Why SWIFT, sanctions, and financial sovereignty still shape global finance

When most people hear SWIFT, they think of a simple international payment network.

But that is only part of the story.

SWIFT is not just a technical system for banks. It sits at the center of global finance, cross-border payments, and increasingly, geopolitics. For some countries, SWIFT is the backbone of international banking. For others, it is a reminder that access to the global financial system can become a political issue very quickly.

That is what makes this topic so interesting.

A country being cut off from SWIFT does not mean money instantly disappears. It does not mean all trade stops overnight. But it does mean that international payments, trade settlement, and financial connectivity become slower, more expensive, and more uncertain.

In other words, losing access to SWIFT is not just a banking inconvenience. It can become an issue of economic pressure, sanctions exposure, and even financial sovereignty.

If you want to understand why SWIFT still matters, the official SWIFT overview is a useful starting point: SWIFT Overview

What SWIFT actually does

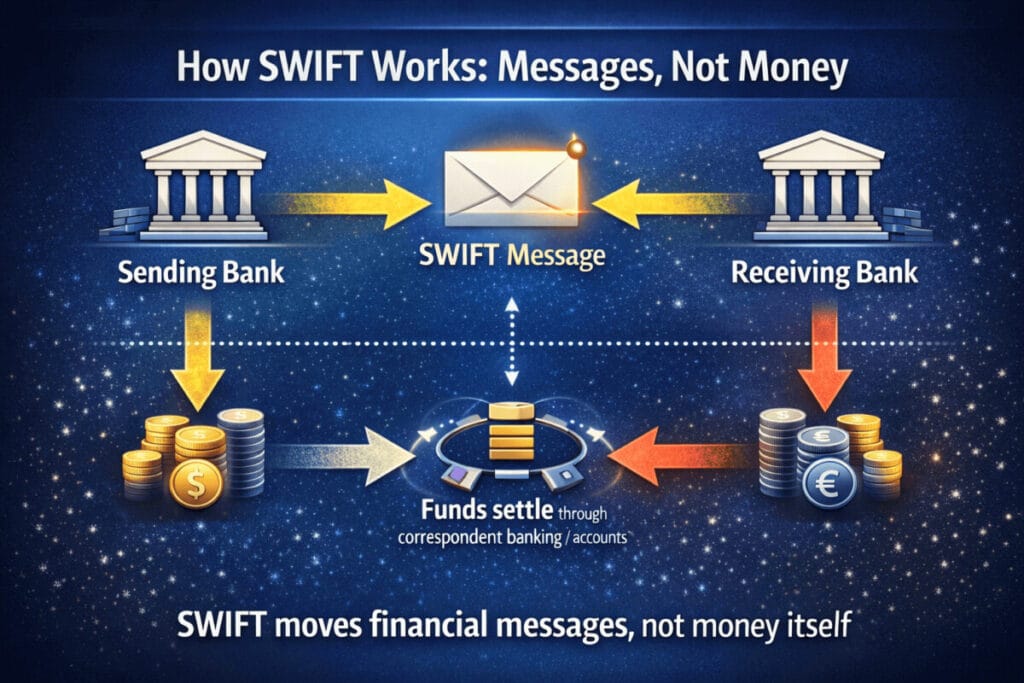

A lot of people assume SWIFT is the system that literally moves money around the world.

That is not quite right.

SWIFT is better understood as a global financial messaging network. It allows banks and financial institutions to send standardized, secure messages to each other. Those messages help coordinate international transactions, including cross-border payments, trade finance, securities activity, and other banking operations.

So when people say a country is “cut off from SWIFT,” what they usually mean is that its banks lose access to one of the most widely used communication networks in international finance.

That matters because global finance runs on trust, standards, and coordination.

If the messaging layer becomes harder to use, the whole process becomes more fragile.

Why being cut off from SWIFT is a big deal

Here is the simplest way to think about it:

Losing access to SWIFT does not always make international finance impossible.

It makes international finance much more difficult.

That difference matters.

Countries and banks may still find workarounds. They may use intermediary banks, alternative messaging channels, regional payment arrangements, or bilateral settlement methods. But each workaround creates more friction.

And in finance, friction means higher cost, slower transactions, and more risk.

A quick summary

| Area | Normal SWIFT Access | Cut Off from SWIFT |

|---|---|---|

| Bank messaging | Standardized and widely accepted | More limited and fragmented |

| Cross-border payments | Relatively predictable | Slower and less efficient |

| Trade settlement | Easier to coordinate | More operational friction |

| Financial confidence | Stronger connectivity | Higher uncertainty |

| Strategic position | Integrated into global finance | Greater pressure to build alternatives |

1. Cross-border payments become slower and more expensive

International payments are already more complicated than domestic transfers.

