Why API security matters so much in fintech

Most users never see an API.

They open an app, connect a bank account, check balances, make a payment, or verify their identity. Everything feels smooth and immediate. Behind that smooth experience, though, APIs are doing a huge amount of work. They move requests, pass data, connect systems, and make modern fintech feel fast.

That is exactly why API security matters.

In fintech, APIs are not just technical connectors. They are trust connectors. They sit between apps, banks, data providers, payment systems, and third-party platforms. If that connection is poorly protected, the problem is not just technical. It becomes a financial, operational, and reputational risk very quickly.

That is why API security in fintech is such a big deal. A beautiful app can still be fragile if the connections behind it are weak.

What API security in fintech actually means

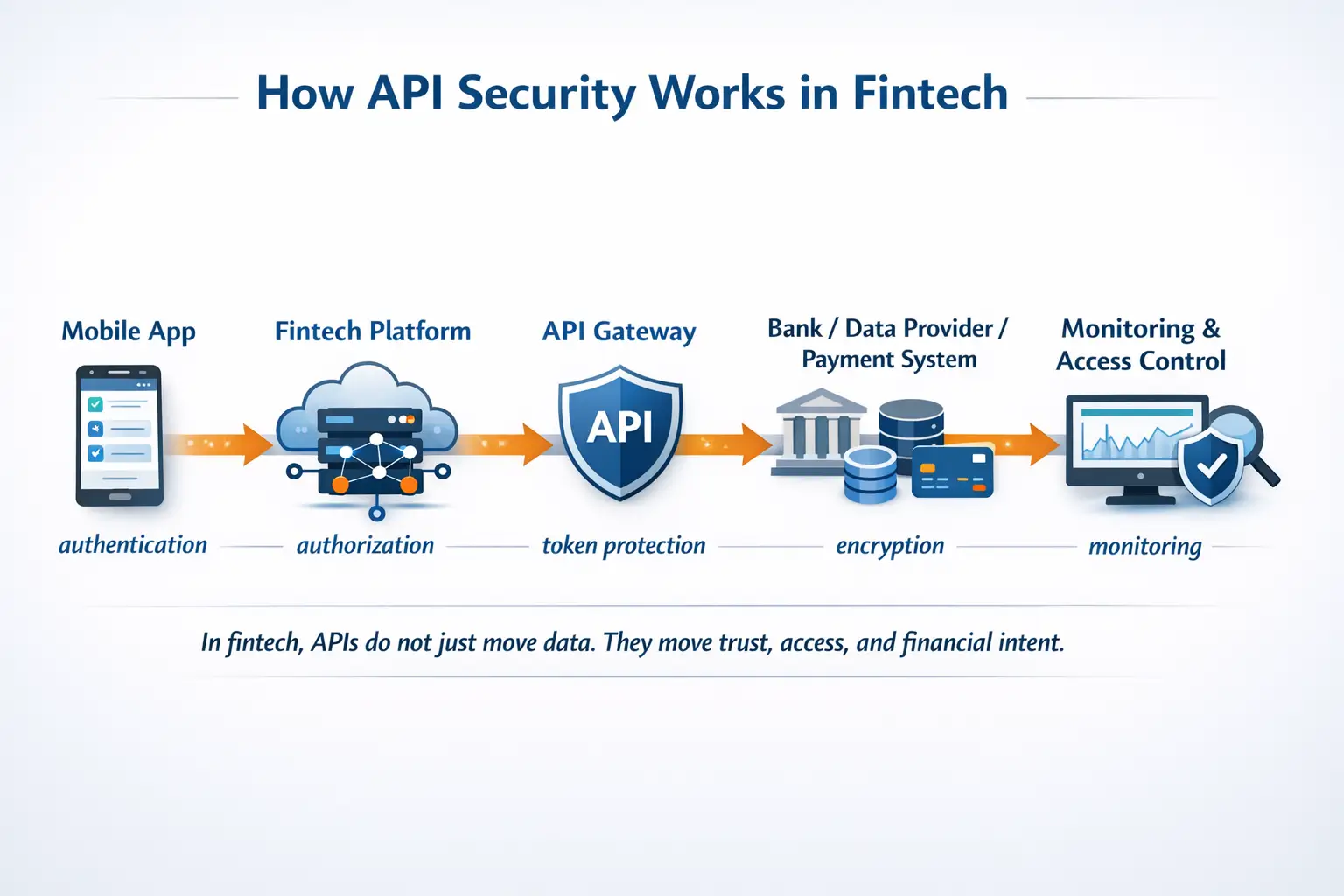

API security in fintech means protecting the digital interfaces that allow systems to exchange financial data, account information, payment instructions, identity signals, and service requests.

