From UPI and QR payments to NEFT, RTGS, and RuPay, here is how payment systems in India actually work

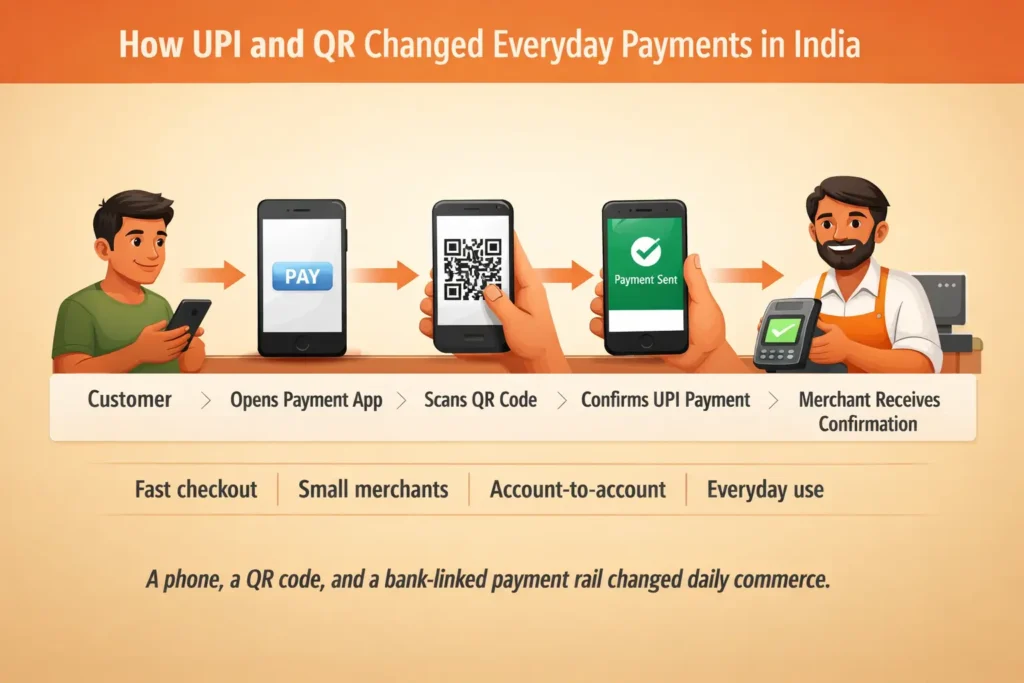

You buy tea from a street stall. You scan a QR code. Done.

You split dinner with friends. UPI. Done.

You pay a bill, top up a wallet, send money to family, or buy something from a tiny shop that would never have taken cards years ago. Again, done.

That is what makes payment systems in India so interesting. In many countries, digital payments still feel like one option among many. In India, digital payments often feel like the default rhythm of everyday life. Money does not just move through banks in the background. It shows up right in front of people, on phones, at shops, in apps, and in daily habits.

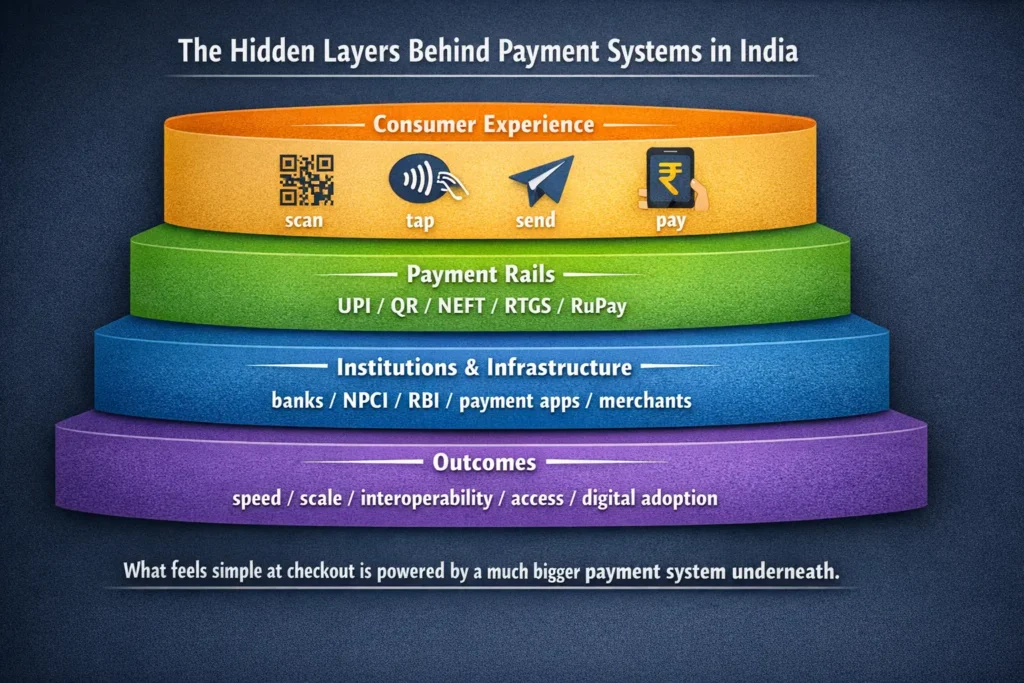

And once you look a little closer, you realize something important. payment systems in India are not just about fast transactions. They are about how a whole country built payment rails that feel usable at scale.