A typical transaction may involve the sending bank, the receiving bank, one or more correspondent banks, compliance checks, and settlement accounts. SWIFT helps hold this process together by providing a shared language for financial messaging.

If that shared language is removed, transactions do not necessarily stop, but they become harder to process. Banks may need to rely on indirect routes or less efficient communication channels. That increases transaction time, raises operational risk, and often adds cost.

For businesses, this matters immediately. A delayed supplier payment is not just a technical problem. It can become a working capital problem, a procurement problem, or even a contract problem.

2. Trade settlement becomes more difficult

This is where a financial infrastructure issue turns into a real economy issue.

International trade depends on confidence that payments will be made and received smoothly. If a country’s banks lose convenient access to SWIFT, exporters, importers, suppliers, and counterparties may start asking uncomfortable questions.

- Will this payment be delayed?

- Will the bank on the other side be able to process it normally?

- Will another intermediary bank be needed?

- Is this transaction worth the additional risk?

That uncertainty matters.

A country may still trade, but the process becomes less efficient. And once trade settlement becomes harder, the impact can spread far beyond the banking sector.

3. Sanctions become more powerful

This is one of the most politically important parts of the SWIFT story.

SWIFT is often discussed as if it were a neutral technical network. In practice, the issue of access can become deeply connected to sanctions and geopolitical pressure.

That is one reason the SWIFT debate is so much more interesting than a normal payments story. It is not only about how banks communicate. It is also about who remains connected to the dominant infrastructure of global finance.

If you want a policy-focused view, the European Council’s sanctions timeline is useful context:

4. Financial markets start pricing in more uncertainty

Finance runs on confidence.

If banks in a country are cut off from a major global messaging network, other institutions often become more cautious. Even if some transactions are still technically possible, counterparties may demand more checks, more documentation, or more compensation for risk.

That can show up in different ways:

- fewer willing counterparties

- higher transaction costs

- greater settlement uncertainty

- reduced foreign currency flexibility

- weaker investor confidence

This is why the impact of losing access to SWIFT can go beyond what the technology itself seems to imply.

The direct effect is operational. The indirect effect is psychological and financial.

And sometimes the indirect effect matters just as much.

5. Countries start thinking about alternatives to SWIFT

Once access to a dominant network looks politically uncertain, countries begin to ask a different question:

What if we need a backup?

That is where the discussion moves from SWIFT to financial sovereignty.

A country may not expect to replace SWIFT overnight. But it may still want a domestic or regional alternative for strategic reasons. That is especially true in a world where sanctions, payment infrastructure, and geopolitical rivalry are becoming more closely linked.

This is why discussions about alternative networks are not only technical. They are also strategic.

6. But alternatives are harder than they look

This is where a lot of commentary becomes too simplistic.

It is easy to say, “If SWIFT is risky, countries should just build their own system.”

But building an alternative to SWIFT is not like launching a new app.

A serious alternative needs more than software. It needs:

- participating institutions

- trusted standards

- correspondent relationships

- legal and regulatory alignment

- market acceptance

- operational scale

That is why the most difficult part of replacing SWIFT is not the code.

It is the network effect.

A payment network becomes powerful when everyone important is already connected to it. That is exactly why SWIFT has remained so influential for so long.

7. In the end, this is about power, not just technology

This is the biggest reason SWIFT still matters.

At first glance, SWIFT looks like an old financial network. But once you look closer, it becomes something bigger: a system tied to global finance, sanctions, state strategy, and financial sovereignty.

That is why the question is not just:

“How does SWIFT work?”

The more interesting question is:

“Who can stay connected to the financial system that everyone else depends on?”

That is no longer just a payments question.

It is a question about power.

Three common misunderstandings about SWIFT

Myth 1: SWIFT moves money directly

Not exactly. SWIFT mainly supports secure, standardized financial messaging. Settlement itself depends on other banking relationships and account structures.

Myth 2: Being cut off from SWIFT means total economic isolation overnight

Not necessarily. Workarounds may still exist. But those workarounds are usually slower, more expensive, and less efficient.

Myth 3: Any country can easily replace SWIFT with a domestic network

In theory, a country can build messaging infrastructure. In practice, replacing a deeply embedded global network is far more difficult because of trust, scale, and international acceptance.

Final thoughts

So, what happens if a country is cut off from SWIFT?

The answer is not “everything stops.”

The better answer is “everything gets harder.”

Cross-border payments become less efficient.

Trade settlement becomes more complicated.

Sanctions become more effective.

And the pressure to build alternatives to SWIFT grows stronger.

That is why SWIFT still matters.

It is old, yes.

But in global finance, old infrastructure can still be the most powerful infrastructure of all.