Why a won stablecoin could reshape fees, settlement, and power in Korea’s payment market

A won-denominated stablecoin is no longer just a crypto topic. In South Korea, it is becoming a payments story, a regulatory story, and potentially a card-industry story. That is what makes the issue so interesting. Korea already has one of the most advanced digital payment markets in the world. Card payments are deeply embedded in daily life, mobile payment apps are widely used, and consumers are used to fast and convenient digital transactions. In other words, a won stablecoin would not be entering a weak or underdeveloped payment market. It would be entering a mature payment economy and challenging the existing structure from inside.

That is exactly why this topic matters.

Most stablecoin discussions focus on cross-border remittances, crypto trading, or financial inclusion in less developed markets. Korea raises a very different question. What happens when a stablecoin tries to compete in a country where consumers already have convenient cards, familiar apps, and dense merchant acceptance? In that kind of market, the key issue is not whether payments will become digital. They already are. The key issue is whether a won stablecoin could change who controls payments, who earns fees, who owns the customer relationship, and who sits at the center of settlement.

Why Korea’s card industry is vulnerable to this debate

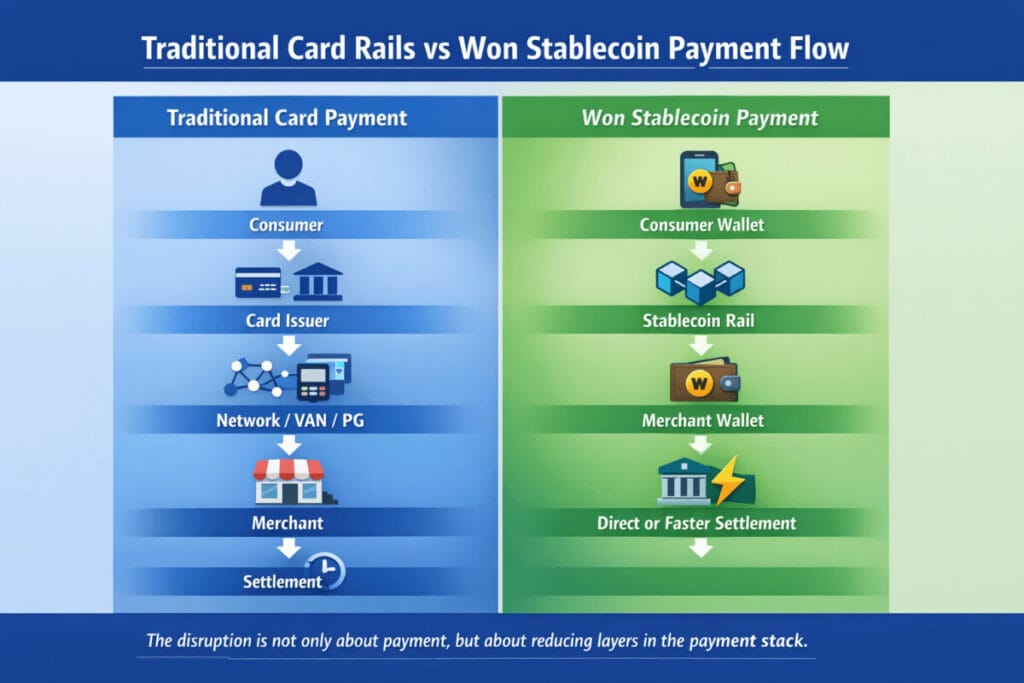

Korea’s card industry has long benefited from a layered payment structure. Consumers use credit cards, debit cards, and mobile-linked card services through familiar brands. Merchants accept those payments through established acquiring and processing systems. Card issuers, merchant acquirers, VAN firms, PG firms, banks, and large platforms all play a role in the payment chain. This structure does far more than move money. It also determines who collects fees, who manages risk, who handles disputes, and who owns transaction data.

That is why the idea of a won stablecoin matters so much.

If a won stablecoin becomes usable in real retail payments, even in limited categories, it could begin to challenge parts of this chain. The biggest impact may not come from consumers suddenly abandoning cards. It may come from the market asking whether every current intermediary is still necessary. Once that question appears, the business model of the card industry starts to face pressure.

How a won stablecoin could pressure card fees

The first major pressure point is fees.