That protection usually includes:

- making sure only the right parties can connect

- limiting what each party can access

- protecting data while it moves

- detecting abnormal requests or misuse

- preventing abuse of tokens, credentials, and sessions

- monitoring API behavior over time

In simple terms, API security is about making sure that “connected” does not become “exposed.”

That matters because fintech is full of connected systems. Mobile apps connect to backend platforms. Platforms connect to banks. Banks connect to open banking providers. Payment systems connect to merchants, wallets, and risk engines. Every connection creates value, but every connection also creates a possible attack path.

Why fintech APIs carry more risk than ordinary APIs

Not every API handles the same level of risk.

An API for weather data and an API for account balances are not the same thing. A broken movie recommendation system is annoying. A broken financial API can expose sensitive data, enable fraud, or interrupt real money movement.

That is why API risk in fintech feels different.

Here is a simple way to think about it:

| API type | Low-risk example | Fintech example |

|---|---|---|

| Data sensitivity | public content or simple metadata | balances, transactions, identity data |

| User impact | inconvenience | financial loss, privacy loss, account abuse |

| Misuse potential | limited | fraud, impersonation, unauthorized access |

| Recovery difficulty | often simple | can involve legal, operational, and trust consequences |

In other words, fintech APIs do not just carry data. They often carry permission, identity, and financial intent.

Why open banking makes API security even more important

Open banking made APIs much more visible in finance.

Instead of keeping all account and payment activity locked inside one institution, open banking(finteconomix-open banking information) created controlled ways for licensed or approved third parties to access financial data or initiate certain actions with customer consent.

That is a huge shift.

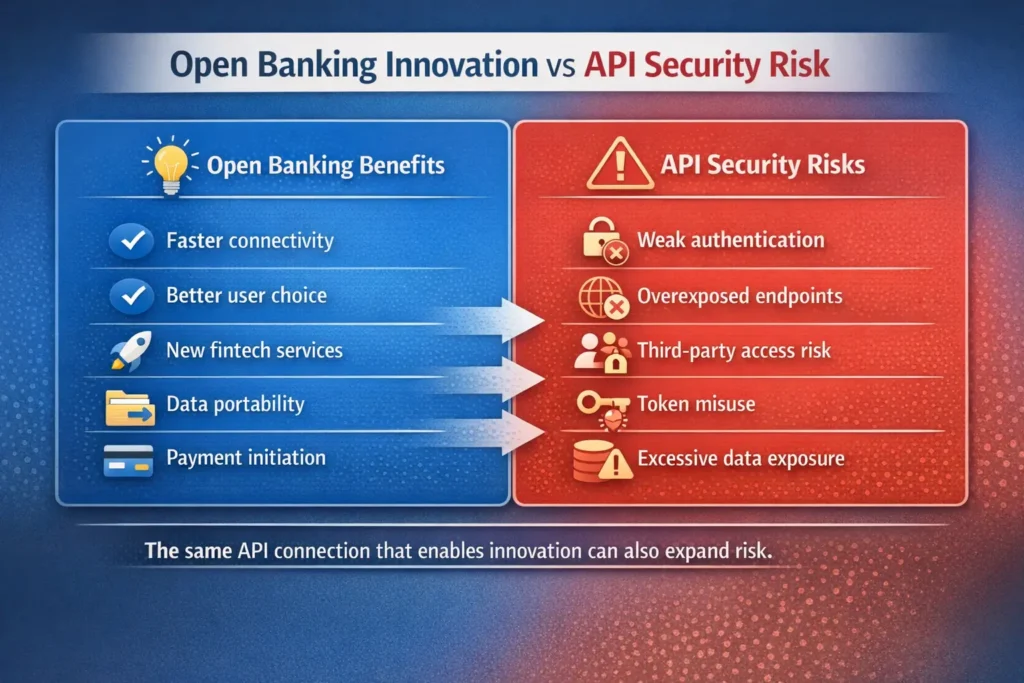

It creates innovation. It improves competition. It gives users more flexibility. But it also means that API security is no longer a background engineering issue. It becomes part of how trust is designed.

