From SEPA and instant payments to TIPS, cards, and cross-border euro transfers, here is how payment systems in Europe actually work

You send money from one European country to another. It feels like it should be easy.

And increasingly, that is the whole point.

That is what makes payment systems in Europe so interesting. Europe is not one country. It is a region with different banks, different languages, different regulators, and different national habits. Yet when it comes to euro payments, the long-term goal has been to make money move more like it is happening inside one market rather than across a patchwork of separate ones.

That is why payment systems in Europe are not just a story about faster transfers. They are a story about building payment infrastructure across borders in a way that feels simple to ordinary users.

Europe’s payments story is really about making borders matter less

The easiest way to understand payment systems in Europe is this: Europe has been trying to make euro payments feel less fragmented.

That matters because payments become awkward very quickly when every country works differently. If transferring money across borders feels slower, more expensive, or more confusing than paying domestically, the market never really feels connected.

That is where SEPA becomes the main character.

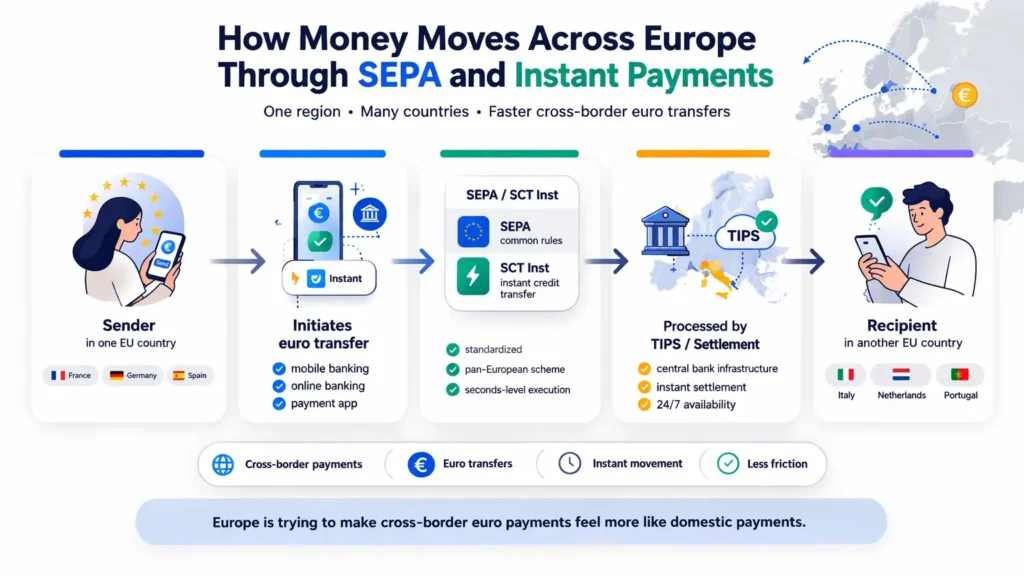

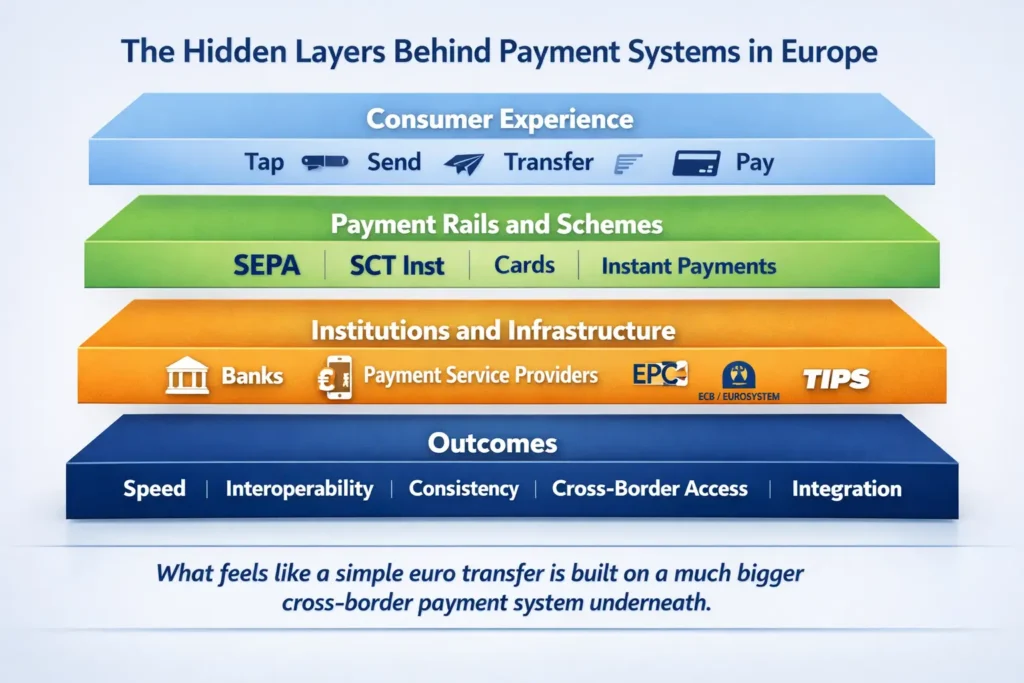

SEPA, the Single Euro Payments Area, was built to make cashless euro payments across Europe work more like domestic payments. In simple terms, it is part of the project of making Europe feel more connected at the payments level, even if the political and banking structures remain complex.

That is one reason payment systems in Europe are such a strong topic. The story is not just about new technology. It is about reducing friction across a whole region.

SEPA is the foundation of payment systems in Europe

If there is one concept people need to understand first, it is SEPA.

SEPA changed the way euro payments are organized by harmonizing the rules and standards around non-cash euro transfers. That does not mean every payment experience in Europe is identical. It means the underlying structure has been pushed toward consistency.

