Why It Could Reshape Payments in 2026

AI is starting to move beyond recommendations.

For years, most discussions about AI in payments focused on fraud detection, customer support, or back-office automation. That is still important, but a new question is becoming more interesting:

What happens when AI does not just help you decide what to buy, but also helps complete the purchase?

That is where agentic commerce comes in.

Agentic commerce describes a model where AI agents do more than assist with search. They can help users compare options, follow preferences, and move through parts of the buying process with some level of permission. In simple terms, commerce is shifting from human-only checkout toward human-directed, AI-assisted execution.

This matters because payments were built around a basic assumption: the person choosing the product is also the person clicking the final button. Agentic commerce challenges that assumption.

Why Agentic Commerce Matters Now

The reason this topic matters in 2026 is not just hype. It is about how the role of AI is changing.

A few years ago, AI mostly sat behind the scenes. It ranked products, flagged risky transactions, or answered support questions. Now, AI is starting to appear closer to the front end of commerce. A user may soon say:

Find me a hotel in Manhattan under $300 for next Tuesday and book the best option.

That sounds simple, but it changes the structure of payments.

The user is no longer handling every step directly. The AI agent may search, compare, narrow options, and potentially move toward checkout based on pre-set instructions. At that point, payments are no longer just about speed or convenience. They become a question of identity, delegated authority, and trust.

The Core Shift: From Checkout to Permissioned Action

Traditional e-commerce works like this:

- A person searches

- A person selects

- A person enters payment details

- A person confirms

Agentic commerce introduces a different pattern:

- A person sets goals or limits

- An AI agent searches and evaluates

- The system checks what the agent is allowed to do

- A transaction may proceed within those rules

- The result is reported back to the user

That is a major shift.

The center of gravity moves from manual action to authorized execution.

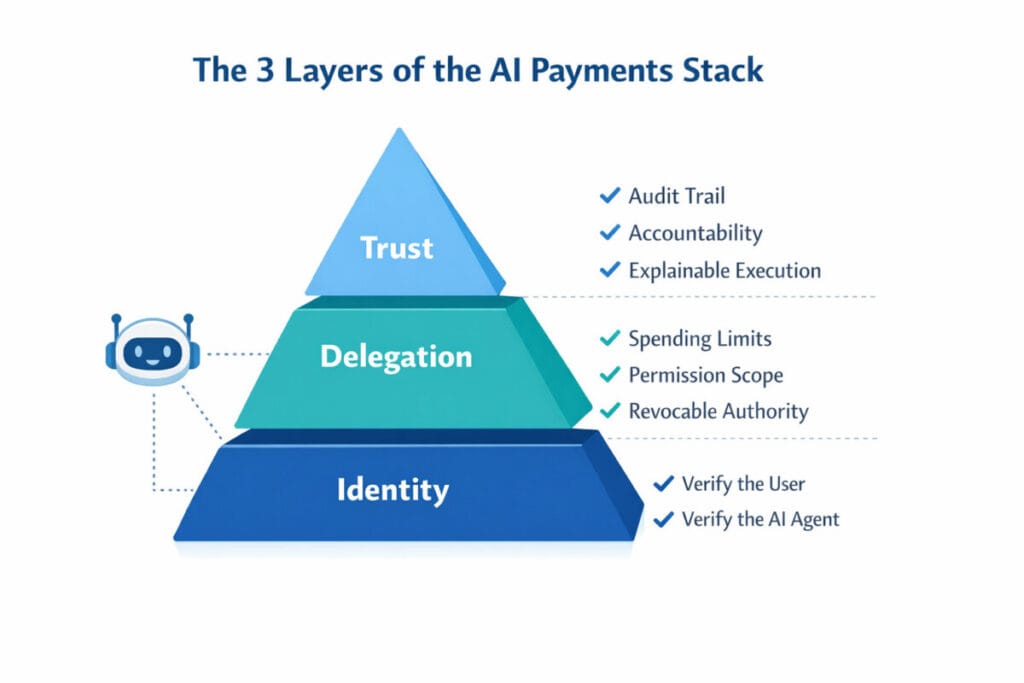

The 3 Layers the AI Payments Stack Will Need

1. Identity

The first issue is identity.

