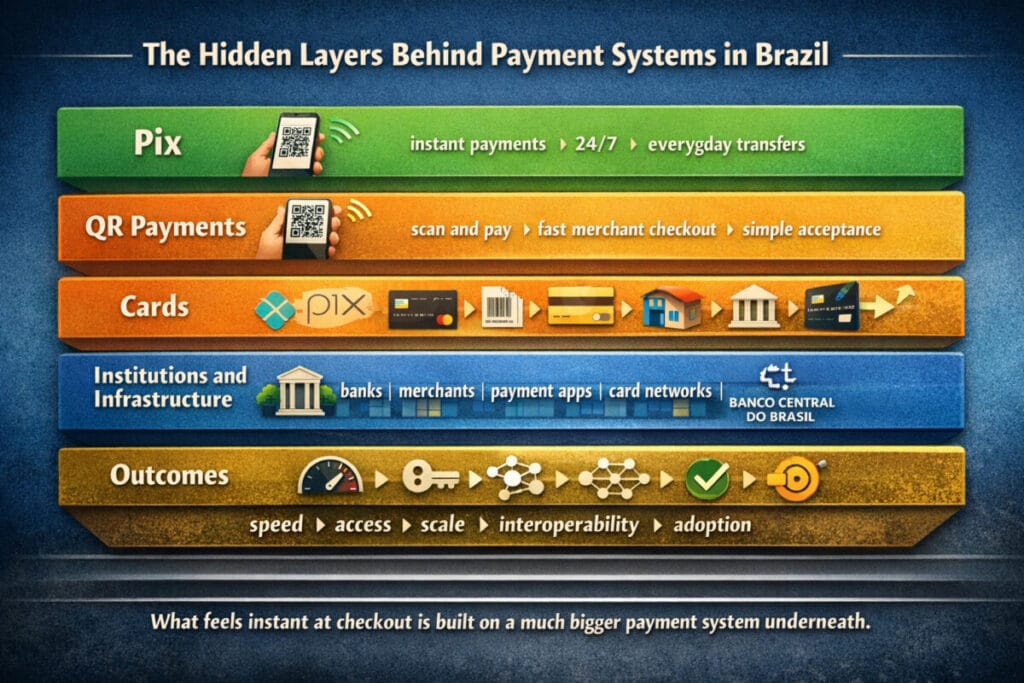

From Pix and QR payments to cards, boleto, and traditional bank transfers, here is how payment systems in Brazil actually work

You buy lunch. You scan a QR code. The payment lands in seconds.

You pay a friend back. Pix.

You buy something online. Maybe Pix again. Maybe a card. Maybe even boleto.

That is what makes payment systems in Brazil so interesting. Brazil is not just a country with digital payments. It is a country where one payment rail, Pix, changed the speed, feel, and culture of everyday money movement so quickly that it became impossible to ignore.

And that is the key point. payment systems in Brazil are not only about one successful product. They are about how a national payment ecosystem can shift when instant payments become normal for ordinary life.

Brazil feels different because Pix is not a side feature

In many countries, faster payments still feel like an upgrade, an option, or a niche tool. In Brazil, Pix feels much bigger than that.

The Central Bank of Brazil describes Pix as an easy, fast, affordable, safe, and versatile payment experience for end users and businesses. That helps explain why payment systems in Brazil feel different from the start. Faster money movement is not hidden behind technical language. It shows up in real daily behavior. People use it to pay friends, merchants, service providers, and businesses in ways that feel simple and immediate.

That is why Brazil stands out in any global payment series. The story is not just that instant payments exist. The story is that instant payments became part of everyday life.

Pix is the star of payment systems in Brazil

If there is one system that defines payment systems in Brazil, it is Pix.

Pix launched in November 2020 and quickly became the country’s most important payment story. The Central Bank’s official Pix statistics show the scale clearly. Monthly transactions have climbed into the billions, and annual transaction value has reached levels so large that Pix is no longer just a fast-payment success story. It is infrastructure.

That is what makes Pix so powerful. It did not just make payments quicker. It changed expectations.

Once people get used to sending money in seconds, twenty-four hours a day, seven days a week, the older idea of waiting starts to feel outdated. That shift is one of the biggest reasons payment systems in Brazil get so much attention from people studying the future of payments.

QR codes made Pix even stronger

One reason Pix spread so fast is that it worked beautifully with QR-based payments.

This matters more than it sounds.

A payment system does not become a national habit just because the underlying technology is strong. It becomes a habit when paying feels easy for both sides. In Brazil, QR payments helped make Pix practical in everyday commerce, from larger retailers to smaller merchants.

