In a country where cards are strong, online checkout tells a different story

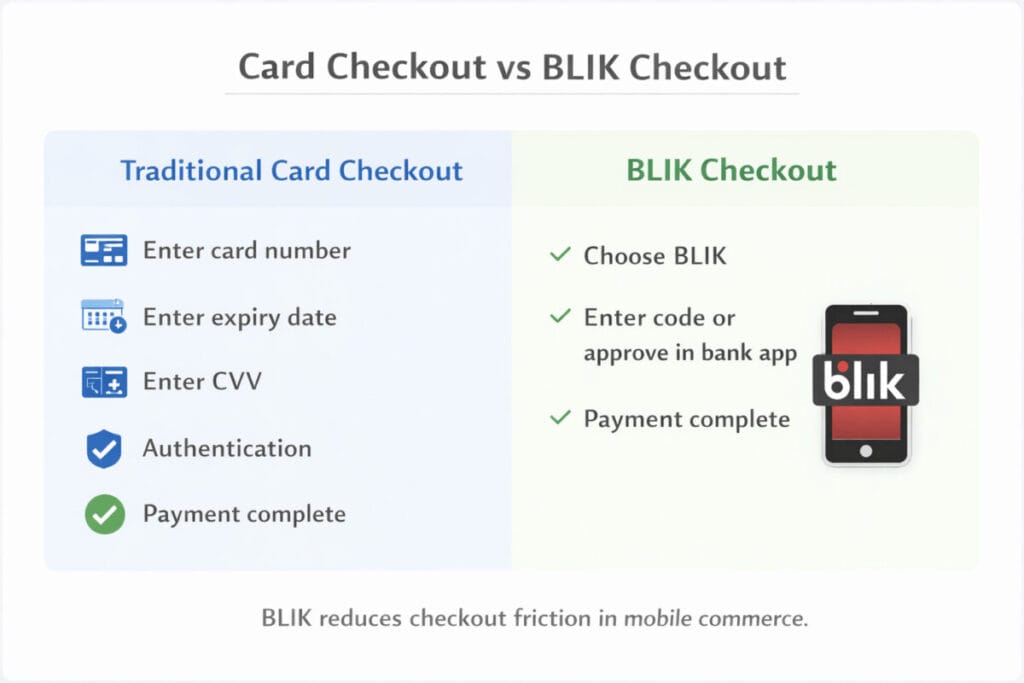

When people think about online payments, they usually think about cards first. That makes sense. Card checkout has been the default flow in e-commerce for years: enter the card number, add the expiry date, type the security code, pass authentication, and complete the purchase.

Poland is not a weak card market. In fact, it is one of the world’s most contactless-friendly payment markets. At the end of 2023, contactless cards accounted for 97.2% of all payment cards in Poland. That matters, because it means BLIK did not rise simply because cards failed. It rose in a market where cards were already strong.

And yet, online, many Polish shoppers do not behave as outsiders might expect. In e-commerce, BLIK is not just an alternative payment option anymore. It has become one of the most natural ways to pay.

