Risks, Regulation, and the Future of Digital Money

Stablecoins are no longer just a crypto market tool. They are now part of a bigger debate about digital money, cross-border payments, and the future of the global financial system.

To supporters, stablecoins look like a faster and more flexible way to move money. To many central banks, they look like a growing challenge to monetary sovereignty, financial stability, and regulatory control.

That is why the real question is no longer whether stablecoins matter. They already do.

The real question is this:

What happens when privately issued digital money becomes large enough to influence the public financial system?

This article explains why central banks are worried about stablecoins, why the market still supports them, and what the future of stablecoin regulation may look like.

What Are Stablecoins and Why Are They Growing So Fast?

Stablecoins are digital tokens designed to maintain a stable value, usually by being linked to a fiat currency such as the US dollar.

Their popularity comes from a simple promise: they are easier to use for payments and transfers than highly volatile crypto assets.

Supporters usually point to five main advantages:

- faster cross-border payments

- 24/7 availability

- easier use in blockchain-based markets

- support for programmable payments

- lower friction in digital asset settlement

This helps explain why the market has grown so quickly. Recent commentary has described stablecoins as large enough to raise real policy questions, not just niche crypto discussions.

Why Are Central Banks Concerned About Stablecoins?

For central banks, money is not just another tech product. It is part of a country’s core financial infrastructure.

That is why their concerns about stablecoins usually fall into three big areas:

- monetary sovereignty

- financial stability

- regulatory enforcement

1. Monetary Sovereignty: Who Controls Money?

One of the biggest central bank concerns is monetary sovereignty.

If privately issued, mostly dollar-linked stablecoins become widely used across borders, especially in countries with weaker local currencies, they can reduce the role of domestic money in payments and savings.

From a central bank perspective, that matters a lot. Monetary policy works best when the public still relies on the national currency and the domestic banking system. If users begin to prefer private digital dollars, policymakers may lose influence over how money moves through the economy.

In simple terms, central banks worry that private digital money could weaken public control over the monetary system.

2. Financial Stability: Could Stablecoins Pull Money Out of Banks?

The second major concern is financial stability.

In normal times, stablecoins may look like just another payment option. But in a crisis, people and businesses could move money out of banks and into instruments they believe are safer, faster, or easier to access.

That matters because bank deposits are a key part of the modern financial system. If large amounts of money move quickly out of deposits and into stablecoins, that could increase stress in funding markets and weaken the banking system’s stability.

This is why many central bankers do not see stablecoins as just a payments innovation. They also see them as a possible bank disintermediation risk.

3. Regulation and Compliance: Who Is Responsible?

The third concern is about regulation, AML/KYC, and accountability.

Traditional finance usually has clear institutions, clear rules, and clear lines of responsibility. Stablecoin ecosystems can be much more fragmented. There may be an issuer, exchanges, custodians, wallets, blockchain networks, and decentralized platforms all involved at the same time.

According to the BIS critique summarized in recent reporting, stablecoins fall short on three key tests for a modern monetary system: singleness, elasticity, and integrity.

In plain English, that means:

- not all stablecoins are equally trusted or equally accepted

- supply cannot always expand as flexibly as bank-created money

- compliance controls may be weaker in some parts of the ecosystem

For central banks, the key question is simple:

If stablecoins become more important, who guarantees trust, oversight, and final responsibility when something goes wrong?

Why Does the Market Still Support Stablecoins?

The market often sees the same issue very differently.

Instead of focusing first on control, private-sector supporters focus on efficiency, speed, and innovation.

From that point of view, stablecoins solve real problems:

- they can make cross-border payments faster

- they reduce friction in digital transfers

- they fit naturally into tokenized and on-chain markets

- they work well with smart contracts

- they can support new financial services

That is why many fintech and crypto players argue that stablecoins should not be treated only as a threat. Some policy commentary has also started to make a similar case, arguing that regulated stablecoins could complement traditional money instead of replacing it.

Central Banks vs Market View: A Simple Comparison

| Topic | Central Bank View | Market and Industry View |

|---|---|---|

| Main focus | Stability, sovereignty, control | Efficiency, speed, innovation |

| View of stablecoins | Potential systemic risk | Useful next-generation payment tool |

| Main concern | Deposit flight, weaker policy transmission, regulatory gaps | Overregulation, slower innovation, reduced competitiveness |

| Main opportunity | Publicly supervised digital money | Better global payments and on-chain settlement |

| Preferred solution | Stronger rules, CBDCs, supervised integration | Legal clarity, regulated growth, interoperability |

| Core question | “Will this weaken the financial system?” | “Will this improve how money moves?” |

This is why the debate often feels stuck. The two sides are not asking the same question.