Traditional card payments involve multiple intermediaries, and each layer can add cost. Even when the consumer experience looks simple, the economics behind the transaction are not frictionless. Merchant fees, processing arrangements, settlement timing, and backend infrastructure all shape the final cost of card payments.

If a won stablecoin allows some transactions to move through a wallet-based or token-based model with a shorter chain, merchants will inevitably ask a basic question: why should we continue paying today’s card-related costs for every transaction?

That does not mean stablecoin payments would be free. They would still require compliance systems, wallet operations, fraud controls, customer support, and dispute-handling mechanisms. But the mere existence of an alternative payment rail could put new pressure on existing fee structures. In payments, cost pressure alone can be disruptive even before mass consumer adoption arrives.

This is why a won stablecoin matters to Korea’s card industry. It is not only about whether stablecoins replace cards. It is also about whether they weaken the pricing power of card-based payments.

How a won stablecoin could change settlement

The second major pressure point is settlement.

Card payments feel immediate to consumers, but the backend process is more complex than the front-end experience suggests. Settlement still relies on layered institutional arrangements, established business relationships, and operational rules. One reason card networks remain powerful is that they do not simply enable payment. They organize a settlement. They help define when money moves, who takes temporary exposure, and how failed or disputed transactions are resolved.

A won stablecoin could begin to change that logic.

If tokenized won-based payments allow settlement to become more direct, faster, or more programmable, some of the traditional advantages of existing card structures may weaken. This does not mean the old system disappears overnight. It means the market starts to imagine a payment architecture in which some transactions no longer need to move through the same settlement path as before.

That possibility matters in Korea because policy and industry discussions around digital money are no longer purely theoretical. They are increasingly connected to real experiments involving digital currency infrastructure, deposit-token models, and retail payment use cases. Once the market begins to accept the idea that money itself can move in a more programmable and direct way, the value of legacy settlement layers comes under review.

So the real disruption may not be visible at the checkout screen. It may happen deeper in the stack, in the way transactions are settled and controlled behind the scenes.

Why platforms and wallets could become more powerful

The third pressure point is platform power.

The card industry has traditionally been strong because it controls important payment relationships: card issuance, merchant acceptance, brand trust, loyalty systems, and consumer familiarity. But if a won stablecoin is distributed through digital wallets, super apps, or platform ecosystems, the center of gravity could begin to shift.

In that world, the most valuable player may no longer be the company that issues the card. It may be the company that controls the wallet, the app interface, the user identity layer, the merchant relationship, or the embedded payment environment.

This is a critical change.

For years, payment power often sat with the institution that issued the payment instrument. In a more wallet-centered future, power could move toward the institution that owns the consumer interface. That shift would matter enormously in Korea, where platform ecosystems are already strong and where consumers are comfortable making payments inside apps rather than thinking in terms of a physical card.

That is why a won stablecoin is not just a money question. It is also a platform question.

Why the card industry will not collapse overnight

Still, it would be a mistake to assume that a won stablecoin would quickly destroy Korea’s card industry.

Incumbent payment systems are rarely defenseless. Korea’s card sector still has several powerful advantages that are difficult to replicate quickly.

First, merchant acceptance is already broad and deeply embedded in everyday commerce.

Second, the card industry has long experience with refunds, chargebacks, dispute handling, and consumer protection.

Third, consumers trust card-based systems because they understand how they work and know what protections they can expect.

Fourth, regulatory familiarity still matters. Stablecoin-based retail payments may look efficient in theory, but mass adoption in a country like Korea will depend heavily on trust, legal clarity, and operational reliability.