BLIK is no longer a niche method in Polish e-commerce

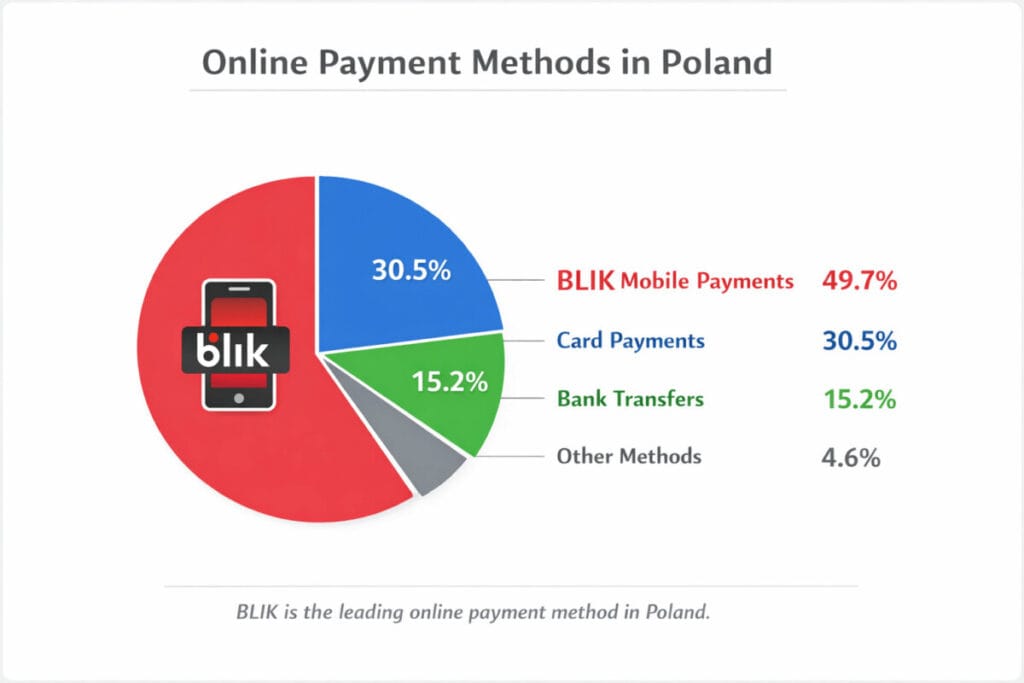

The scale is too large to dismiss as a local quirk. In 2025, BLIK users completed 2.9 billion transactions worth PLN 441.5 billion, and the company said e-commerce remained its strongest channel. That alone tells you BLIK is not a side story in Polish payments. It is one of the main stories.

The more revealing number comes from the National Bank of Poland. In remote transactions, primarily e-commerce, non-card mobile payments in the BLIK system accounted for 49.7% of transaction volume and 44.9% of transaction value in the central bank’s assessment. In other words, BLIK is not merely popular online in Poland. It is central to how online payments already work.

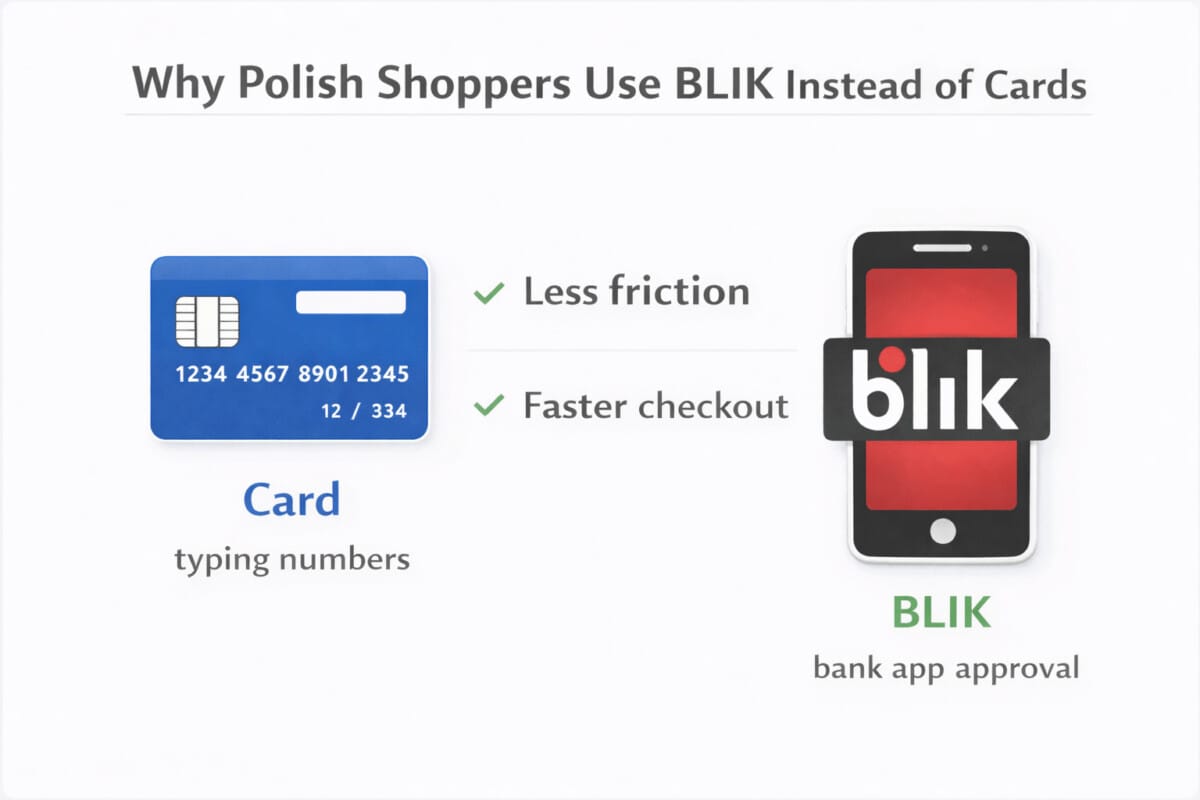

The real competition is not cards versus BLIK

The real competition is friction versus convenience.