That is a big deal.

A payment system becomes much more powerful when users do not need to think constantly about whether the sender and receiver are in the same country. That is exactly why payment systems in Europe matter so much in the global conversation. Europe’s payment story is not only about speed. It is also about interoperability and standardization across borders.

If the U.S. story is about multiple domestic rails and the India story is about UPI changing everyday behavior, Europe’s story is about what happens when many countries try to make cross-border payments feel normal.

Instant payments are changing expectations across Europe

Now the story gets more current.

For a long time, “European payments” often sounded efficient in theory but not always instant in practice. That has been changing. The European Central Bank explains that instant payments make funds available in the payee’s account within ten seconds. That simple idea has become much more important because it changes what people expect money to do.

Once people know that payments can move within seconds, waiting starts to feel less acceptable.

That is why payment systems in Europe are entering a new phase. The conversation is no longer only about standardizing payments. It is also about making those standardized payments fast.

And this is not just market hype. The EU adopted new rules on instant euro payments in 2024, and the European Commission has made clear that payment service providers in the euro area must charge the same or lower fees for instant payments as for regular transfers. That turns instant payments from a premium feature into something much closer to normal infrastructure.

SCT Inst is one of the most important pieces

One of the key terms in payment systems in Europe is SCT Inst, or SEPA Instant Credit Transfer.

This is one of the schemes that makes pan-European instant euro transfers possible. It is designed around the idea that money should move quickly across participating payment service providers and across borders inside the wider SEPA framework.

This matters because payment systems are not transformed by slogans. They are transformed by rulebooks, standards, and participation.

That may sound less exciting than flashy apps, but it is actually the reason Europe’s payments story is so important. A lot of payment innovation around the world is product-led. Europe’s approach often looks more infrastructure-led. It is about building a common system that many providers can plug into.

That is exactly why payment systems in Europe are worth paying attention to. The interesting part is not just the user experience. It is the architecture underneath.

TIPS helps power the instant side of the system

If SEPA is the wider payments framework, then TIPS is one of the pieces that helps the instant side of the system work.

TIPS, or TARGET Instant Payment Settlement, is the Eurosystem’s market infrastructure service for settling instant payments in central bank money. The ECB says it enables payment service providers to offer real-time fund transfers around the clock, every day of the year.

That matters because fast payments still need strong infrastructure underneath them. Otherwise, “instant” remains just a surface promise.

This is one of the most interesting parts of payment systems in Europe. The region is not only trying to make payments faster at the customer level. It is also building the deeper settlement and infrastructure layers needed to support that speed reliably across borders.

Cards still matter, but they are not the whole story

Even in a system increasingly shaped by transfers and instant payments, cards still matter in payment systems in Europe.

People still tap cards in stores, use them online, and rely on them in everyday spending. But if you look at Europe’s long-term payments direction, the bigger policy and infrastructure conversation is often less about card dominance and more about account-to-account transfers, instant euro payments, and reducing cross-border friction.

That is one of the reasons Europe feels different from some other payment markets. The most interesting story is not just consumer card usage. It is the broader effort to build a payments environment where transfers across countries feel easier, faster, and more consistent.

Europe is trying to make complexity feel invisible

The smart thing about payment systems in Europe is that the ambition is not to make the system simple at the institutional level. Europe is still institutionally complex. The ambition is to make that complexity less visible to the user.

That is a very modern payment goal.

Users do not want to think about schemes, infrastructures, or legal harmonization every time they send money. They want payments to work. Europe’s payments strategy makes more sense once you see it that way. It is really about hiding complexity behind common standards and faster rails.

That is also why Europe keeps showing up in discussions about the future of payments. It is one of the clearest examples of how payment design and regulation can work together to reshape behavior across an entire region.

Why payment systems in Europe matter beyond Europe

Understanding payment systems in Europe is useful even if you do not live in the EU.

It shows what happens when a payments market tries to unify across borders instead of staying trapped inside national systems. It shows how regulation can push faster payments into the mainstream. And it shows that payments are not only about apps or checkout buttons. They are also about standards, schemes, settlement layers, and shared infrastructure.

That is what makes Europe such a strong entry in this series. If the U.S. story is about coexistence, India’s story is about UPI-led daily adoption, and Brazil’s story is about Pix turning instant payments into a habit, Europe’s story is about making many markets feel more like one.

Final thoughts

The simplest way to understand payment systems in Europe is this: Europe is trying to make money move across borders with less friction, more consistency, and much more speed.

SEPA provides the common framework. SCT Inst helps make instant euro transfers possible. TIPS supports real-time settlement infrastructure. And new EU rules are pushing instant payments further into the mainstream.

That is why Europe’s payments story matters. It is not just about speed. It is about turning a region of many countries into something that feels more connected when money moves.

References

- European Central Bank – Single Euro Payments Area (SEPA)

https://www.ecb.europa.eu/paym/retail/sepa/html/index.en.html - European Central Bank – What are instant payments?

https://www.ecb.europa.eu/paym/retail/instant_payments/html/index.en.html - European Central Bank – What is TIPS?

https://www.ecb.europa.eu/paym/target/tips/html/index.en.html

Read the Full Payment Systems Series

| Country / Region | Main Focus | Read More |

|---|---|---|

| United States | Cards, ACH, wire transfers, RTP, FedNow | Payment Systems in US |

| India | UPI, QR payments, NEFT, RTGS, RuPay | Payment Systems in India |

| Brazil | Pix, QR payments, cards, boleto | Payment Systems in Brazil |

| Europe | SEPA, instant payments, SCT Inst, TIPS | Payment Systems in Europe |

| Singapore | PayNow, FAST, SGQR, cross-border links | Payment Systems in Singapore |