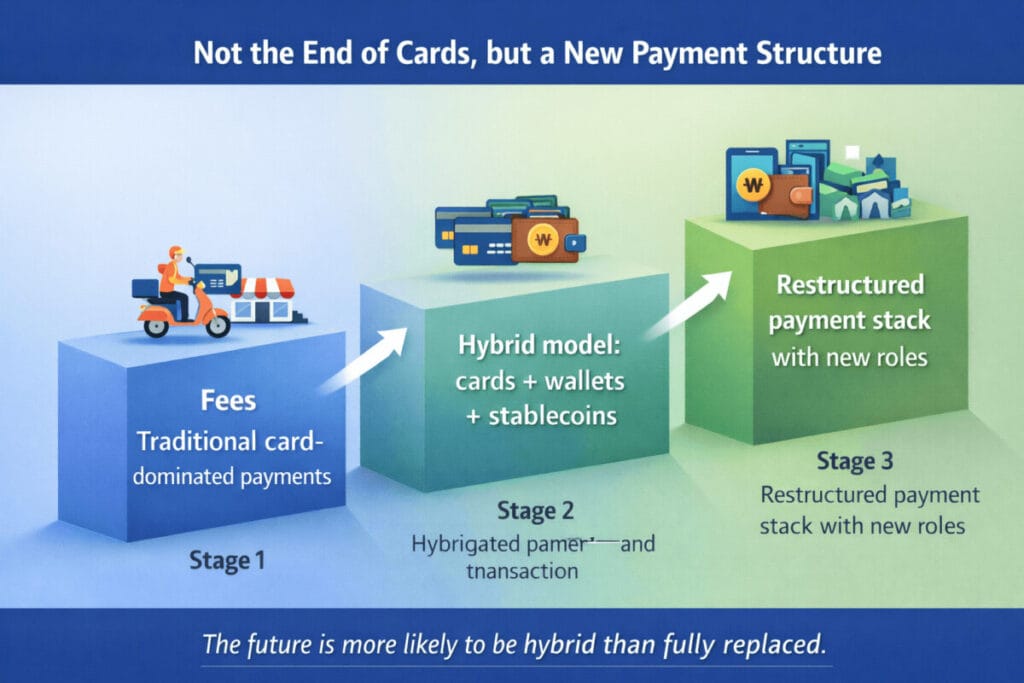

For those reasons, the most realistic scenario is not immediate replacement. It is gradual restructuring.

A won stablecoin may not remove cards from Korean commerce. But it could force the card industry to justify why its current role, costs, and position in the payment chain should remain unchanged.

The likely outcome: not replacement, but restructuring

The most realistic outcome is not that Won stablecoins will completely replace card payments. It is that they reshape the market.

Card companies could respond in several ways. Some may resist through regulation and industry lobbying. Some may adapt by integrating stablecoin-related services into existing payment products. Others may try to position themselves as infrastructure providers within a tokenized payment environment. In that case, the question would no longer be whether card companies survive, but what role they play in a changed payment system.

That distinction matters.

Disruption in payments does not always mean outsiders destroy incumbents. Sometimes incumbents absorb part of the new model and preserve their relevance. Korea’s card industry could follow that path. A card company might lose some pricing power in one area while gaining a new role in wallet-linked settlement, international payment products, or compliant stablecoin-based consumer services.

In that sense, a won stablecoin may not mean the end of Korea’s card industry. It may mean the beginning of a new competitive phase.

Comparison table: traditional card payments vs a won stablecoin model

| Category | Traditional Card Payment Model | Potential Won Stablecoin Model |

|---|---|---|

| Payment center | Card issuer and existing network | Wallet, platform, or token-based rail |

| Revenue source | Merchant fees, network position, card economics | Wallet fees, settlement services, platform control |

| Settlement structure | Layered and institution-heavy | Potentially shorter and more direct |

| Consumer experience | Familiar, trusted, stable | Newer, potentially seamless through apps |

| Core strength | Merchant reach, consumer protection, dispute handling | Lower-cost pressure, programmability, new design flexibility |

| Core weakness | Fee pressure and legacy complexity | Merchant fees, network position, and card economics |

This table shows why the issue matters. A won stablecoin is not just another payment method. It represents a possible reordering of the payment stack.

Final thoughts

So how could a won stablecoin disrupt Korea’s card industry?

Not by making cards disappear tomorrow.

Not by instantly replacing familiar consumer habits.

And not by magically removing every intermediary from the payment process.

The real disruption is more subtle and more important than that.

A won stablecoin could pressure card fees.

It could challenge the logic of existing settlement structures.

It could strengthen wallets and platforms.

It could force card companies to redefine their role in a payment market that becomes more tokenized, more programmable, and less dependent on the traditional structure that made them powerful.

That is why this is not a narrow crypto issue. It is a broader payment-industry question.

In Korea, the future of the card industry may not depend only on whether consumers keep tapping cards. It may depend on who controls what happens behind the tap.