In traditional digital payments, the main question is whether the user is legitimate. In agentic commerce, that question expands:

Who is acting right now?

Is it the user directly?

Is it a trusted AI agent acting on the user’s behalf?

Is it a malicious bot pretending to be a legitimate assistant?

This is why future payment systems may need to verify not only the customer, but also the agent. Identity will no longer be just about account ownership. It may also need to cover digital actors operating with delegated authority.

2. Delegation

The second issue is delegation.

This is where agentic commerce becomes much more than a shopping tool. The real question is not whether AI can recommend products. The real question is:

What is the AI allowed to do?

Can it only suggest options?

Can it add items to a cart?

Can it buy within a certain spending limit?

Can it reorder approved products?

Can it cancel or refund?

These are not small interface decisions. They are payment design decisions.

In the next generation of commerce, users may need to define rules like:

- spending limits

- merchant restrictions

- category restrictions

- time-based permissions

- approval requirements

- revocable consent

That means future payment systems may need to support programmable delegation, not just one-click checkout.

3. Trust

The third issue is trust.

Even if identity and delegation are technically possible, the system still fails if nobody trusts it.

Users need confidence that AI will stay within its limits. Merchants need confidence that the request is legitimate. Payment providers need confidence that they can track, explain, and manage what happened if something goes wrong.

In this context, trust is not a branding concept. It is an infrastructure requirement.

Trust means the system should support:

- clear records of who initiated the action

- visible limits on what the AI was allowed to do

- auditable consent

- explainable payment flows

- dispute handling and accountability

Without trust, agentic commerce may look impressive in demos but struggle in real financial systems.

Traditional Commerce vs. Agentic Commerce

| Category | Traditional Commerce | Agentic Commerce |

|---|---|---|

| Main actor | Human user | Human user + AI agent |

| Payment trigger | Direct human action | Rule-based or delegated execution |

| Core question | Is this the real user? | Who is acting, and under whose authority? |

| Main risk | Fraud, stolen credentials | Overreach, unclear authority, responsibility gaps |

| Key infrastructure | Authentication, authorization, settlement | Authentication, delegation, verification, observability |

This is why agentic commerce should not be dismissed as just another AI shopping feature. It has the potential to reshape how payment authority is structured.

What This Means for Banks, PSPs, and Merchants

Banks

Banks may need to prepare for a world where the customer journey does not always begin inside a banking app. If AI interfaces become the first point of interaction, banks may play a bigger role as trusted infrastructure providers rather than front-end experience owners.

Payment Service Providers

For PSPs, this could create entirely new product categories. The next wave of payment infrastructure may include:

- agent verification

- delegated payment controls

- conditional authorization

- transaction observability

- accountability frameworks

In other words, the future opportunity may not be just better APIs. It may be better control layers for AI-driven transactions.

Merchants

For merchants, the big question is simple:

Can your product and checkout flow be understood and executed by AI agents?

If product data is messy, permissions are unclear, and checkout flows are too rigid, merchants may lose visibility in a future commerce environment where AI helps drive purchase decisions.

Why 2026 Could Be a Turning Point

2026 stands out because the conversation is changing from theory to infrastructure.

The market is moving beyond “AI can help commerce” toward “AI may become a transaction actor inside commerce.” That pushes payments into a new phase.

The old competition in payments was mostly about:

- speed

- conversion

- cost

- user experience

Those things still matter. But agentic commerce adds new competitive questions:

- Who can verify AI agents?

- Who can manage delegated authority safely?

- Who can make machine-assisted payments explainable and trustworthy?

That is why this topic matters now.

Final Take

Agentic commerce is not just a new shopping interface. It is a new coordination problem for payments.

Once AI starts participating in commerce more directly, payment systems can no longer rely on old assumptions. The immediate actor may not always be a human. Consent may need to become more structured. Authorization may need to become more programmable. Trust may need to be designed into the system from the start.

That is why the next payments stack may depend on three layers:

- Identity

- Delegation

- Trust

If agentic commerce really reshapes payments in 2026, it will not be because AI makes checkout look smarter.

It will be because payments learn how to handle who acts, who authorizes, and who is accountable in an AI-mediated world.

References