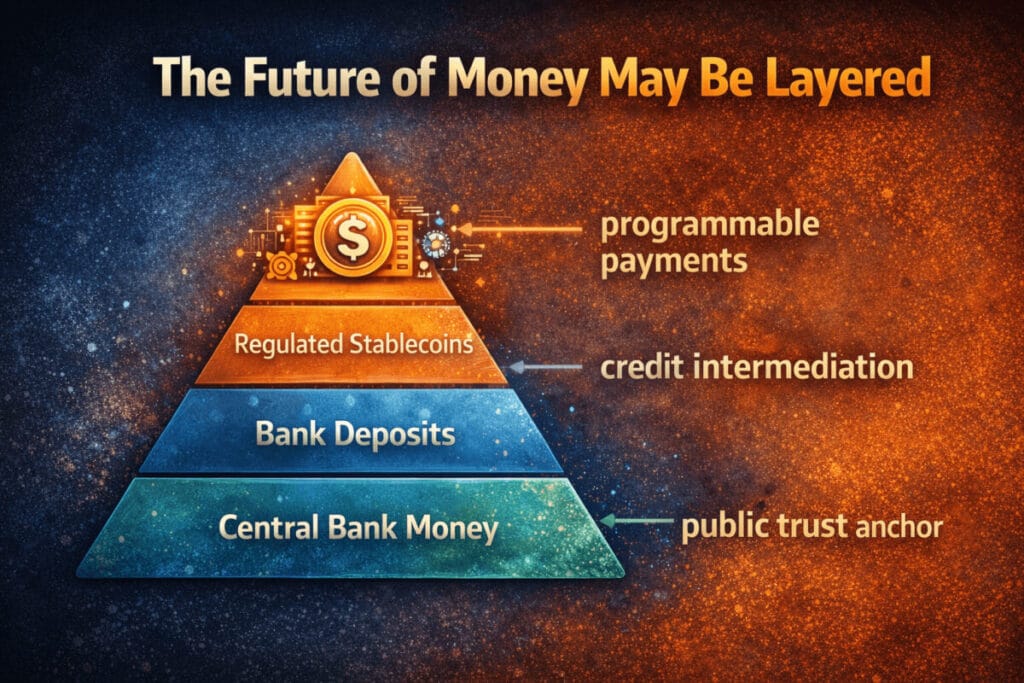

Is This Just a Fight Between Stablecoins and CBDCs?

Not really.

A lot of people frame the story as stablecoins vs CBDCs, but the more realistic future may be a system where different forms of money coexist.

Recent commentary has suggested that the financial system of the future may include multiple forms of money, with central bank money still acting as the anchor.

That could mean:

- central bank money remains the public foundation

- bank deposits remain important for credit intermediation

- regulated stablecoins serve selected payment and settlement use cases

This is a more practical way to think about the future of digital money.

The Real Issue: How Should Stablecoins Be Regulated?

The biggest question is no longer whether stablecoins should exist.

The real policy question is:

How should stablecoins be allowed into the financial system?

That leads to practical regulatory issues such as:

- who can issue stablecoins

- what reserve assets are required

- whether users have guaranteed redemption at par

- how AML/KYC rules apply

- what consumer protection standards are needed

- whether issuers should get access to payment systems or central bank facilities

This is where the debate is moving now. The future of stablecoins will not be decided only by technology. It will be decided by rules, trust, and institutional design.

My View: The Most Likely Outcome Is Regulated Coexistence

My view is simple.

Central banks are right to be cautious. Money and payments are too important to leave entirely outside the public regulatory perimeter.

But it is also unrealistic to think stablecoins will simply disappear. They already serve real demand, especially in cross-border payments, digital asset settlement, and blockchain-based financial activity.

That is why the most realistic path is neither total rejection nor blind acceptance.

It is regulated coexistence.

The winners in this space will not be the countries that simply ban stablecoins or fully surrender to them. They will be the ones that answer the hard questions first:

- Which stablecoins are allowed?

- Under what reserve rules?

- With what level of supervision?

- And for which use cases?

That is where the future of stablecoin regulation and digital money will be decided.

Key Takeaways

- Stablecoins are now important enough to matter for mainstream finance.

- Central banks worry about monetary sovereignty, financial stability, and regulatory control.

- The market supports stablecoins because of speed, efficiency, and on-chain utility.

- The real debate is not whether stablecoins should exist, but how they should be regulated.

- The most realistic outcome is likely regulated coexistence between public money, bank money, and private digital money.

References

[1]: PaymentExpert, Why stablecoins have central bankers running scared, June 26, 2025.

[2]: OMFIF, Why central banks should embrace stablecoins, January 19, 2026.

[3]: Binance Square, Why are central banks concerned about stablecoins?