When people ask whether open banking is safe, they are really asking whether these API connections are strongly protected, whether consent is handled properly, and whether third-party access stays within the right limits.

That is why open banking security matters so much in fintech. Once multiple parties are connected, the risk is no longer only about one app or one bank. It is about the full chain of access.

The biggest API security risks in fintech

API security sounds abstract until you break it into real risks.

In fintech, the biggest problems often include:

- weak authentication between systems

- overexposed endpoints

- poor access control

- stolen or misused tokens

- insecure third-party integrations

- excessive data exposure

- weak monitoring of unusual API activity

A single issue may not look dramatic at first. But that is how many real problems begin.

An API may expose more data than necessary.

A third-party service may keep access longer than it should.

A token may be reused in a way nobody expected.

A normal-looking request may become dangerous when repeated at scale.

This is why API security in fintech is not just about blocking bad traffic. It is about controlling trust at every connection point.

API security is also a third-party risk problem

This is where fintech gets especially interesting.

Many fintech companies do not build every service themselves. They depend on cloud vendors, identity providers, payment processors, fraud tools, banking partners, and data aggregators. That means their real risk is not only inside their own code. It also lives in the way they connect to outside systems.

That is why platform risk matters.

A fintech company may have a well-designed app and still face serious exposure if:

- an outside provider has weak controls

- access permissions are too broad

- monitoring stops at the company boundary

- shared credentials or tokens are poorly protected

- a connected partner becomes the weak link

So API security is also about ecosystem security. In fintech, one weak connection can create problems across many connected services.

Why authentication and authorization matter so much

This is one of the easiest places for beginners to get confused.

Authentication and authorization are related, but they are not the same thing.

- Authentication asks: who are you?

- Authorization asks: what are you allowed to do?

In fintech APIs, both matter.

A system may confirm that a third party is legitimate, but that does not mean it should access every account field, every payment function, or every user record. Good API security is not only about letting the right party in. It is about limiting that party to the right scope.

This is especially important in open banking and platform finance, where access often depends on consent, scope, timing, and purpose. A secure connection is not enough if the permissions behind it are too broad.

Good API security is not just about secrecy

A lot of people assume API security is mainly about hiding things.

That is only part of the story.

Good fintech API security is also about:

- reducing unnecessary exposure

- creating strong identity for systems and clients

- enforcing least-privilege access

- logging and monitoring behavior

- detecting misuse quickly

- keeping services resilient when traffic or attacks change

That last part matters a lot.

In fintech, an API problem can also become a service reliability problem. If an important API slows down, fails, or is abused, the result may look like an outage to the customer. Payments may fail. Account data may not load. Risk checks may break. Support demand may rise immediately.

So API security and operational resilience are closely connected.

What strong API security looks like in fintech

The strongest fintech companies do not treat API security like a checklist they complete once.

They treat it like a living control system.

In practice, strong API security usually means:

- clear identity for every connecting client

- secure token and credential handling

- limited and well-defined scopes

- encrypted communication

- rate limits and abuse controls

- logging, alerting, and anomaly detection

- regular review of third-party access

- security decisions built into design, not added at the end

That is what makes API security in fintech different from “just protect the backend.”

It is not only about technical defense. It is about designing safe connectivity from the beginning.

Why this matters for trust

Most users will never say, “I love this fintech because its API authorization model is well designed.”

But they absolutely notice the results of weak API security.

They notice when linked accounts feel risky.

They notice when app connections fail at critical moments.

They notice when data sharing feels unclear or overly broad.

They notice when trust breaks.

That is why API security matters beyond engineering teams.

It affects:

- user trust

- partner trust

- regulatory confidence

- platform reliability

- long-term product credibility

In digital finance, secure connections are part of the product experience, even if users never see the technical layer directly.

The real takeaway

API security in fintech is not just a backend concern.

It is one of the main reasons modern digital finance works at all.

Fintech depends on connections. Open banking depends on connections. Platform finance depends on connections. And once financial services depend on connected systems, API security becomes a core part of trust.

That is why API security is about more than protecting one endpoint. It is about protecting identity, permissions, data, resilience, and platform relationships across the full financial journey.

In fintech, the connection is the product.

And in many cases, the connection is also the risk.

References

NIST, Guidelines for API Protection for Cloud-Native Systems

Open Banking Limited, Getting Started – OBL API Security Profile