That is the most useful way to understand why Polish shoppers often choose BLIK instead of cards for online payments. Card checkout is familiar, but familiarity does not always mean low friction. On a phone, especially, card payments can still feel like work. You type the number. You check the date. You add the CVV. You wait for authentication. You bounce between screens. One small interruption does not matter much on its own, but several small interruptions can make checkout feel slower than it should.

BLIK changed that equation by fitting payments into a place Polish consumers were already visiting every day: their banking app. Instead of repeatedly entering card details into merchant checkouts, users can often approve a payment in a flow that feels shorter, more direct, and more familiar.

That difference sounds small. In practice, it is huge.

Why BLIK feels better online

1. It reduces checkout friction

The biggest advantage of BLIK is not that it looks futuristic. It is that it removes steps shoppers do not enjoy. Fewer fields, less repeated data entry, and a cleaner mobile experience can make a payment feel easier even when the underlying process remains secure.

2. It keeps trust inside the banking app

For many users, the most comfortable place to approve a payment is not a merchant page but their own bank’s mobile app. BLIK benefits from that instinct. It feels closer to “I am confirming this in my bank” than “I am handing over my card details again.”

3. It matches how people already bank

BLIK works because it is not asking users to learn a completely new behavior. It piggybacks on an existing habit: opening a banking app. In payments, that matters more than novelty. The methods that win are often the ones that ask for the smallest behavioral change.

4. It is already part of everyday life

A payment method becomes powerful when people stop thinking about it as a payment method. That is where BLIK seems to be in Poland. It is used not just online, but across other contexts too, which reinforces familiarity and makes it feel normal at checkout.

BLIK vs cards in Polish online payments

| Factor | Card payments | BLIK |

|---|---|---|

| Checkout flow | Often requires manual card entry and authentication | Often feels shorter and more direct |

| Mobile experience | Can involve multiple input steps | Designed around banking-app usage |

| User comfort | Familiar, but can feel repetitive | Familiar through daily bank-app behavior |

| Trust perception | Depends on merchant checkout flow | Often feels anchored in the bank relationship |

| Position in Polish e-commerce | Still important | Already a leading remote payment method |

This is why “BLIK vs cards in Poland” is not really a story about one method replacing another across the board. It is a story about one method being better aligned with online behavior.

Cards are not losing everywhere

This point is important.

The Polish story is not that cards have become irrelevant. Far from it. Cards remain deeply embedded in the country’s payment landscape, especially in physical retail. What makes Poland interesting is that online payments follow a different logic. The winner in e-commerce is not automatically the same as the winner in stores.

That distinction matters far beyond Poland. It suggests that in modern payments, the most successful method is not necessarily the most established one. It is often the one that best fits the context of use.

What the Polish market gets right

Poland shows something many payment discussions miss: users do not choose the most impressive payment technology. They choose the one that gets out of the way fastest.

That is why BLIK matters. It is not simply a local brand success story. It is an example of how a payment method can win by solving a boring but important problem: reducing friction at checkout.

For merchants, that means payment choice is not just a technical integration issue. It is part of conversion. For fintechs, it is a reminder that owning the user interface matters. For the rest of Europe, it is a case study in how local payment infrastructure can shape consumer habits in ways global assumptions often miss.

If you want to understand the Polish payments market, start here: not with the question of whether cards are strong, but with the question of why online shoppers still prefer something else.

Final thought

BLIK did not become powerful in Polish e-commerce because cards were weak. It became powerful because online checkout punishes friction, and BLIK often feels like the smoother path.

That is the real reason many Polish shoppers use BLIK instead of cards for online payments.

In the end, the most successful payment method is rarely the one that feels the most innovative. It is the one that feels the least annoying.

References and Further Reading

If you want to understand how BLIK became one of the most widely used online payment methods in Poland, the following resources provide useful data and background.

- BLIK official website – payment features and ecosystem

https://blik.com/en - National Bank of Poland – payment system statistics

https://www.nbp.pl - European Central Bank – payment trends in Europe

https://www.ecb.europa.eu/paym - Polish Bank Association – digital banking and payment adoption

https://www.zbp.pl - McKinsey – global digital payments insights

https://www.mckinsey.com/industries/financial-services/our-insights/payments

These reports show that the growth of solutions like BLIK is not only a Polish phenomenon but part of a broader shift toward faster and more seamless digital payment experiences.