India feels different because payments feel built into daily life

The easiest way to understand payment systems in India is this: they do not feel hidden in the way many other payment systems do. They feel visible.

In some countries, digital payments still depend heavily on cards, bank portals, or slower transfer habits. In India, the payment experience often feels much more direct. Open the app, scan the code, send the money, move on. That simplicity is a huge part of why the system feels so alive.

But the big story is not just convenience. It is that India built a payment environment where digital movement of money became normal across a very wide range of users, merchants, and situations. That is a much bigger achievement than just making one app popular.

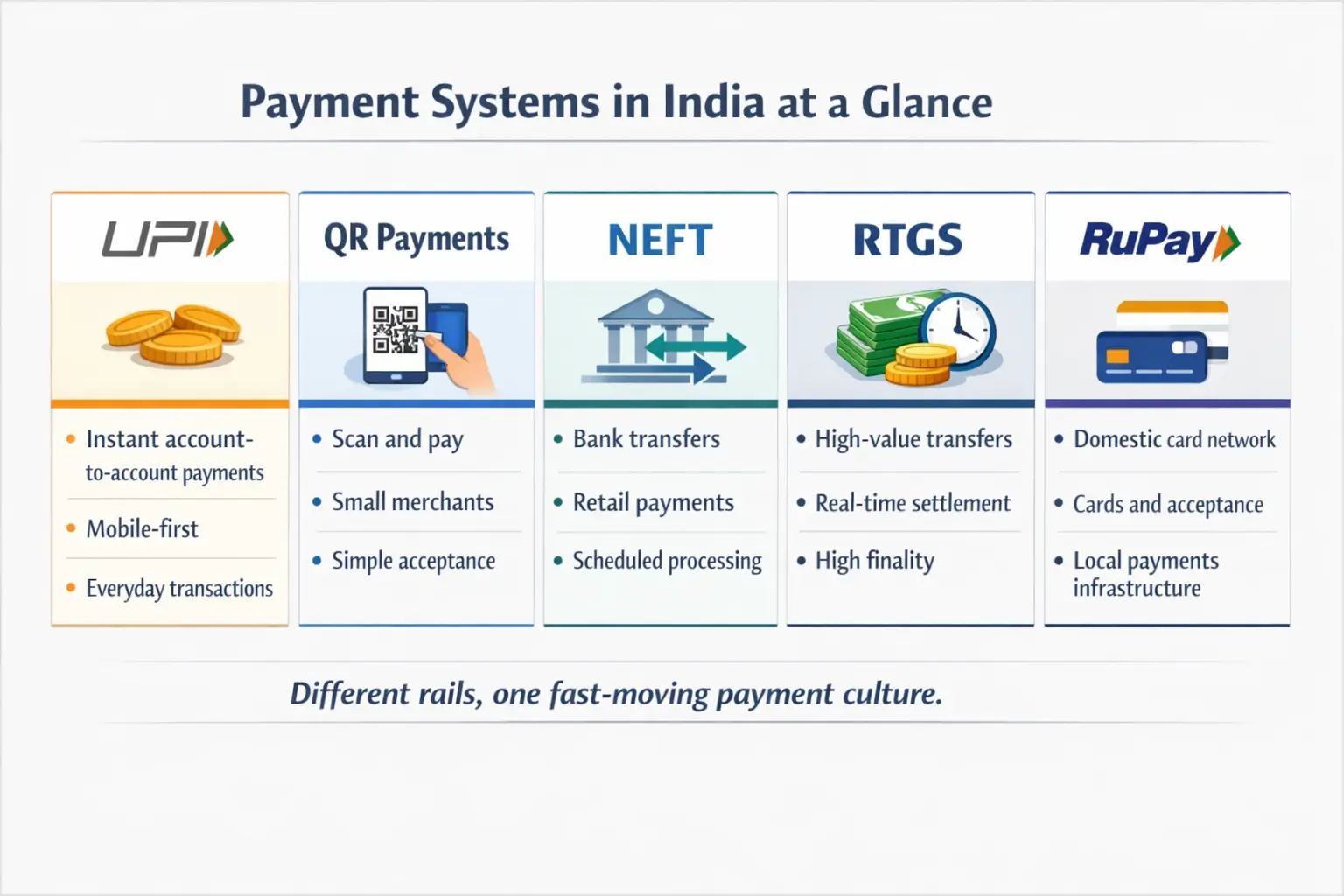

UPI is the star of payment systems in India

If there is one system that defines payment systems in India, it is UPI.

UPI, or Unified Payments Interface, changed the feel of digital payments in India. It made account-to-account payments fast, simple, and easy to use through mobile apps. Instead of thinking about long account details every time, users could rely on a much more practical payment experience.

That matters because the best payment systems do not just move money. They reduce friction.

