Why payment orchestration matters for global ecommerce, fintech, and digital growth

payment orchestration, what is payment orchestration, payment orchestration explained, payment infrastructure, checkout optimization, intelligent payment routing, global payments, payment gateway vs payment orchestration

If you sell online, you are not really in the business of “accepting payments.”

You are in the business of getting payments to actually go through.

That sounds obvious, but it changes everything.

Most brands obsess over ads, landing pages, pricing, and conversion funnels. Then they treat payments like the boring part at the end. Add a gateway. Connect a processor. Turn on wallets. Done.

Not done.

Because the real fight starts after the customer clicks Pay.

Will the transaction be routed through the right provider?

Will a soft decline be retried intelligently?

Will a customer in Brazil see the payment method they trust?

Will a customer in Europe hit too much authentication friction?

Will a recurring payment fail for no good reason next month?

Will one provider outage quietly kill revenue for an hour before anyone notices?

That is the world of payment orchestration.

And if you run a fast-growing ecommerce brand, SaaS company, marketplace, travel platform, subscription business, or fintech product, payment orchestration is no longer some niche infrastructure topic for payments nerds. It is becoming one of the clearest competitive advantages in digital commerce.

Stripe defines payment orchestration as the centralization of gateways, processors, acquirers, and other financial service providers into a single platform, while its newer routing materials describe the orchestration layer as the piece that connects a business to multiple processors and enables dynamic routing instead of locking everything into one provider. (Stripe)

What is payment orchestration?

At the simplest level, payment orchestration is the control layer that helps a business manage multiple payment providers, methods, and flows from one place.

Instead of building your entire checkout and payment stack around a single processor or gateway, orchestration lets you operate with more flexibility.

Think of it like this:

A payment gateway is a road.

A payment processor is a vehicle moving the transaction.

An acquirer is part of the financial path that gets the payment authorized and settled.

Payment orchestration is the traffic control system.

It decides how traffic moves.

It can help determine:

- which provider should handle a transaction

- which payment methods should appear in which market

- what to do when a payment fails

- when to trigger routing rules

- how to monitor performance across providers

- how to reduce dependency on one vendor

- how to unify reporting and visibility across a fragmented stack

That is why payment orchestration is not just a technical add-on. It is an operating model.

Why this matters now

Ten years ago, a lot of online businesses could get surprisingly far with a relatively simple setup. One processor. A few card networks. Maybe PayPal. Maybe Apple Pay later.

That world is gone.

Digital payments are more global, more fragmented, more local, and more strategic than they used to be. Worldpay’s 2025 payments insights emphasize that digital payments now dominate online commerce globally, with digital wallets playing an increasingly central role across markets, and that the mix of preferred payment methods differs sharply by region. That matters because it means there is no longer one “normal” checkout for a global business. (worldpay)

In plain English:

what works in the US will not always work in Germany, Brazil, India, or Singapore.

And even inside the same country, what works for a subscription app may not work for travel, marketplaces, gaming, luxury ecommerce, or B2B SaaS.

That is why payment orchestration is rising in relevance. Modern payment complexity is no longer an edge case. It is the default.

The real job of payment orchestration

A lot of articles make payment orchestration sound abstract. It is not abstract at all. It is very practical.

Its job is to help businesses answer one brutally important question:

How do we make checkout perform better without rebuilding our payments stack every time the business changes?

That breaks down into a few big jobs.

1. Smarter routing

Not every transaction should travel the same path.

One provider may perform better for certain card types. Another may be stronger in a specific geography. Another might offer better economics for certain payment methods or ticket sizes.

Payment orchestration makes it possible to route payments based on business logic instead of sending everything down one lane.

That does not just matter for engineers. It matters for revenue.

2. Better resilience

Provider outages happen. Regional slowdowns happen. Unexpected decline spikes happen.

If you only rely on one core payments provider, your checkout experience can become fragile very quickly. A problem on their side becomes a problem on your side.

An orchestration layer can reduce that fragility by giving businesses more optionality and more ways to fail gracefully instead of failing completely.

3. Global payment method flexibility

Consumers do not all want to pay the same way.

Some markets are wallet-heavy. Some are still strongly card-driven. Some have powerful account-to-account rails. Some have locally dominant payment methods that matter far more than outsiders expect.

A checkout that feels natural in one region can feel weird, incomplete, or low-trust somewhere else.

Payment orchestration helps businesses adapt without turning every country launch into a custom engineering project from scratch.

4. Lower friction, not just more payments

There is a huge difference between “offering more payment methods” and “creating less payment friction.”

