions begin interacting in real time. Banks, card networks, payment processors, and even central banks coordinate to process a single transaction.

Modern payment systems are not just about moving money. They are part of a complex financial architecture that enables global commerce to function smoothly.

In this article, we will explore three fundamental questions:

- What is a payment?

- How do digital payments actually work?

- What roles do banks, card networks, and central banks play in the payment system?

Understanding this invisible infrastructure helps us see how the modern economy truly operates.

What Is a Payment?

At its most basic level, a payment is the transfer of value.

When a buyer receives a product or service, a payment is made in exchange for that value.

Throughout history, payment methods have evolved alongside technology:

- Cash

- Bank Transfer

- Card Payment

- Mobile Payment

- Digital Wallet

Despite these technological changes, the fundamental purpose of payments has remained the same.

A payment must ensure that:

- The buyer transfers value

- The seller receives value

- The transaction is securely recorded

However, in modern financial systems, money rarely moves instantly from one person to another. Instead, payments pass through multiple institutions before final settlement occurs.

This layered process forms the foundation of the modern payment system architecture.

What Consumers Experience When They Pay

From the consumer’s perspective, making a payment feels incredibly simple.

Imagine paying for coffee with a card.

The entire process usually involves only three steps:

- Tap a card or mobile wallet on the payment terminal

- Wait for the payment approval message

- Receive a receipt

This process typically takes only two to three seconds.

Yet during those few seconds, several financial systems and institutions are working together behind the scenes.

Although invisible to the consumer, this infrastructure is essential to making digital payments possible.