That is a huge part of why payment systems in Brazil feel so alive. The system is not trapped inside bank interfaces or formal financial settings. It shows up in the places where real spending happens.

When a payment rail is fast, simple, and easy to accept, adoption becomes much easier to imagine. When it works with QR in daily life, it starts to feel normal very quickly.

Cards still matter in payment systems in Brazil

Even with all the attention around Pix, payment systems in Brazil are not just about instant payments.

Cards still matter a lot. In fact, the Central Bank said in 2025 that Pix and cards were the most used payment instruments in Brazil. That tells you something important: Pix did not erase the rest of the system overnight. It changed the balance of the system.

Cards remain important because they still fit many types of spending, especially in retail and e-commerce. Brazil also has its own strong card culture, including installment payments, which have long shaped how people shop.

That is why payment systems in Brazil are more interesting than a one-line “Pix won” story. Pix is dominant and transformative, but the broader payments environment still includes cards as a major part of everyday commerce.

Boleto still tells you something important about Brazil

If you want to understand payment systems in Brazil properly, you also need to know about boleto.

Boleto is one of the older and more traditional payment methods in Brazil. The Central Bank still lists boleto among the traditional instruments that continue to coexist with Pix, cards, and bank transfers. That coexistence matters because it shows how payment systems evolve in layers, not in a single clean replacement.

Boleto helps explain something deeper about Brazil’s payment culture. New rails can grow quickly without making every older method disappear at once. Some users, merchants, and use cases keep older methods relevant, even when the newer rail is clearly shaping the future.

That makes payment systems in Brazil feel more realistic and more useful as a case study. Real payment markets do not move like classroom diagrams. They move through overlap.

Traditional bank transfers still have a place

Brazil also has a broader payment infrastructure beyond Pix, including traditional transfer mechanisms inside the Brazilian Payments System.

That matters because payment systems in Brazil are not powerful only because Pix is popular. They are powerful because Pix sits inside a larger institutional and regulatory structure managed by the Central Bank.

In other words, the big story is not “Brazil made one good app.” The story is that Brazil built a modern payment environment where instant payments became central without turning the whole system into chaos.

That institutional layer is part of what makes the country so important in discussions about payment design.

Why payment systems in Brazil get so much global attention

There is a reason people keep talking about payment systems in Brazil.

Brazil offers something many countries want to understand: how to build a payment rail that is not only technically fast, but socially normal. A lot of markets talk about innovation. Brazil shows what innovation looks like when millions of people actually use it all the time.

That is why Pix gets so much global attention. It shows what happens when a central bank-led instant payment system becomes deeply embedded in ordinary behavior, merchant acceptance, and consumer expectations.

And that is what makes Brazil such a strong next chapter after the U.S. and India. If the U.S. story is about multiple rails coexisting and India’s story is about UPI reshaping daily payment behavior, Brazil’s story is about how Pix turned instant payments into a national habit.

Why this matters even if you do not live in Brazil

Understanding payment systems in Brazil is useful even if you never pay with Pix yourself.

It shows how quickly payment behavior can change when the system is easy enough, cheap enough, and accepted widely enough. It also shows that central bank-backed payment infrastructure can shape real consumer habits, not just policy discussions.

Most of all, Brazil reminds people that payments are not just about technology. They are about design, trust, access, timing, and daily convenience. When those things line up, a payment rail can move from “new feature” to “normal life” very fast.

Final thoughts

The simplest way to understand payment systems in Brazil is this: Brazil did not just launch an instant payment system. It changed the pace of everyday money movement.

Pix is the center of that story. QR payments helped make it feel natural in ordinary commerce. Cards still matter. Boleto still helps explain the country’s layered payment culture. And the broader Brazilian Payments System provides the structure underneath it all.

That is why Brazil is such an important payments story. It is not just fast. It shows what happens when fast becomes normal.

References

- Banco Central do Brasil – Pix Statistics

https://www.bcb.gov.br/en/financialstability/pixstatistics - Banco Central do Brasil – Pix is now the most used payment method in Brazil

https://www.bcb.gov.br/en/pressdetail/2588/nota

Read the Full Payment Systems Series

| Country / Region | Main Focus | Read More |

|---|---|---|

| United States | Cards, ACH, wire transfers, RTP, FedNow | Payment Systems in US |

| India | UPI, QR payments, NEFT, RTGS, RuPay | Payment Systems in India |

| Brazil | Pix, QR payments, cards, boleto | Payment Systems in Brazil |

| Europe | SEPA, instant payments, SCT Inst, TIPS | Payment Systems in Europe |

| Singapore | PayNow, FAST, SGQR, cross-border links | Payment Systems in Singapore |