The first one is easy to talk about. The second one actually makes money.

A checkout can technically support lots of options and still perform badly if the routing is weak, the ordering is wrong, the fallback logic is missing, or the authentication flow creates too much drag.

Orchestration matters because it is not just about breadth. It is about control.

5. Better visibility

One of the messiest realities in payments is that performance data often gets trapped in separate systems.

Different PSP dashboards. Different processor reports. Different decline codes. Different finance exports. Different support explanations.

That makes it hard to answer simple but important questions:

- Why is authorization down in this market?

- Which provider is underperforming?

- Are retries helping or hurting?

- Which payment methods actually improve conversion?

- What is the tradeoff between cost and authorization here?

Payment orchestration is valuable partly because it can make the stack easier to understand.

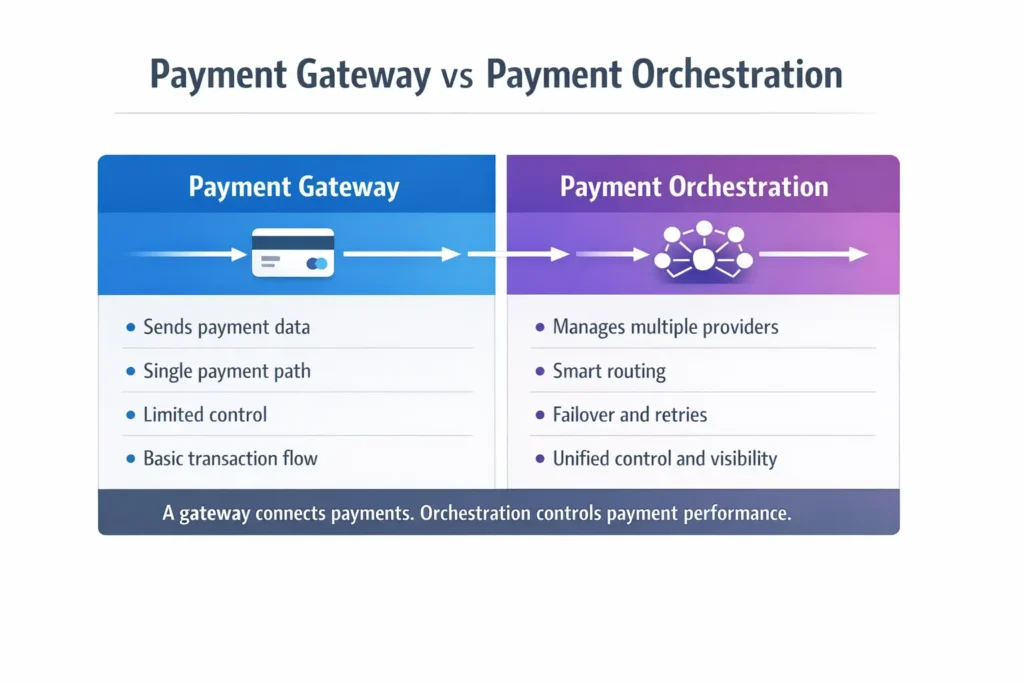

Payment orchestration vs payment gateway

This is one of the most searched comparisons around the topic, and for good reason.

Many people first hear about orchestration and assume it is basically the same thing as a gateway. It is not.

Here is the simple version:

| Category | Payment gateway | Payment orchestration |

|---|---|---|

| Core role | Connects and transmits payment data | Manages, routes, and optimizes payment flows |

| Scope | Usually one payment path or one provider environment | Multiple providers, methods, and rules |

| Focus | Transaction enablement | Payment performance and operational control |

| Retry/failover logic | Limited | Much stronger potential |

| Multi-provider visibility | Usually fragmented | Can be centralized |

| Strategic value | Functional | Operational and commercial |

A gateway helps process the payment.

An orchestration layer helps decide how that payment should be handled.

That distinction matters.

Because if your business is small and simple, a gateway might be enough.

If your business is growing across markets, methods, providers, and product lines, orchestration starts becoming far more relevant.

Why US digital brands should care

A lot of US brands still underestimate how much checkout quality shapes customer perception.

The customer does not think in terms of processors, routing layers, or acquirer performance. They think in terms of vibes.

- Why did my card fail?

- Why is this checkout weird?

- Why is this asking for so much?

- Why can’t I use the payment method I expected?

- Why did my renewal break?

- Why is getting my refund taking forever?

To the customer, these are not infrastructure questions.

They are trust questions.