How Digital Payments Actually Work

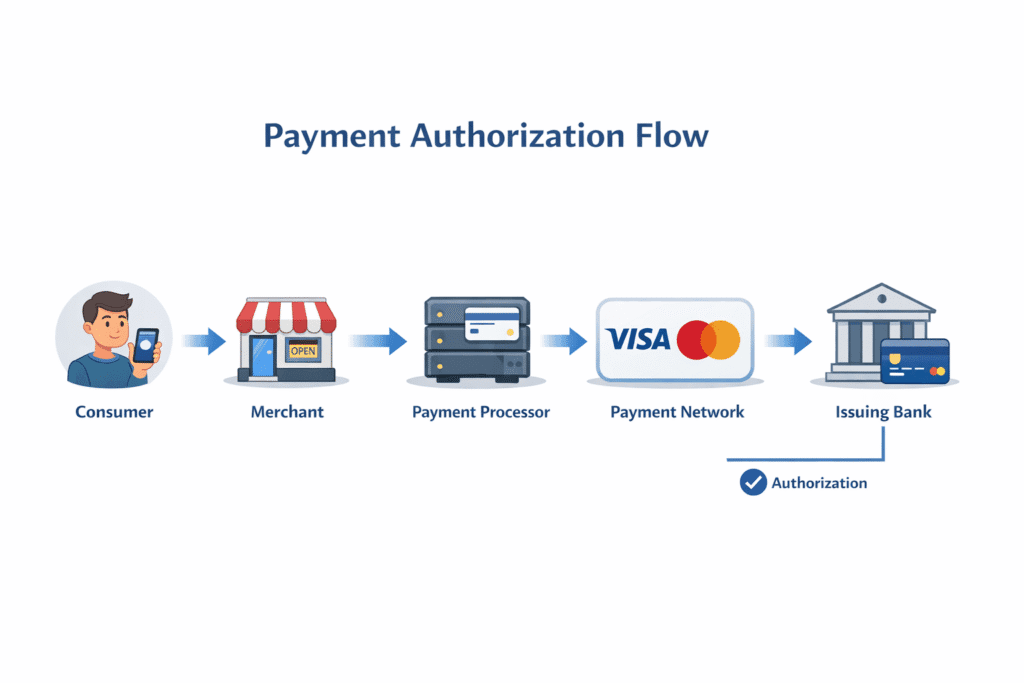

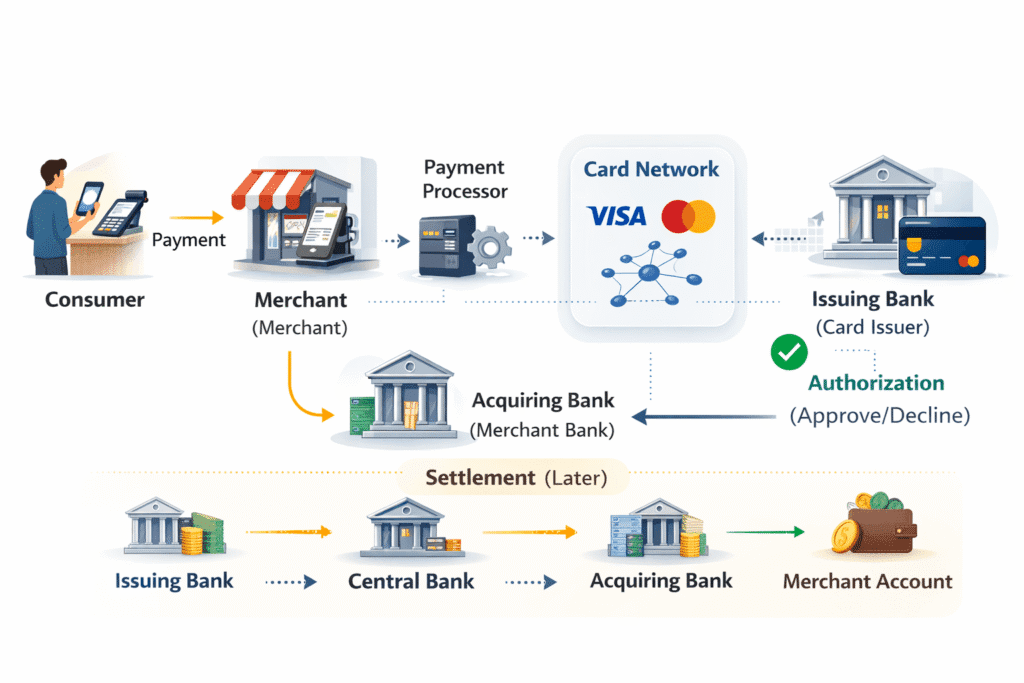

Digital payments rely on collaboration between multiple financial institutions.

When a card payment occurs, several participants are involved:

- Consumer – the buyer making the payment

- Merchant – the business receiving payment

- Payment Processor – the system that routes payment requests

- Card Network – the global payment network (Visa, Mastercard, etc.)

- Issuing Bank – the bank that issued the consumer’s card

- Acquiring Bank – the bank that provides payment services to the merchant

Understanding how card payments work requires examining two key stages.

Authorization

When a payment request is made, the issuing bank performs several checks:

- Is there sufficient credit or account balance?

- Is the card valid?

- Does the transaction appear fraudulent?

If the transaction passes these checks, the issuing bank sends an authorization approval back through the payment network to the merchant.

This entire process typically happens in a matter of seconds.

Clearing and Settlement

Even after authorization is approved, the actual transfer of funds does not occur immediately.

Instead, the payment moves through a clearing and settlement process.

During this stage:

- The card network organizes transaction data

- Banks calculate their obligations to each other

- Funds are transferred to the merchant’s bank account

This process usually takes one to several days to complete.

The Role of Banks in the Payment System

Banks are central to the operation of the payment system.

Their responsibilities include:

- Managing customer accounts

- Processing payment authorizations

- Handling interbank settlement

Two types of banks appear in card payment systems.

Issuing Bank

The issuing bank is the bank that issued the card to the consumer.

It decides whether to approve or decline a transaction based on:

- credit limits

- available balance

- fraud detection systems

Acquiring Bank

The acquiring bank is the bank that provides payment services to merchants.

It enables merchants to accept card payments and receive funds from transactions.

The Role of Card Networks

Card networks provide the connective infrastructure of the global payment system.

Major card networks include:

- Visa

- Mastercard

- American Express

- UnionPay

Their responsibilities include:

- transmitting payment messages

- processing transaction data

- operating clearing and settlement systems

In essence, card networks function as global routing systems that connect banks and merchants across the world.

The Role of the Central Bank

While most consumers never interact directly with central banks, these institutions provide the foundation for the entire payment system.

Central banks operate the infrastructure that allows banks to settle payments between one another.

Interbank Settlement

When funds move between banks, final settlement typically occurs using accounts held at the central bank.

Examples of major central bank settlement systems include:

- Fedwire (United States)

- TARGET2 (Europe)

- BOK-Wire+ (South Korea) https://www.bok.or.kr/eng/main/contents.do?menuNo=400412

These systems enable secure and reliable settlement between financial institutions.

Payment System Stability

Central banks are also responsible for maintaining the stability of national payment systems.

If payment systems fail, economic activity across an entire country could be disrupted.

Ensuring payment reliability is therefore a key function of central banking.

Digital Currency Innovation

Many central banks are now exploring Central Bank Digital Currency (CBDC).

CBDCs represent a potential new form of digital money issued directly by central banks and could reshape the future of payment systems.

Why Payment Systems Matter

Payment systems are not simply financial services.

They are critical infrastructure for the modern economy.

Efficient payment systems enable:

- faster economic activity

- lower transaction costs for businesses

- greater financial innovation

The mobile payments and digital wallets we use today are built on top of this underlying infrastructure.

Conclusion

When we tap a smartphone or swipe a card, an invisible financial system begins operating instantly.

Banks, card networks, payment processors, and central banks all work together to approve transactions within seconds. Afterward, clearing and settlement processes ensure that funds are ultimately transferred between institutions.

Payments are far more than simple money transfers.

They are a core infrastructure of the modern financial system and a key driver of fintech innovation.