UPI did exactly that. It made small everyday payments feel digital without making them feel complicated. It made person-to-person transfers easier. It made merchant payments more natural. It helped turn QR codes into a real everyday payment habit rather than just a tech demo.

That is why payment systems in India are so often discussed through the lens of UPI. It is not just another product inside the system. It is the system feature that changed public expectations.

QR payments made digital payments feel normal

One of the smartest things about payment systems in India is that they do not rely only on expensive hardware or traditional card acceptance setups. QR-based payments helped digital payments spread in a way that felt practical.

That matters more than people think.

A payment system does not become powerful only because the technology is advanced. It becomes powerful when people can actually use it easily. India’s payment story is strong partly because digital payments moved into ordinary places: small stores, food counters, local merchants, taxis, informal everyday commerce.

That changes everything.

Once a payment rail is easy for both users and merchants, adoption stops feeling like a special event. It starts feeling normal. That is exactly what makes payment systems in India stand out.

NEFT and RTGS still matter

Even though UPI gets most of the attention, payment systems in India are not only about UPI.

India also has NEFT and RTGS, and both still matter because not every payment need is the same. NEFT supports electronic retail funds transfer across banks and works well for many standard account transfers. RTGS is the serious lane for higher-value transactions where real-time transfer and finality matter more.

This layered structure is important. It shows that India did not replace everything with one single rail. Instead, it built a system where different rails serve different jobs.

That is one reason the payment ecosystem feels strong rather than trendy. UPI may dominate the conversation, but the broader system still includes rails built for different payment sizes, speeds, and use cases.

RuPay is part of the bigger story too

Another reason payment systems in India are interesting is that India’s payment landscape is not only about transfers. It also includes card infrastructure, and RuPay plays an important role there.

RuPay matters because it reflects something bigger than just card issuance. It is part of India’s broader effort to build domestic payment infrastructure instead of relying only on global rails. That gives the system more local depth and helps explain why India’s payment conversation often sounds different from the payment conversation in countries that lean much more heavily on international card networks.

So while UPI grabs most of the spotlight, RuPay helps round out the larger picture of how payment systems in India evolved.

This is not just about speed. It is about scale

A lot of countries want faster payments. India’s more interesting story is that it managed to pair speed with scale.

That is a huge difference.

A payment system can look impressive in a product demo. It becomes truly important when millions of people use it for ordinary life. Then it stops being a feature and becomes infrastructure.

That is what happened with payment systems in India. The story is not just that digital payments became available. The story is that they became normal across a very large and diverse population. That gives India a very different place in the global payments conversation.

Why payment systems in India get so much global attention

People around the world pay attention to payment systems in India because India is no longer just another market adopting digital payments. It is a case study in how payment design can shape behavior.

The country’s payment ecosystem shows what happens when ease of use, interoperability, and digital habits start reinforcing each other. Once people trust the system, and once merchants expect people to pay digitally, and once sending money feels almost effortless, the network effect becomes very hard to ignore.

That is why India keeps coming up in discussions about the future of payments. It is not only innovating in theory. It is showing what high-volume digital payment behavior looks like in real life.

Why this matters even if you do not live in India

Understanding payment systems in India is useful even if you never use UPI yourself.

It helps explain where payment systems may be heading. It shows that real payment innovation is not just about launching new apps or adding prettier buttons. It is about reducing friction so effectively that digital payments become part of daily instinct.

It also shows that cards are not the only way a modern payment system can scale. In some markets, account-to-account systems can become much more central to everyday commerce than outsiders expect.

That is part of what makes India such a fascinating next stop in this series. If the U.S. story is about multiple rails coexisting, the India story is about what happens when one rail changes daily behavior at enormous scale.

Final thoughts

The simplest way to understand payment systems in India is this: India did not just digitize payments. It made digital payments feel natural.

UPI changed the everyday payment experience. QR payments helped push digital acceptance into ordinary commerce. NEFT and RTGS still matter for broader transfer needs. RuPay adds another layer to the domestic payments story.

So when people talk about India as one of the most important payment markets in the world, they are not just talking about technology. They are talking about a payment system that became part of how daily life actually works.

References

- Reserve Bank of India – Payment and Settlement Systems Act, 2007

https://www.rbi.org.in/commonman/english/scripts/FAQs.aspx?Id=420 - NPCI – UPI: Unified Payments Interface

https://www.npci.org.in/product/upi - Reserve Bank of India – National Electronic Funds Transfer (NEFT) System

https://www.rbi.org.in/commonman/english/scripts/FAQs.aspx?Id=274

Read the Full Payment Systems Series

| Country / Region | Main Focus | Read More |

|---|---|---|

| United States | Cards, ACH, wire transfers, RTP, FedNow | Payment Systems in US |

| India | UPI, QR payments, NEFT, RTGS, RuPay | Payment Systems in India |

| Brazil | Pix, QR payments, cards, boleto | Payment Systems in Brazil |

| Europe | SEPA, instant payments, SCT Inst, TIPS | Payment Systems in Europe |

| Singapore | PayNow, FAST, SGQR, cross-border links | Payment Systems in Singapore |