That is especially important for younger consumers, who are extremely comfortable abandoning a purchase, switching apps, or trying a competitor. If the checkout feels clunky, slow, unreliable, or oddly outdated, they do not sit around diagnosing the architecture. They leave.

That is what makes payment orchestration interesting from a brand perspective. It is backend infrastructure that directly shapes frontend trust.

In other words:

checkout is not just UX anymore. It is revenue infrastructure.

Where payment orchestration matters most

Not every business has the same need. But some categories feel the impact earlier and harder.

Ecommerce

Fast-growing ecommerce brands hit payment complexity sooner than they expect.

At first, one provider may be enough. Then the brand expands internationally, adds wallets, adds subscriptions, experiments with local methods, enters new regions, and starts seeing weird approval patterns that nobody can fully explain.

That is usually when the payment stack starts feeling less like a feature and more like a system that needs strategy.

Subscription businesses

Subscription companies do not just care about first-time conversion. They care about recurring success.

A failed renewal is not always a lost customer for product reasons. Sometimes it is just a preventable payment issue.

That makes orchestration especially relevant when recurring billing becomes important to revenue retention.

Travel

Travel is one of the clearest orchestration use cases because it is naturally complex.

Higher ticket sizes. International customers. Different currencies. More declines. More cancellations. More refund sensitivity. More pressure on every checkout moment.

A fragile payment stack becomes expensive very quickly in travel.

Marketplaces and platforms

Marketplaces often deal with even more moving parts: different seller flows, disbursements, refunds, cross-border complexity, and operational reporting needs.

The more layers the business model has, the more valuable payment control becomes.

The hidden business case

The strongest argument for payment orchestration is not that it sounds modern. It is that it can change the economics of checkout.

Businesses often talk about payments as a cost center. Fees. fraud. chargebacks. payment ops. support complexity.

But high-performing businesses increasingly see payments as a growth lever.

Why?

Because even small improvements can compound.

A small lift in authorization can mean a major revenue gain at scale.

A better retry strategy can recover transactions that would otherwise disappear.

A more locally relevant checkout can improve conversion in new markets.

A more resilient setup can reduce the damage of outages.

A more unified data layer can improve decision-making across product, finance, and operations.

None of that is flashy.

It is just extremely valuable.

That is part of why Primer argues that orchestration can increase flexibility, reduce costs, and improve performance, while also warning that some approaches can create new complexity or a new kind of vendor dependency if businesses are not thoughtful about how they implement it. (Primer)

When a company may not need it yet

To be clear, not every business should rush into payment orchestration tomorrow.

If you are operating in one market, with low complexity, low transaction volume, a small set of payment methods, and no major provider issues, a simpler setup may still be the right move.

Sometimes the smartest decision is not adding another layer too early.

But the case gets stronger when several of these are true:

| Signal | Why it matters |

|---|---|

| You sell in multiple markets | Payment preferences and provider performance vary |

| You rely heavily on one provider | Outage and concentration risk increase |

| You care about authorization trends | Routing and visibility become more important |

| You need local payment methods | Single-stack setups often become restrictive |

| Your payment data is fragmented | Decision-making gets harder |

| You run subscriptions or renewals | Payment performance affects retention |

| Checkout issues directly hit revenue | Infrastructure quality becomes strategic |

If that list feels familiar, orchestration is probably no longer a “nice to have” topic.

Final thoughts

The future of digital commerce is not about adding endless payment methods and hoping for the best.

It is about building a checkout system that is flexible, resilient, locally relevant, and commercially intelligent.

That is what payment orchestration is really about.

Not making payments look more complicated.

Making complicated payments feel simple.

Customers will never say, “Wow, amazing orchestration layer.”

They will just notice that checkout worked, the payment method felt right, the renewal did not fail, and the brand felt trustworthy.

That is the point.

The best payment infrastructure is usually invisible.

And in modern fintech and ecommerce, payment orchestration is becoming one of the most important invisible layers in the stack.

References

Stripe — What is payment orchestration? and related orchestration/routing documentation:

https://stripe.com/resources/more/what-is-payment-orchestration-what-businesses-need-to-know

https://stripe.com/resources/more/intelligent-payment-routing

https://docs.stripe.com/payments/orchestration

Worldpay — Global Payments Report and 2025 payment trends overview:

https://www.worldpay.com/en/global-payments-report

https://www.worldpay.com/en/insights/articles/digital-payments-GPR-guide

Primer — Payment orchestrator tradeoffs and gateway comparison:

https://primer.io/blog/pros-and-cons-of-working-with-a-payment-orchestrator

https://primer.io/blog/payment-orchestration-vs-payment-gateway